|

|

|

|

|||||

|

|

|

EverQuote, Inc. EVER has been trading above its 200-day simple moving average (SMA), signaling a short-term bullish trend. Its share price as of Monday was $23.55, down 21.6% from its 52-week high of $30.03.

The 50-day SMA is a key indicator for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of an uptrend or downtrend.

Shares of EverQuote have gained 7.7% year to date, underperforming its industry, the sector, and the Zacks S&P 500 Composite’s growth of 12.6%, 20.4% and 20.3%, respectively, in the same time frame.

The insurer has a market capitalization of $859.8 million. The average volume of shares traded in the last three months was 0.4 million.

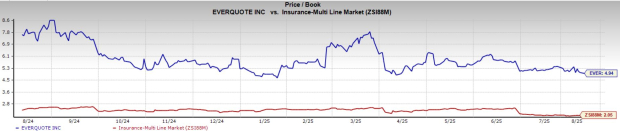

Shares ofEVER are trading at a premium to the Zacks Multi line industry. Its price-to-book value of 4.94X is higher than the industry average of 2.05X.

However, shares of other multi-line insurers, such as MGIC Investment Corporation MTG, Kemper Corporation KMPR and CNO Financial Group, Inc. CNO, are trading at a discount to the industry average.

The Zacks Consensus Estimate for EverQuote’s 2025 earnings per share indicates a year-over-year increase of 47.7% while the same for revenues is pegged at $644.9 million, implying a year-over-year improvement of 28.9%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 10.7% and 14.8%, respectively, from the 2025 estimates. EVER has an impressive Growth Score of A. This style score helps analyse the growth prospects of a company.

Analysts covering the stock have lifted estimates for 2025 and have raised the same for 2026 over the past seven days. The Zacks Consensus Estimate for 2025 earnings has moved up 10.2% in the past seven days, while the same for 2026 has moved up 5.7% in the same time frame.

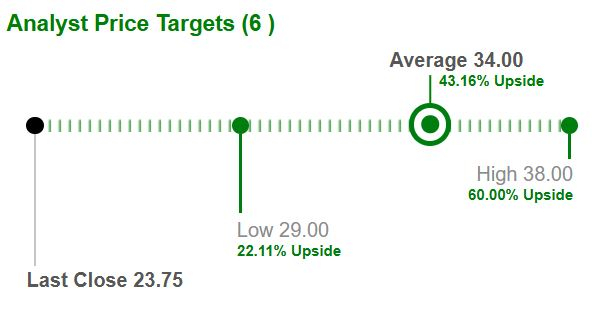

Based on short-term price targets offered by six analysts, the Zacks average price target is $34 per share. The average indicates a potential 43.2% upside from the last closing price.

Return on equity (ROE) for the trailing 12 months was 36.9%, comparing favorably with the industry’s 14.7%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing 12 months was 36.3%, better than the industry average of 2%, reflecting EVER’s efficiency in utilizing funds to generate income.

EverQuote continues to benefit from rising consumer quote requests, aided by higher volumes sourced through its verified partner network. The company is focused on sustaining this momentum by enhancing platform capabilities and expanding its data assets to draw more consumers over time. Broader advertising reach and richer data utilization, combined with quote and bind feedback, improve providers’ marketing efficiency, driving increased participation and ad spend. EverQuote believes it is well poised to benefit from the normalization of auto insurance carrier demand, given the auto carrier recovery.

The company anticipates VMD will benefit from strong revenue growth in the health direct-to-consumer agency during the annual health open enrollment period, supporting an improved operating point for the business.

While EverQuote has seen positive momentum, it continues to face several challenges. Expenses are rising due to the higher cost of revenues, sales and marketing, R&D, and G&A. The company competes in a crowded market against carriers and platforms across both offline and online channels. Competitive pressures, along with potential adverse regulatory changes, could weigh on revenue and growth, while compliance requirements may add further cost burdens.

EverQuote is seeing momentum from rising consumer traffic and stronger partner network volumes, with further gains anticipated from the health direct-to-consumer agency during the annual open enrollment period. The company also exhibits strong capital efficiency, outperforming industry averages in both return on equity and return on invested capital. However, rising costs, heightened competition, and regulatory risks limit near-term upside.

Given its expensive valuation, it is better to wait for some more time before taking a call on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-21 | |

| Jul-17 | |

| Jul-16 | |

| Jul-15 | |

| Jul-02 | |

| Jun-17 | |

| May-27 | |

| May-12 | |

| May-07 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite