|

|

|

|

|||||

|

|

|

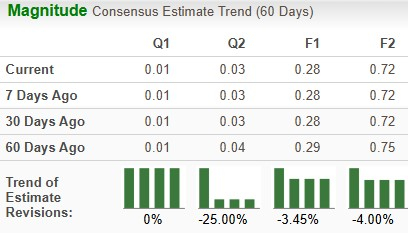

Intel Corporation INTC is scheduled to report its second-quarter 2025 earnings on July 24, after the closing bell. The Zacks Consensus Estimate for sales and earnings is pegged at $11.87 billion and a penny per share, respectively. Over the past 60 days, estimates for INTC have declined 3.45% to 28 cents for 2025 and decreased 4% to 72 cents for 2026.

The leading semiconductor manufacturer delivered a four-quarter earnings surprise of negative 76.25%, on average, beating estimates only once. In the last reported quarter, the company’s earnings surprise was 1200.00%.

Our proven model does not predict a likely earnings beat for Intel for the second quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Intel currently has an ESP of -350.00% with a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

During the quarter, Intel has successfully achieved industry-first full NPU (Neural Processing Unit) compliance in the MLPerf Client v0.6 benchmark. MLPerf is an industry-standard benchmarking suite created to assess AI system performance. The newly released MLPerf Client v0.6 Benchmark is a subset of MLPerf designed to evaluate client devices such as laptops and PCs with a strong emphasis on large language model acceleration and NPU performance. During the process, Intel Core Ultra Series 2 processors showcased the fastest NPU response time with an impressive token latency and highest NPU throughput. This is likely to boost prospects in the emerging market of AI PCs.

In the quarter under review, Intel expanded its collaboration with original equipment manufacturers like HP and Lenovo to develop next-generation AI PC. HP’s recent lineup of cutting-edge AI PCs, including EliteBook X, EliteBook Ultra and EliteBook 8, is powered by Intel Core Ultra series processors. Lenovo also deployed the Intel Core Ultra processor to power its leading-edge AI PC ThinkBook Plus Gen 6 Rollable. The company is also witnessing healthy demand for its Xeon 6 processor in high-performance computing (“HPC”) and AI-driven workloads. The processor offers significantly faster memory performance at high-capacity configurations compared with its competitor Advanced Micro Devices’ AMD EPYC processor.

Intel also expanded its Arc GPU lineup to deliver an impressive AI experience for PC, workstation and edge use cases. These factors are expected to have a favorable impact on second-quarter earnings. However, Intel’s growing ambition in GPU space is threatened by NVIDIA Corporation NVDA’s strong presence in the GPU domain across AI, cloud and data center applications.

In the to-be-reported quarter, Intel announced that it has inked a definitive agreement with Silver Lake to sell 51% of the Altera business. It will significantly bolster Intel’s liquidity position and drive investment in growth initiatives.

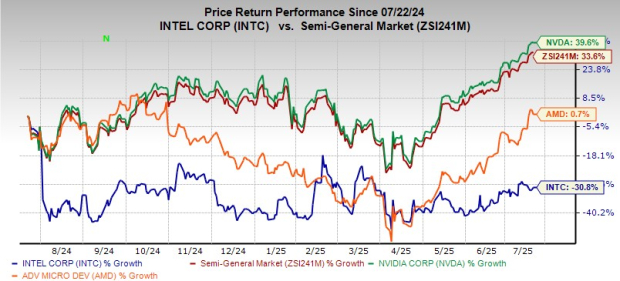

Over the past year, Intel has lost 30.8% against the industry’s growth of 33.6%. The company has also underperformed its peers like NVIDIA and AMD. NVIDIA has surged 39.6%, while AMD has increased 0.7% during this period.

From a valuation standpoint, Intel appears to be relatively cheaper than the industry and below its mean. Going by the price/sales ratio, the company shares currently trade at 1.94 forward sales, lower than 15.78 for the industry.

Intel has been undertaking several strategic decisions to gain a firmer footing in the expansive AI sector, spanning cloud and enterprise servers to networks, volume clients and ubiquitous edge environments, in tune with the evolving market dynamics. AI has moved from a niche capability to a critical must-have component for businesses. Organizations across sectors are rapidly moving to integrate AI to boost productivity and streamline workflow across operations. Intel is well-positioned to gain from this trend.

With AI at its core, Intel is swiftly expanding its portfolio offerings to support a wide range of use cases such as IT applications, gaming, content development and more. Intel’s collaboration with major manufacturers such as HP, Dell, Lenovo and Microsoft augurs well for long-term growth.

The company has been undertaking several strategic restructuring initiatives to trim operating costs and boost liquidity. It is winding up the automotive business to focus more on its core operations. This is expected to free up significant resources available for R&D funding in the core PC and data center segments. This bodes well for long-term growth.

Growing prowess in the AI PC market and strategic partnership with major manufacturers are expected to be major growth drivers in the upcoming quarters. The company has made significant strides in its cost-cutting plan to rebuild a sustainable growth engine. Strategic divestiture for focus on primary growth engines and liquidity improvement is a positive. Strong focus on innovation and enhancing portfolio strength are tailwinds. With a Zacks Rank #1, Intel appears to be primed for further stock price appreciation. Intel’s cheaper valuation could be a favorable entry point for investors ahead of the second quarter earnings.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 15 min | |

| 24 min | |

| 26 min | |

| 32 min | |

| 34 min | |

| 36 min | |

| 53 min | |

| 53 min | |

| 55 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite