|

|

|

|

|||||

|

|

|

The Coca-Cola Company KO has reported second-quarter 2025 results, with the bottom line surpassing the Zacks Consensus Estimate. Meanwhile, the top line missed the consensus mark. The company’s revenues and earnings per share (EPS) improved year over year. The results have benefited from continued business momentum, aided by enhanced pricing across markets. This quarter’s results once again highlight the strength of KO’s resilient, all-weather strategy.

Coca-Cola reported a comparable EPS of 87 cents in the second quarter, up 4% from the year-ago period. Comparable EPS also beat the Zacks Consensus Estimate of 83 cents. Unfavorable currency translations hurt the comparable EPS by 5 percentage points. Comparable currency-neutral earnings per share rose 9% year over year.

Revenues of $12.54 billion grew 1% year over year but missed the Zacks Consensus Estimate of $12.59 billion. Organic revenues rose 5% from the prior-year quarter, led by growth across all segments, except for Bottling Investments. Coca-Cola’s reported revenues benefited from growth across most operating segments, except for Latin America and Bottling Investments. The improved price/mix in the quarter was offset by lower concentrate sales and adverse currency rates.

For the second quarter of 2025, KO gained a global value share in the total non-alcoholic ready-to-drink beverages category.

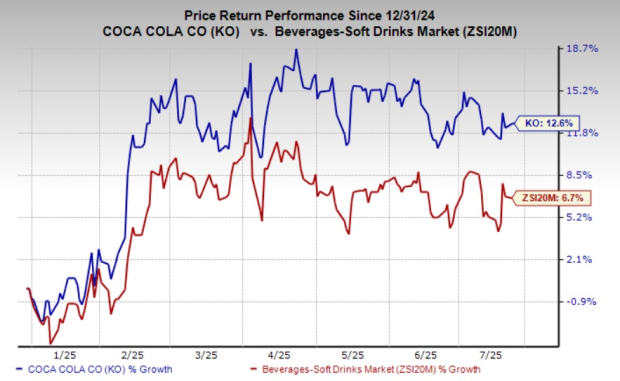

Shares of Coca-Cola dipped nearly 1% in the pre-market trading session following the mixed second-quarter results. The Zacks Rank #2 (Buy) stock has risen 12.6% in the year-to-date period compared with the industry’s growth of 6.7%.

In the reported quarter, concentrate sales were down 1% year over year, while the price/mix improved 6%. The price/mix benefited from pricing actions across the marketplace and a favorable mix. The impacts of high-inflation markets were lower in second-quarter 2025 compared with the same period last year.

In the second quarter, concentrate sales were in line with unit case volume. Coca-Cola’s total unit case volume fell 1% year over year in the second quarter, led by declines in Mexico, India and Thailand, which more than offset growth in Central Asia, Argentina and China.

Our model predicted year-over-year organic revenue growth of 4.9% for the second quarter, with a 5.8% gain from the price/mix and a 0.9% decline in the concentrate sales volume.

CocaCola Company (The) price-consensus-eps-surprise-chart | CocaCola Company (The) Quote

Coming to the cluster-category performance, the unit case volume dipped 1% year over year for the sparkling soft drinks category. The trademark Coca-Cola’s unit volume dropped 1%, led by a decline in Latin America, offset by growth in EMEA. Coca-Cola Zero Sugar advanced 14%, aided by growth in all geographic operating segments. The sparkling flavors category declined 2% year over year, backed by a decline in the Asia Pacific, offset by growth in EMEA.

Volume for juice, value-added dairy and plant-based beverages was down 4% in the second quarter, led by growth in the Asia Pacific, offset by an improvement in Latin America.

Unit volume for the water, sports, coffee and tea category was flat year over year in the second quarter. Coca-Cola witnessed flat volume growth in the water category, as improvement in EMEA and the Asia Pacific was fully offset by a decline in Latin America. Sports drinks fell 3%, driven by declines in Latin America, negated by gains in North America. The coffee business rose 1% due to growth in the Asia Pacific. The tea volume was flat, backed by growth in EMEA, offset by declines in North America.

Reported revenues rose 3% year over year each for North America and the Asia Pacific, and improved 5% for EMEA. However, revenues declined 4% for Latin America and 8% for Bottling Investments.

Organic revenues improved 13% year over year in Latin America, 3% in North America, 4% in EMEA and 5% in the Asia Pacific. Meanwhile, organic revenues were down 2% in Bottling Investments.

In dollar terms, the operating income surged 63% year over year to $4.28 billion, including a 6-point impact of currency headwinds. Comparable operating income rose 8.5% year over year to $4.38 billion. Comparable currency-neutral operating income advanced 15% on strong organic revenue growth across most segments, effective cost management and the timing of marketing investments.

The operating margin of 34.1% in the second quarter expanded significantly from 21.3% in the prior-year quarter. The comparable operating margin expanded 193 bps to 34.7%. The comparable currency-neutral operating margin expanded 325 bps to 36%.

Our model predicted the second-quarter adjusted operating margin to contract 10 bps year over year to 32.7%, driven by a 30-bps increase in the SG&A expense rate.

Management has reiterated its organic revenues guidance for 2025 and updated its EPS view. It anticipates organic revenue growth of 5-6% for 2025. Comparable net revenues are expected to include a 1-2% currency headwind based on current rates and hedge positions (compared with 2-3% currency headwind expected earlier). The guidance also includes a 1% negative impact of acquisitions, divestitures and structural changes. The company anticipates an underlying effective tax rate of 20.8% for 2025.

Comparable currency-neutral EPS for 2025 is expected to increase 8% year over year, at the mid-point of the prior-mentioned 7-9%. The company anticipates comparable EPS growth of 3% for 2025 from the $2.88 reported in 2024. The revised guidance is at the high-end of the prior mentioned 2-3%.

Comparable EPS growth is expected to include currency headwinds of 5% (compared with 5-6% headwind mentioned earlier). The EPS guidance also includes a 1% negative impact of acquisitions, divestitures and structural changes compared with a marginal impact mentioned earlier.

Management envisions an adjusted free cash flow of $9.5 billion for 2025, including $11.7 billion in cash flow from operations. Capital expenditure is likely to be $2.2 billion.

For third-quarter 2025, comparable revenues are expected to include a 1% currency headwind. Comparable EPS is estimated to include a 5-6% currency headwind.

We have highlighted three other top-ranked stocks from the Consumer Staples sector, namely Vita Coco Company COCO, Zevia ZVIA and Diageo DEO.

Vita Coco produces and sells coconut water products under the Vita Coco brand name in the United States, Canada, Europe, the Middle East, Africa, and the Asia Pacific. The company currently has a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for COCO’s 2025 earnings and sales indicates growth of 12.5% and 6.5%, respectively, from the previous year’s reported figures. Vita Coco has a trailing four-quarter average earnings surprise of 28.2%.

Zevia is focused on addressing health challenges resulting from excess sugar consumption by offering a portfolio of zero sugar, zero calorie, naturally sweetened beverages. It presently has a Zacks Rank #2.

The Zacks Consensus Estimate for Zevia’s 2025 sales and EPS indicates growth of 3.4% and 48.4%, respectively, from the prior-year reported levels. ZVIA delivered a trailing four-quarter earnings surprise of 33.6%, on average.

Diageo is involved in producing, distilling, brewing, bottling, packaging and distributing spirits, wine and beer. DEO currently has a Zacks Rank #2.

The Zacks Consensus Estimate for Diageo’s 2025 sales implies growth of 0.7% from the previous year’s reported numbers. Meanwhile, DEO’s earnings estimate indicates a year-over-year decline of 2.3%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite