|

|

|

|

|||||

|

|

|

Bristol Myers BMY recently collaborated with Bain Capital to create a new independent biopharmaceutical company, which will be focused on developing new therapies for autoimmune diseases that address significant unmet needs of patients.

Bain Capital will make a $300 million funding in the new company, while BMY will out-license five immunology candidates.

Among these, three are clinical stage candidates and two are phase I-ready pipeline candidates. Each of these targets promising mechanisms in autoimmune diseases. Out of these, the most advanced assets are afimetoran, an oral, potential best-in-class TLR7/8 inhibitor that is currently being studied in a phase II study for systemic lupus erythematosus (SLE), and BMS-986322, an oral TYK2 inhibitor, which successfully established proof-of-concept in a positive plaque psoriasis phase II study.

Other licensed assets include BMS-986326, a novel, potential best-in-class, IL2 fusion protein that is currently being studied in phase I studies for SLE and atopic dermatitis, and BMS-986481 and BMS-986498, two phase I-ready biologics targeting the IL18 and IL10 pathways, respectively.

Per the terms, BMY will retain a nearly 20% equity stake in the new company and be entitled to royalties and milestones tied to the success of each asset.

In addition, Robert Plenge, MD, PhD, executive vice president and chief research officer at BMY, will be part of the new company’s board of directors.

BMY is currently transitioning its portfolio as its key drugs face generic competition, thereby impacting top-line growth.

BMY’s growth portfolio primarily comprises Opdivo, Orencia, Yervoy, Reblozyl, Opdualag, Abecma, Zeposia, Breyanzi, Camzyos, Sotyku, Krazatiand others.

In the immunology space, BMY’s Sotyktufaces stiff competition from Amgen’s AMGN Otezla in the psoriasis space. Notably, Amgen acquired global commercial rights to Otezla from erstwhile Celgene (now part of Bristol-Myers). Amgen is also evaluating Otezla in additional indications.

This apart, oncology is a key focus area for BMY. space. However, BMY faces competition from large pharma companies like Merck MRK in this space. The immuno-oncology space is dominated by Merck’s blockbuster drug Keytruda (pembrolizumab).

Keytruda is approved for several types of cancer and alone accounts for around 50% of MRK’s pharmaceutical sales. Merck is currently working on different strategies to drive long-term growth of Keytruda.

Shares of Bristol Myers have lost 17.2% year to date against the industry’s growth of 0.6%.

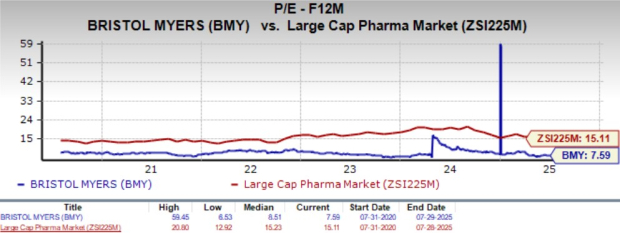

From a valuation standpoint, BMY is trading at a discount to the large-cap pharma industry. Going by the price/earnings ratio, BMY’s shares currently trade at 7.59x forward earnings, lower than its mean of 8.51x and the large-cap pharma industry’s 15.11X.

The bottom-line estimate for 2025 has moved down to $6.33 from $6.76 in the past 30 days and that for 2026 has declined 2 cents.

BMY currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 5 hours |

Bristol Myers, NVIDIA join forces to build life sciences most powerful AI factory

BMY

Pharmaceutical Technology

|

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite