|

|

|

|

|||||

|

|

|

Lumen Technologies, Inc. LUMN reported a second-quarter 2025 adjusted loss (excluding special items) of 3 cents per share, which was significantly narrower than the Zacks Consensus Estimate of a loss of 24 cents. The company reported adjusted loss per share of 13 cents in the prior-year quarter.

Quarterly total revenues were $3.092 billion, down 5% year over year and missed the Zacks Consensus Estimate by 1.1%. The top line was impacted by $46 million in one-time reimbursements related to the Rural Digital Opportunity Fund (“RDOF”).

Driven by significant AI-fueled connectivity demand, Lumen secured a total of $9 billion in PCF deals, up $500 million since the first quarter. As AI needs surge, large companies across various industries are urgently seeking fiber capacity, which is becoming highly valuable and potentially scarce. Lumen has inked deals with various tech giants like Microsoft, Amazon, Google Cloud and Meta Platforms to provide the network capabilities for AI innovation. The company also remains focused on “cloudifying” telecom and driving the adoption of its network-as-a-service solutions.

Among notable highlights, in the current year, LUMN now expects $350 million of run-rate cost benefit compared with $250 million targeted earlier. It continues to expect $1 billion of run-rate cost benefit exiting 2027. The company remains highly optimistic regarding the sale of Mass Markets' fiber-to-the-home business, including Quantum Fiber, across 11 states to AT&T T for $5.75 billion in cash. The transaction is expected to close in the first half of 2026, pending regulatory approvals and customary closing conditions.

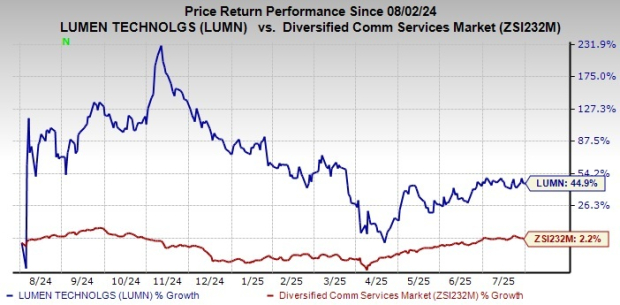

Following the results announcement, LUMN stock is down 5.5% in the pre-market session today. In the past year, shares of LUMN have jumped 44.9% compared with the Diversified Communications Services industry’s gain of 2.2%.

By segment, Business revenues fell 3.4% year over year to $2.49 billion, while revenues from Large Enterprises declined 2% to $732 million. Mid-Market Enterprise revenues declined 11% to $500 million. Public Sector revenues were up 8% to $486 million. Revenues of North America’s Enterprise Channels were down 2% to $1.718 billion. The metric for Wholesale decreased 5% to $690 million.

Revenues from Mass Markets were down 12.8% year over year to $602 million.

The company added 34,000 Quantum fiber subscribers, taking the count to 1.2 million in the reported quarter.

Lumen Technologies, Inc. Price, Consensus and EPS Surprise

Lumen Technologies, Inc. price-consensus-eps-surprise-chart | Lumen Technologies, Inc. Quote

In the second quarter, LUMN added 117,000 fiber broadband-enabled locations. As of June 30, 2025, the total enabled locations in the retained states were 4.4 million.

Total operating expenses increased 18% year over year to $3.695 billion.

Operating loss was $603 million against an operating income of $135 million in the year-ago quarter. Adjusted EBITDA (excluding special items) slipped to $877 million from $1.011 billion for respective margins of 28.4% and 30.9%.

In the second quarter, Lumen generated $570 million of net cash from operations compared with $511 million in the prior-year quarter.

Free cash outflow (excluding cash special items) for the second quarter was $209 million compared with an outflow of $156 million in the prior-year quarter.

As of June 30, 2025, the company had $1.6 billion in cash and cash equivalents with $17.565 billion of long-term debt compared with the respective figures of $1.9 billion and $17.334 billion as of March. 31, 2025.

Lumen completed a significant refinancing. With $2 billion of term loans refinanced, maturities have been pushed out to 2033, reducing annual interest expense by another $50 million.

For 2025, adjusted EBITDA is predicted to be between $3.2 billion and $3.4 billion, with LUMN expecting to report numbers near the high end of the range. This is mainly due to progress on M&S, improved cost controls and improved performance from legacy services. Adjusted EBITDA includes the impact from investments in transformation, higher startup costs for PCF sales and legacy revenue declines. LUMN expects EBITDA to rebound in 2026.

Capital expenditures to be between $4.1 billion and $4.3 billion, with LUMN expecting to report the numbers near the low end of the range. This is mainly due to project timings.

Free cash flow is now anticipated to be between $1.2 billion and $1.4 billion, up from the previous guidance of $700 million to $900 million. The guidance lift primarily stems from $400 million tax refund, lower capex, improved adjusted EBITDA performance and reduced interest expense. Management added that free cash flow would be lumpy from quarter to quarter as it moves through the PCF builds.

Lumen currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

AT&T reported strong second-quarter 2025 results with adjusted earnings and revenues beating the respective Zacks Consensus Estimate. The company recorded strong subscriber growth backed by a resilient business model and robust cash flow position, driven by a diligent execution of operational plans. AT&T expects to continue investing in key areas of 5G and fiber, and adjust its business according to the evolving market scenario to fuel long-term growth.

Excluding non-recurring items, adjusted earnings improved to 54 cents per share from 51 cents a year ago. Adjusted earnings per share for the second quarter beat the Zacks Consensus Estimate by 3 cents. Quarterly GAAP operating revenues increased 3.5% year over year to $30.85 billion, largely due to higher Mobility service and equipment sales and Consumer Wireline revenues, partially offset by lower Business Wireline and Mexico revenues. The top line beat the consensus mark of $30.53 billion.

Rogers Communications Inc RCI reported second-quarter 2025 adjusted earnings of 82 cents per share, which beat the Zacks Consensus Estimate by 2.5% but decreased 3.5% year over year. RCI’s revenues of $3.77 billion missed the consensus mark by 0.39% but increased 1.3% year over year. In domestic currency (Canadian dollar), adjusted earnings declined 1.7% year over year to C$1.14 per share. Total revenues increased 2.4% year over year, reaching C$5.22 billion, driven by service revenue growth in Wireless, Cable and Media businesses.

T-Mobile US, Inc. TMUS, a leading wireless service provider, reported better-than-expected second-quarter fiscal 2025 results. This Bellevue, WA-based wireless service provider reported a top-line expansion backed by industry-leading postpaid customer growth. T-Mobile follows a multi-layer approach to 5G, with dedicated standalone 5G deployed nationwide across 600 MHz, 1.9 GHz and 2.5 GHz bands.

Net sales were $21.13 billion, up from $19.77 billion in the year-ago quarter, driven by solid growth in service revenues. The top line beat the consensus estimate of $20.97 billion. Net income in the second quarter was $3.22 billion or $2.84 per share, up from $2.92 billion or $2.49 in the year-ago quarter. The 10.2% year-over-year growth was primarily driven by the top-line expansion. The bottom line beat the Zacks Consensus Estimate of $2.69.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

T-Mobile Earnings Beat, Revenue Light. CEO Shoots Down Expanded Starlink Deal.

TMUS -10.75%

Investor's Business Daily

|

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite