|

|

|

|

|||||

|

|

|

Flowers Foods, Inc. (FLO) reported second-quarter fiscal 2025 results. The top line increased year over year but missed the Zacks Consensus Estimate. The bottom line declined year over year but beat the consensus mark. Management revised its 2025 outlook, citing lower-than-expected second-quarter sales, ongoing bread category pressures and intense competition.

Flowers Foods posted adjusted quarterly earnings per share (EPS) of 30 cents, beating the Zacks Consensus Estimate of 29 cents. However, the bottom line decreased from 36 cents reported in the year-ago quarter.

Flowers Foods, Inc. price-consensus-eps-surprise-chart | Flowers Foods, Inc. Quote

Sales of $1,242.8 million missed the Zacks Consensus Estimate of $1,269 million and rose 1.5% year over year. Price/mix declined 1.2%, volumes dropped 2.4% and the Simple Mills acquisition added 5.1%. We estimated the price/mix to be up 0.6% and volumes to decline 2% in the second quarter.

Branded retail sales inched up 5% to $826.7 million, driven by contributions from the acquisition, partially offset by an unfavorable price/mix and lower volumes. Price/mix inched down 1.5%, sales volume decreased 1.3% and the Simple Mills acquisition contributed 7.8%. We anticipated the price/mix to be down 1.3% and volumes to decline 2% in the fiscal second quarter.

Other sales decrease 4.9% to $416.1 million, impacted by softer volumes in store-branded retail sales and non-retail sales resulting from the execution of non-retail margin optimization strategies. Price/mix declined 1.2% and volume declined 3.7%. We estimated price/mix to be up 4% and volume to decline 2% in the fiscal second quarter.

Materials, supplies, labor and other production costs (exclusive of depreciation and amortization) increase 110 basis points (bps) to 51.2% of net sales. This improvement was driven by increased outside product purchases and lower production volumes, partly offset by lower ingredient and workforce-related costs.

Selling, distribution and administrative (SD&A) expenses were 38.1% of sales, down 40 bps. The decrease in SD&A costs as a percentage of net sales was due to lower distribution fees. These were partially offset by higher workforce-related expenses and fleet expense largely related to the California conversion. Adjusted SD&A expenses were 37.7% of sales, down 50 bps from the year-ago quarter.

Adjusted EBITDA decreased 4% to $137.7 million. The adjusted EBITDA margin was 11.1%, down 60 bps. We anticipated an adjusted EBITDA margin decrease of 90 bps to 10.8% for the quarter under review.

FLO ended its fiscal second quarter with cash and cash equivalents of nearly $11 million and long-term debt of $1,749.2 million. Stockholders’ equity at the quarter end was $1,427.8 million.

In the fiscal second quarter, cash flow from operating activities totaled $130.8 million and capital expenditures were $30.8 million. The company paid out dividends worth $52.4 million during this time.

For fiscal 2025, management now expects net sales in the range of $5.239-$5.308 billion, indicating a 2.7% to 4% increase year over year. This forecast is revised from the previous guidance of $5.297-$5.395 billion, implying a 3.8% to 5.7% increase year over year.

Adjusted EBITDA is likely to be in the range of $512-$538 million compared with $534-$562 million projected earlier and $538.5 million recorded in fiscal 2024.

For fiscal 2025, adjusted EPS is envisioned in the range of $1.00-$1.10 compared with the earlier view of $1.05-$1.15 and $1.28 delivered in fiscal 2024.

Management expects depreciation and amortization in the range of $168-$172 million, while net interest expenses are likely to be $58-$62 million. For fiscal 2025, capital expenditures are expected in the range of $135-$145 million.

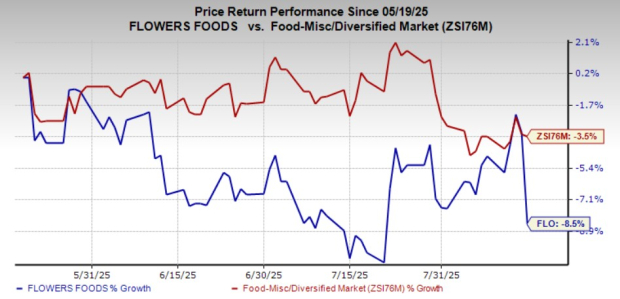

This Zacks Rank #4 (Sell) stock has lost 8.5% in the past three months compared with the industry’s decline of 3.5%.

Post Holdings, Inc. (POST) operates as a consumer-packaged goods holding company in the United States and internationally. It currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Post Holdings’ current fiscal-year sales and earnings indicates growth of 3.1% and 10.9%, respectively, from the prior-year levels. POST delivered a trailing four-quarter earnings surprise of 21.4%, on average.

Smithfield Foods, Inc. (SFD) produces packaged meats and fresh pork in the United States and internationally. It flaunts a Zacks Rank #1 at present. SFD delivered a trailing four-quarter earnings surprise of 6.6%, on average.

The Zacks Consensus Estimate for Smithfield Foods’ current fiscal-year sales and earnings indicates growth of 7.1% and 28.7%, respectively, from the prior-year levels.

The Chefs' Warehouse, Inc. (CHEF) distributes specialty food and center-of-the-plate products in the United States, the Middle East and Canada. It currently carries a Zacks Rank of 2 (Buy). CHEF delivered a trailing four-quarter earnings surprise of 11.3%, on average.

The Zacks Consensus Estimate for The Chefs' Warehouse’s current fiscal-year sales and earnings indicates growth of 6.4% and 19.1%, respectively, from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-21 | |

| Jul-16 | |

| Jul-15 | |

| Jul-07 | |

| Jul-06 | |

| Jun-15 | |

| May-25 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-21 | |

| May-21 | |

| May-21 | |

| May-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite