|

|

|

|

|||||

|

|

|

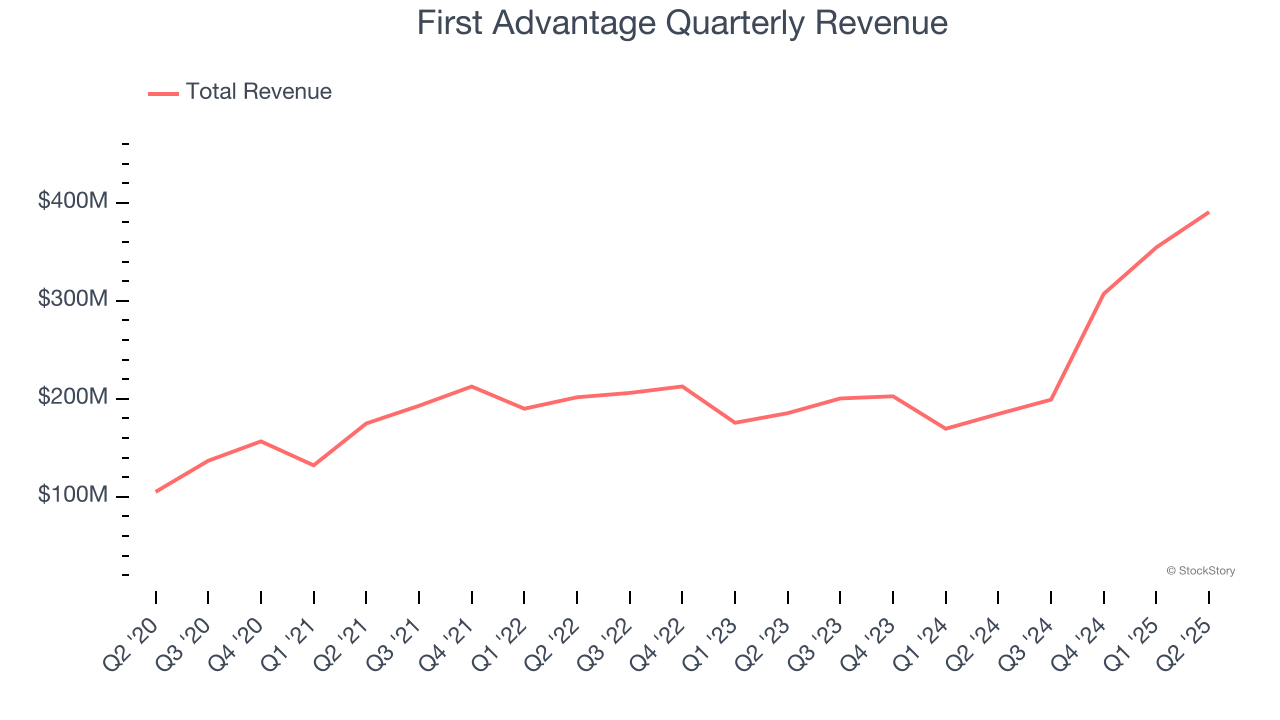

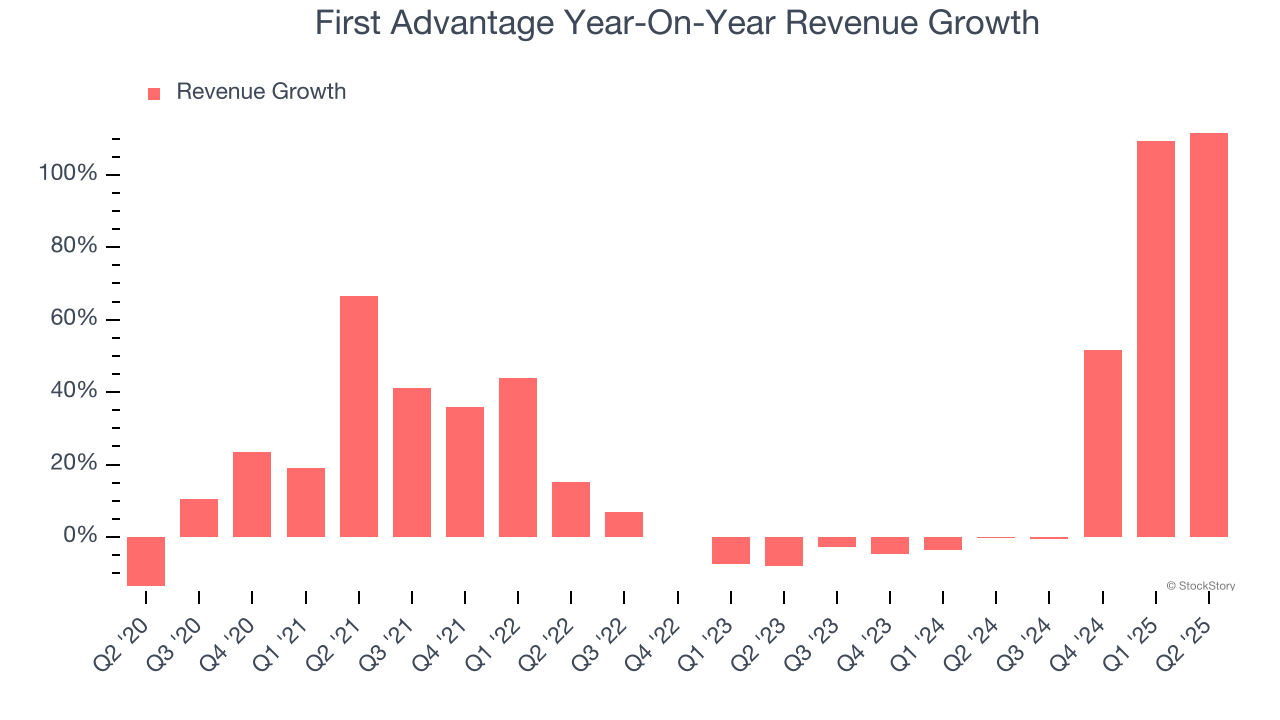

Background screening provider First Advantage (NASDAQ:FA) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 112% year on year to $390.6 million. The company’s full-year revenue guidance of $1.55 billion at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $0.27 per share was 13.8% above analysts’ consensus estimates.

Is now the time to buy First Advantage? Find out by accessing our full research report, it’s free.

“During the second quarter, we delivered solid financial performance at the top end of our previously stated expectations, despite continuing uncertainty within macroeconomic trends. Our balanced vertical strategy and market reach, combined with our consistent go-to-market execution, underpins the strength and resiliency of our business model. We continue to advance on our FA 5.0 strategic priorities, including seamlessly integrating our acquisition of Sterling and executing our best-of-breed product, data, and technology strategy. In addition, we are encouraged by continuing momentum in our international markets and are seeing strong customer interest in our Digital Identity solutions,” said Scott Staples, Chief Executive Officer.

Processing approximately 100 million background checks annually across more than 200 countries and territories, First Advantage (NASDAQ:FA) provides employment background screening, identity verification, and compliance solutions to help companies manage hiring risks.

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.25 billion in revenue over the past 12 months, First Advantage is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, First Advantage’s sales grew at an incredible 21.8% compounded annual growth rate over the last five years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. First Advantage’s annualized revenue growth of 26.7% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, First Advantage reported magnificent year-on-year revenue growth of 112%, and its $390.6 million of revenue beat Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to grow 25.1% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market sees success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

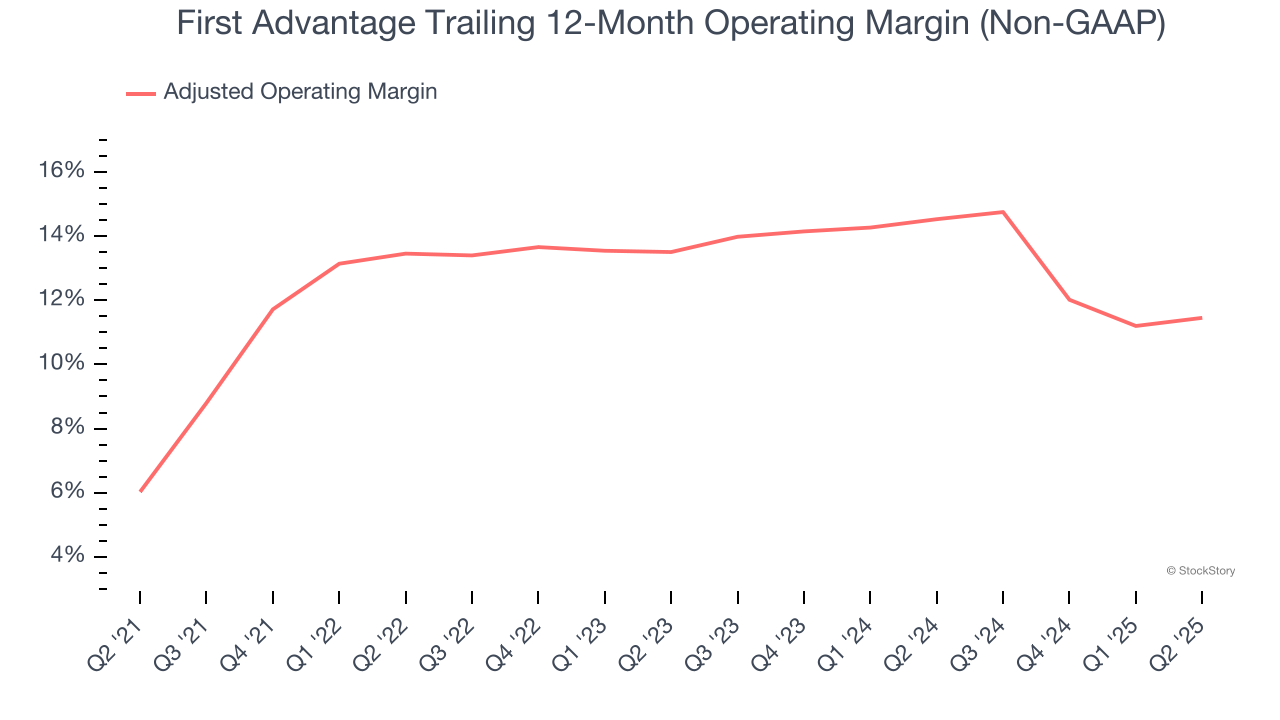

First Advantage has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 12%, higher than the broader business services sector.

Looking at the trend in its profitability, First Advantage’s adjusted operating margin rose by 5.4 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q2, First Advantage generated an adjusted operating margin profit margin of 13.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

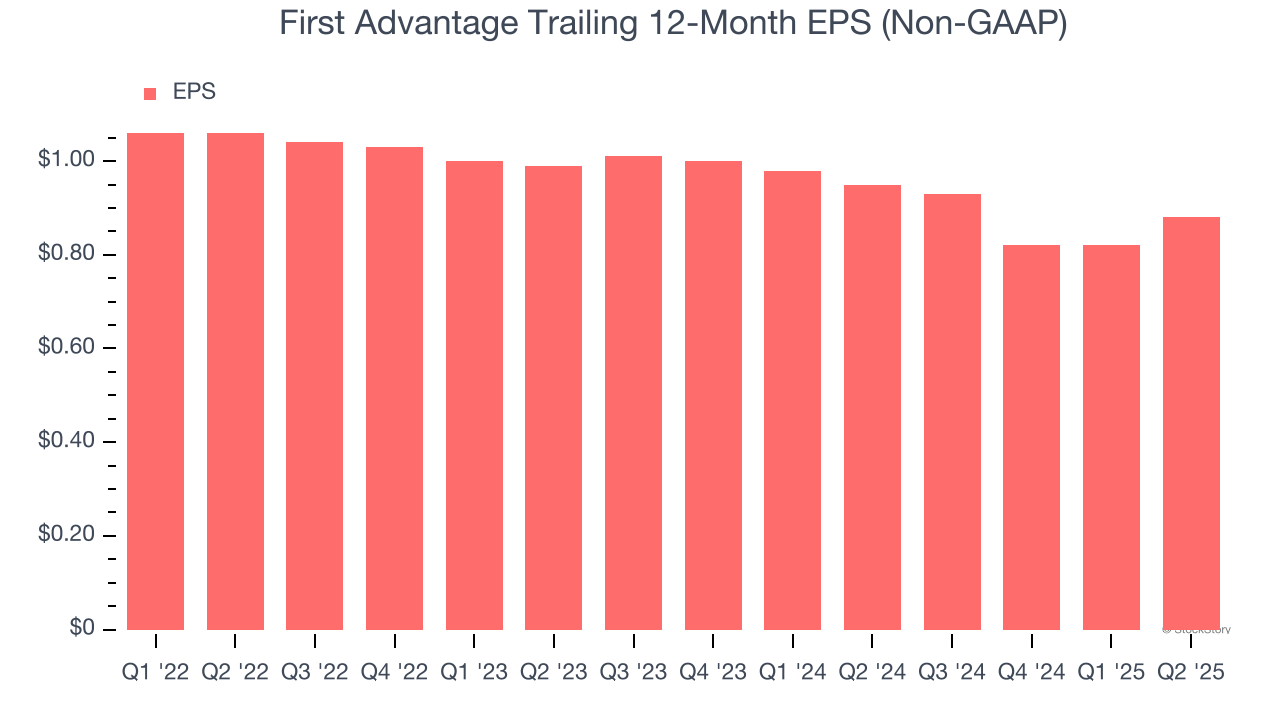

We track the change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for First Advantage, its EPS declined by 5.7% annually over the last two years while its revenue grew by 26.7%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

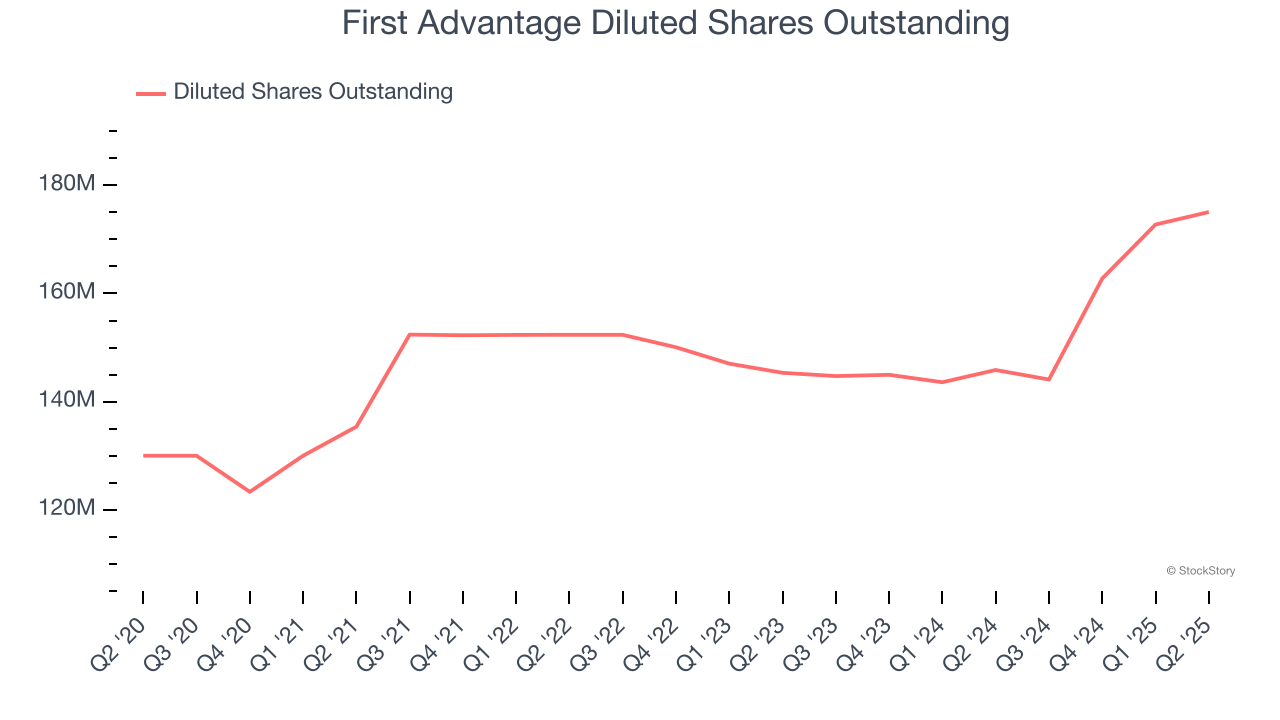

Diving into the nuances of First Advantage’s earnings can give us a better understanding of its performance. A two-year view shows First Advantage has diluted its shareholders, growing its share count by 20.5%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q2, First Advantage reported adjusted EPS at $0.27, up from $0.21 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects First Advantage’s full-year EPS of $0.88 to grow 17.5%.

We enjoyed seeing First Advantage beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 4.9% to $17.02 immediately after reporting.

First Advantage had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Jul-21 | |

| Jul-16 | |

| Jul-15 | |

| Jun-11 | |

| May-08 | |

| May-08 | |

| May-07 | |

| May-07 | |

| Apr-16 | |

| Mar-13 | |

| Mar-02 | |

| Feb-27 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite