|

|

|

|

|||||

|

|

|

When it comes to identifying potential short candidates or stocks to steer clear of, apparel brands are often high on my list. The industry is notoriously difficult, as consumer trends shift quickly, brand loyalty can be fleeting, and managing seasonal inventory is a constant balancing act. Even the strongest names stumble when demand softens or fashion trends miss the mark.

Carter’s (CRI), the well-known children’s apparel maker with numerous brands, is a clear example of these challenges in action. The company has been grappling with declining sales, a share price stuck in a prolonged downtrend, and now, a wave of downward revisions to its earnings estimates. These headwinds, combined with a tough retail environment, make Carter’s a stock that investors may want to avoid for now.

Headwinds Pressure CRI Sales and Margins

Carter’s also faces a difficult macro backdrop, with inflation, high interest rates, weak consumer confidence, and tariff uncertainty. First-quarter 2025 sales fell 4.8% year over year, with declines across US Retail (-4.3%), US Wholesale (-5.3%), and International (-4.9%) segments.

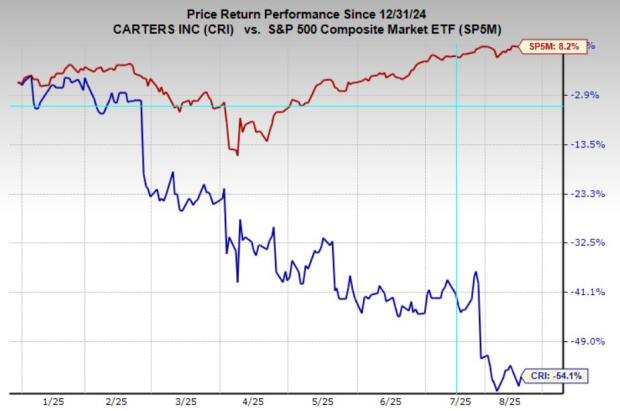

Margins also weakened and lower volumes drove gross margin down 140 bps and operating income down 35.7%. Tariffs remain a major cost challenge, particularly as most production is in Asia, leaving limited nearshoring alternatives. The stock underperforms the sector, which has struggled too.

Carter’s Stock Falls on Earnings Downgrades

Investor sentiment toward Carter’s has weakened further as analysts slash their earnings forecasts. Over the past month, estimates for the current quarter have been cut by 13.3%, while full-year 2025 projections have fallen 4.2%. Looking ahead, 2026 earnings estimates have dropped even more sharply, down 13.6%, which together gives the stock a Zacks Rank #5 (Strong Sell) rating.

On the top line, the outlook remains sluggish. Sales are now expected to decline 1.7% in 2025, followed by only a modest 0.9% rebound in 2026. This combination of downward earnings revisions and muted growth expectations underscores the headwinds facing the company and helps explain the recent weakness in the stock.

Should Investors Avoid CRI Stock?

Given the combination of falling sales, and persistent tariff and macroeconomic headwinds, Carter’s faces an uphill battle. The earnings downgrades signal that analysts remain cautious on the company’s near-term prospects, and the modest sales rebound projected for next year are unlikely to be enough to reignite investor enthusiasm.

With shares already underperforming both the broader market and the retail apparel sector, and visibility into a turnaround still limited, CRI appears positioned for continued pressure. Until there’s clear evidence of a sustainable recovery in demand and profitability, investors may be better served looking for opportunities elsewhere.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-08 | |

| Jun-25 | |

| Jun-17 | |

| Jun-17 | |

| Jun-15 | |

| Jun-10 | |

| May-14 | |

| May-13 | |

| May-13 | |

| May-07 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite