|

|

|

|

|||||

|

|

|

Pagaya Technologies Ltd. PGY posted positive net income for the second consecutive quarter in the three months ended June 30, 2025. PGY, one of the most compelling fintech companies in today’s market, posted a record GAAP net income of $16.7 million, which compared favorably with a net loss of $74.8 million incurred in the prior-year quarter.

Results were primarily aided by a 30% rise in total revenues and other income. Pagaya recorded revenues from fees of $317.7 million, which increased 31% year over year, driven by a rally in network AI fees. Improved economics in AI integration fees earned from certain partners, as well as 13.6% year-over-year growth in network volume to a record $2.6 billion, drove the rise in network AI fees. This was partially offset by a decrease in capital markets execution fees.

Contract fees increased 52.9% year over year to $31.8 million and interest income rose 31% to $10.7 million. However, investment loss increased by $1.6 million to $2.1 million in second-quarter 2025 because of an unfavorable impact of the change in valuation of certain proprietary investments.

Given the solid second-quarter 2025 results, PGY raised its 2025 revenue guidance. The company expects 2025 total revenues and other income between $1.25 billion and $1.325 billion, up from the previously mentioned $1.175-$1.3 billion. In 2024, total revenues and other income earned were $1.032 billion.

PGY’s competitors, LendingTree TREE and LendingClub LC, also posted solid second-quarter results. LendingTree’s adjusted EBITDA increased 35% year over year, fueled by strong revenue growth across all three business segments. LendingClub posted a 33% increase in total revenues, driven by higher marketplace sales and loan pricing, credit outperformance and higher net interest income on a larger balance sheet with lower deposit funding costs.

Given Pagaya’s strong performance, investors must be tempted to buy the stock. But, before making any investment decision, it is better to have a look at PGY’s fundamentals and growth prospects.

Diversified & Resilient Business Model: PGY’s core strength lies in its resilient and adaptable business model. The company has been actively expanding beyond its original focus on personal loans, moving into auto lending and point-of-sale financing. This diversification reduces exposure to cyclical risk in any single loan category, making the business more stable across economic cycles.

Parallel to this, Pagaya has built a robust network of more than 135 institutional funding partners to support the sale of its ABS. The company leverages forward flow agreements — structured financing arrangements in which institutional investors commit to purchasing future loan originations from Pagaya’s banking partners. These agreements offer a critical alternative funding source if ABS markets face disruptions during periods of market stress.

PGY has a competitive edge in its proprietary data and product suite. One standout offering is its pre-screen solution, which enables banks and lenders to present pre-approved loan offers to existing customers without requiring a formal application.

By analyzing the lender’s customer base and identifying qualified borrowers proactively, the company helps financial institutions deepen customer relationships and expand credit access with minimal incremental marketing spend. This marks an evolution in its value proposition from driving market share gains for partners to enhancing their share of wallet with existing customers.

Lean Balance Sheet: Pagaya operates a capital-efficient model that largely avoids holding loans on its balance sheet, significantly reducing its exposure to credit risk and market volatility. This is made possible through a robust network of institutional funding partners and a strategic focus on issuing ABS.

The capital raised in advance is held in trust and deployed only when a lending partner originates a loan through Pagaya’s AI-driven network. At that point, the loan is immediately acquired by a pre-committed funding source, either through an ABS vehicle or a forward flow agreement. As a result, most loans never reside on Pagaya’s balance sheet or only do so briefly before being transferred.

This off-balance-sheet model has proven particularly effective during periods of elevated interest rates and market stress, such as from 2021 through 2023. By minimizing credit exposure and avoiding significant loan write-downs, Pagaya has maintained its financial flexibility in turbulent environments.

PGY appears to rely heavily on forward flow agreements. These contracts provide a reliable and predictable source of capital, helping the company maintain liquidity even amid tightening credit markets and rising inflation.

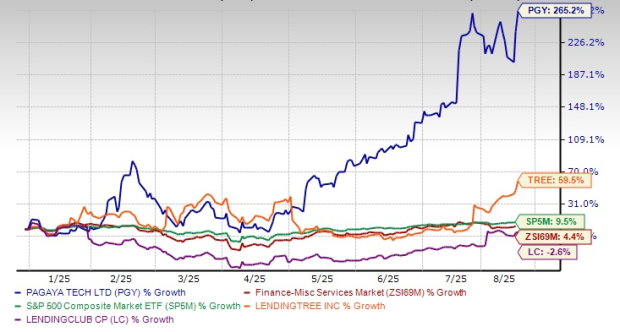

So far this year, PGY shares have skyrocketed 265.2%, outperforming the industry and the S&P 500 Index’s 4.4% and 9.5% rallies, respectively. The company’s performance has also been better than that of LendingTree and LendingClub.

LendingTree’s shares have soared 59.5%, while the LendingClub stock has lost 2.6% year to date.

Analysts seem optimistic regarding PGY’s earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for Pagaya’s 2025 and 2026 earnings has been revised upward to $2.51 and $3.18 per share, respectively. The estimated numbers indicate year-over-year growth rates of 202.4% and 26.7% for 2025 and 2026, respectively.

Given Pagaya’s impressive year-to-date performance, resilient business model and capital-efficient funding strategy, the company stands out in the fintech space. Its AI-driven platform, diversified revenue streams and reliance on forward flow agreements shield it from market volatility and credit risk.

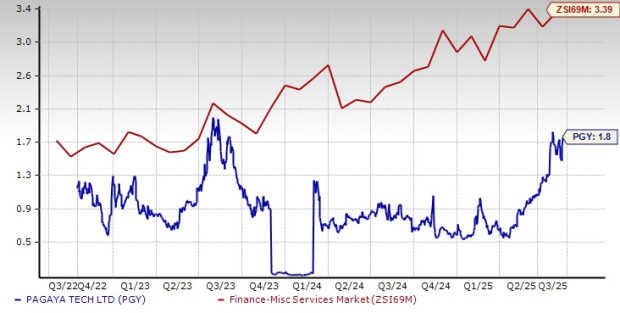

In terms of valuation, the PGY stock looks inexpensive. The stock is trading at a forward 12-month price/sales (P/S) ratio of 1.80X, below the industry average of 3.39X. However, Pagaya stock is trading at a premium compared with TREE and LC, which have forward P/S ratios of 0.78X and 1.72X, respectively.

Thus, the Pagaya stock looks like an attractive pick for investors seeking exposure to a high-growth, tech-enabled lender with solid fundamentals. Bullish analyst sentiments add another layer of optimism.

At present, Pagaya carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jun-30 | |

| Jun-15 | |

| Jun-11 | |

| Jun-11 | |

| Jun-10 | |

| Jun-08 | |

| Jun-02 | |

| Jun-02 | |

| Jun-01 | |

| Jun-01 | |

| May-27 | |

| May-27 | |

| May-26 | |

| May-21 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite