|

|

|

|

|||||

|

|

|

Philip Morris International Inc. PM is likely to register growth in its top and bottom lines when it reports second-quarter 2025 earnings on July 22, before the market opens.

The Zacks Consensus Estimate for revenues is pegged at almost $10.3 billion, implying an 8.3% increase from the prior-year quarter’s reported figure. The consensus mark for quarterly earnings has risen by a penny in the past 30 days to $1.85 per share, suggesting an increase of 16.4% from the figure reported in the year-ago quarter.

Philip Morris has a trailing four-quarter average earnings surprise of 3.6%. Nevertheless, in the last reported quarter, the company’s bottom line surpassed the Zacks Consensus Estimate by a margin of 5%. (Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.)

Our proven model doesn’t conclusively predict an earnings beat for Philip Morris this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Philip Morris has an Earnings ESP of -0.04% and a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Philip Morris International Inc. price-consensus-eps-surprise-chart | Philip Morris International Inc. Quote

Philip Morris’ ability to leverage strong pricing has been a key driver of its revenue and operating income growth. Smokers’ propensity to absorb price increases, given the addictive nature of cigarettes, has enabled the company to sustain revenue growth.

The company has continued to benefit from its significant strides toward a smoke-free future. Smoke-free products accounted for 44% of Philip Morris’ gross profit in the first quarter of 2025, reflecting the growing success of IQOS ILUMA, its flagship heat-not-burn device. Key innovations like ZYN nicotine pouches and VEEV ONE e-vapor have also been making substantial progress in driving the company’s smoke-free growth.

These upsides bode well for the quarter to be reported. The Zacks Consensus Estimate for total smoke-free product revenues (excluding Wellness and Healthcare) for the first quarter is pegged at $4,225.9 million, indicating an increase from $3,530 million recorded in the year-ago period. Apart from this, Philip Morris’ cost-saving measures and strategic initiatives to enhance its margins have been working well.

Building on its strong start to the year, Philip Morris is expected to have sustained solid momentum in smoke-free products during the second quarter. Management anticipates IQOS HTU adjusted IMS growth of around 10%. ZYN shipments in the U.S. are expected to have remained at similar levels to the first quarter as trade restocking continues, with further acceleration likely in the second half of the year.

On its last earnings call, PM forecasted adjusted earnings in the range of $1.80 to $1.85 for the second quarter, including a favorable currency impact of 6 cents a share. Performance in the quarter is likely to reflect the company’s efforts to expand its smoke-free portfolio, maintain pricing power in combustibles, and drive operational efficiencies, all of which remain key factors to monitor in the upcoming results.

Shares of Philip Morris have gained 9.7% over the past three months, outperforming the Zacks industry’s growth of 10.2%. However, the stock lagged behind the S&P 500’s robust advance of 19.5% over the same period.

Performance among major tobacco players, such as Altria Group Inc. MO, Turning Point Brands, Inc. TPB and British American Tobacco p.l.c. BTI, has varied over the past three months. Philip Morris was outpaced by Turning Point Brands, which surged 34.9%, and British American Tobacco, which gained 22.4%. However, PM outperformed Altria, which posted a more modest increase of 0.3% during the same period.

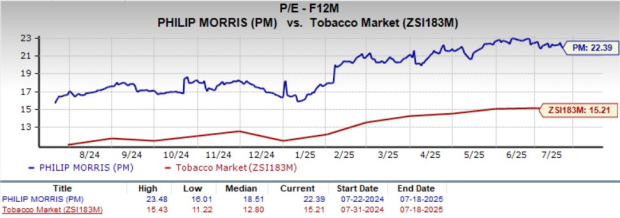

From a valuation perspective, PM is trading at a premium compared with industry benchmarks. The company’s forward 12-month price-to-earnings multiple of 22.39X remains above the industry average of 15.21X. The company also outperformed its peers, Altria Group, Turning Point Brands, and British American Tobacco, which are all trading at lower forward P/E ratios of 10.63X, 21.55X and 10.76X, respectively.

Philip Morris’ strong momentum in smoke-free products, combined with pricing power and solid earnings growth prospects, makes it an appealing choice for investors looking for exposure to the evolving global tobacco sector. Although the stock trades at a premium to peers, its growth profile and strategic transformation justify the valuation. Both existing and prospective investors could view the current levels as an opportunity to buy into the stock.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite