|

|

|

|

|||||

|

|

|

Pentair plc PNR is set to release its second-quarter 2025 results on July 22, before the opening bell.

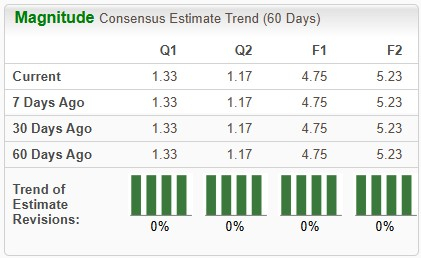

The Zacks Consensus Estimate for PNR’s second-quarter sales is pegged at $1.11 billion, indicating 1.4% growth from the year-ago reported figure.

The consensus estimate for earnings is pegged at $1.33 per share. The Zacks Consensus Estimate for PNR’s earnings has been unchanged in the past 60 days. The estimate indicates year-over-year growth of 9%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

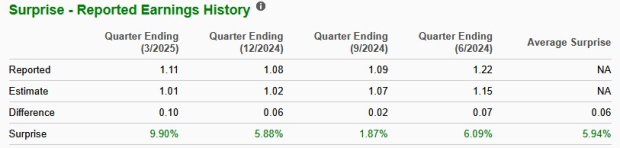

PNR’s earnings beat the Zacks Consensus Estimates in the trailing four quarters, the average surprise being 5.9%. This is depicted in the following chart.

Our model does not predict an earnings beat for Pentair this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you can see below.

You can uncover the best stocks before they are reported with our Earnings ESP Filter.

Earnings ESP: Pentair has an Earnings ESP of +1.26%.

Zacks Rank: PNR currently carries a Zacks Rank of 4 (Sell).

After witnessing lower volumes for five consecutive quarters, the pool segment saw a rebound in volumes in the second quarter of 2024 with 17.1% growth. However, volume growth has since decelerated to 4.1% in the third quarter and 2% in the fourth quarter of 2024. In the first quarter of 2025, it declined to 1.5%. The company expects the Pool segment’s sales to increase 4-5% in 2025. However, considering that new pool builds in 2024 were at historical lows, and the company expects it to be relatively flat in 2025, this raises concerns about the achievability of these targets.

We anticipate lower volume growth of 1.2% for the second quarter of 2025. Pricing is expected to have had a favorable impact of 1.4%. This is expected to have been offset by the unfavorable impacts of currency translation of 0.5%. Our model projects the Pool segment’s sales to be $399 million, indicating a year-over-year rise of 2.1%.

The Flow and Water Solutions segments continue to bear the impacts of a weak residential market due to high interest rates. However, a slight pickup in volumes is likely to have aided the segment in the to-be-reported quarter.

We expect the Flow segment’s sales to be $407 million, indicating an increase of 2.5% from the prior-year quarter’s actual. Our model predicts a 2.2% year-over-year increase in volumes, while pricing is expected to have a positive impact of 1.2%. Currency impacts are projected at a negative 0.9%.

Our model predicts the Water Solutions segment’s net sales to decline 1.3% year over year to $306 million. Ongoing weakness in the residential vertical is expected to lead to a 1.8% dip in volumes, which will likely be offset by a 1.1% rise in pricing. The unfavorable impacts of currency translation of 0.6% are also expected to have lowered its sales.

Pentair has been witnessing a tight supply of raw materials, along with rising logistics costs. Despite the weakness in the Water segment and cost headwinds, the company has delivered margin expansion across its segments, aided by pricing, cost savings and gains from its Transformation initiatives. We expect this to have continued in the second quarter as well.

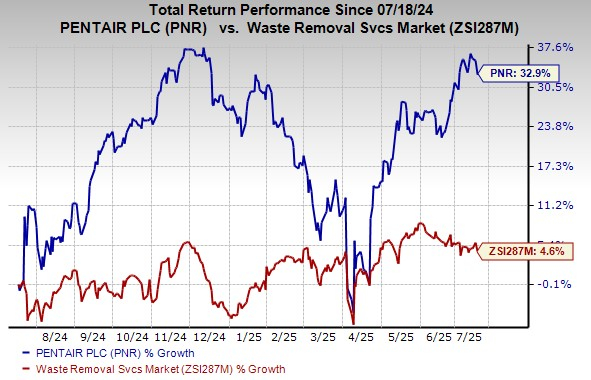

Pentair shares have gained 32.9% in the past year compared with the industry’s 4.6% growth.

Here are some companies with the right combination of elements to post an earnings beat in their upcoming releases.

Emerson Electric Co. EMR, expected to release earnings on Aug 6, currently has an Earnings ESP of +0.46% and a Zacks Rank of 3. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Emerson Electric’s earnings for the third quarter of fiscal 2025 is pegged at $1.51 per share, indicating year-over-year growth of 5.6%. EMR has a trailing four-quarter average surprise of 3.4%.

Illinois Tool Works Inc. ITW, slated to release second-quarter 2025 results on July 30, has an Earnings ESP of +0.97% and a Zacks Rank of 3 at present.

The Zacks Consensus Estimate for Illinois Tool Works’ second-quarter 2025 earnings is pegged at $2.55 per share, suggesting a year-over-year rise of 0.4%. ITW has a trailing four-quarter average surprise of 3%.

Crown Holdings, Inc. CCK is scheduled to release second-quarter 2025 results on July 21. It currently has an Earnings ESP of +0.27% and a Zacks Rank of 3.

The Zacks Consensus Estimate for Crown Holdings’ earnings is pegged at $1.86 per share, which indicates a year-over-year increase of 2.8%. CCK has a trailing four-quarter average surprise of 16.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-28 | |

| Apr-27 | |

| Apr-27 | |

| Apr-23 | |

| Apr-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite