|

|

|

|

|||||

|

|

|

Shares of Palomar Holdings, Inc. PLMR have gained 18.4% in the past year, outperforming its industry and the Finance sector’s growth of 6.4% and 18.2%, respectively. It, however, underperformed the Zacks S&P 500 composite’s growth of 18.8%.

The insurer has a market capitalization of $3.10 billion. The average volume of shares traded in the last three months was 0.3 million.

Palomar Holdings beat earnings estimates in each of the past four quarters, with an average surprise of 14.71%.

Its shares are trading at a premium to the Zacks Property and Casualty Insurance industry. Its price-to-book value of 3.66X is higher than the industry average of 1.55X.

Shares of other insurers like The Allstate Corporation ALL, W.R. Berkley Corporation WRB, and The Progressive Corporation PGR are also trading at a multiple higher than the industry average.

The Zacks Consensus Estimate for Palomar Holdings’ 2025 earnings per share indicates a year-over-year increase of 42.6%. The consensus estimate for revenues is pegged at $807.24 million, implying a year-over-year improvement of 46.9%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 15.9% and 27.4%, respectively, from the corresponding 2025 estimates.

PLMR has an impressive Growth Score of B. This style score helps analyze the growth prospects of a company.

Four of the six analysts covering the stock have raised estimates for 2025, and three of the five analysts have raised the same for 2026 over the past 60 days. Thus, the Zacks Consensus Estimate for 2025 and 2026 earnings has moved up 1.9% and 0.3%, respectively, in the past 60 days.

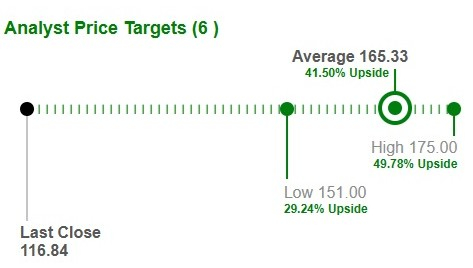

Based on short-term price targets offered by six analysts, the Zacks average price target is $165.33 per share. The average suggests a potential 41.5% upside from the last closing price.

Return on equity is a measure of profitability reflecting how efficiently the company is utilizing its shareholders’ equity. Return on equity of 20.3% compared favorably with the industry’s average of 7.6%.

Also, the return on invested capital in the trailing 12 months was 19.6%, better than the industry average of 5.9%, reflecting the company’s efficiency in utilizing funds to generate income.

Palomar’s fee-based platform, PLMR-FRONT, is positioned to drive medium-term growth. The addition of this revenue stream is expected to strengthen its earnings foundation.

The increasing volume of policies across multiple business lines, strong retention rates, expansion into new geographic areas and distribution channels, and the formation of new partnerships are expected to drive premiums. Palomar Holdings also projects that crop insurance will contribute around $200 million in premiums by 2025.

PLMR identifies Surety as an attractive, long-term growth opportunity. Like crop insurance, Surety is not correlated with the traditional property and casualty insurance cycle, offering diversification and stability.

Net investment income is expected to rise, supported by a high-quality fixed-income portfolio, higher average investment balances, and improved yields. This solid investment base is poised to generate strong returns.

Palomar Holdings’ risk transfer strategy reduces exposure to major catastrophic events, helping to stabilize earnings and improve its combined ratio.

Financially, the insurer maintains a strong capital position and a debt-free balance sheet. As part of its shareholder return initiatives, Palomar Holdings continues to execute share buybacks.

With these strengths in place, Palomar Holdings expects 2025 adjusted net income of $198 million to $205 million 2025, which includes an estimate of $8 million to $12 million of catastrophe losses.

Palomar Holdings is positioning itself as a key player in the crop insurance sector, with its growing emphasis on Surety signaling strong prospects for future expansion. The company’s diverse product suite, ongoing geographic growth, onboarding of new producers, strategic partnerships with other insurers, and implemented rate increases are all poised to fuel its momentum.

As a specialty insurer, PLMR leverages reinsurance to effectively mitigate risk exposure. This strategy enables the company to underwrite policies with sufficient coverage while managing potential losses, contributing to a stable and resilient business model. The stock also has a VGM Score of B. The VGM Score helps identify stocks with the most attractive value, best growth, and the most promising momentum.

Its solid growth projections, as well as strong fundamentals and favorable return on capital, are other positives. Given Palomar Holdings' premium valuation, it is better to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-09 | |

| Jul-08 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jul-01 | |

| Jun-29 | |

| Jun-25 | |

| Jun-25 | |

| Jun-22 | |

| Jun-18 | |

| Jun-18 | |

| Jun-17 | |

| Jun-17 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite