|

|

|

|

|||||

|

|

|

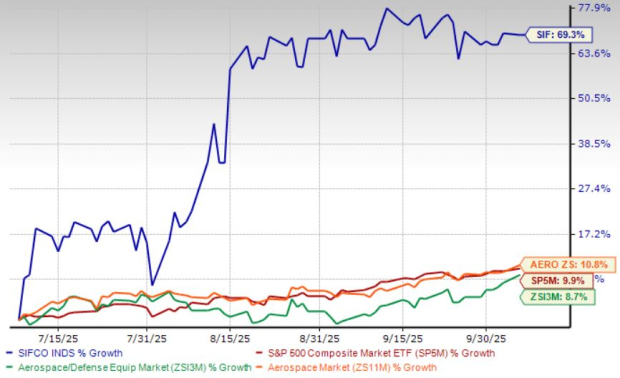

SIFCO Industries, Inc.’s SIF investors have been experiencing some short-term gains from the stock of late. Shares of the Cleveland, OH-based manufacturer of forgings, sub-assemblies and machined components (primarily serving the aerospace and energy or A&E markets) have gained 69.3% in the past three months compared with the industry’s 8.7% rise. The stock also outperformed the sector and the S&P 500’s 10.8% and 9.9% gains, respectively, in the same time frame.

A major development of SIF in recent months includes the announcement of its promising third-quarter fiscal 2025 results in August. The company delivered a notable upswing in both revenue and earnings during the fiscal third quarter. The company achieved a sharp turnaround in profitability, even though sales edged up only slightly, reflecting meaningful operational efficiencies and disciplined cost management.

Per management, the demand for SIFCO’s forged and machined components stayed resilient throughout the quarter as A&E sector customers ramped up production. Although the supply of raw materials improved versus prior periods, certain supply-chain issues continued to limit shipment volumes.

Over the past three months, the stock’s performance has remained strong, outperforming that of its peers like Optex Systems Holdings, Inc OPXS and Park Aerospace Corp. PKE. Optex and Park Aerospace’s shares have gained 5.1% and 30.3%, respectively, in the same time frame.

Despite several challenges within the aerospace industry, including widespread supply chain weaknesses and the complexities of navigating rapid digitalization and new technologies, the favorable share price movement indicates that the company might be able to maintain its positive market momentum at present.

SIFCO specializes in forging, heat-treating, chemical processing and machining services, catering to original equipment manufacturers (OEMs), Tier 1 and Tier 2 suppliers and aftermarket service providers. These multiple growth drivers reflect robust growth potential.

SIFCO continues to benefit from steady demand in its core A&E markets. Management emphasized that customers across these segments — particularly aerospace and defense — are ramping up production, which has sustained strong orders for SIF’s forged and machined components. Its specialized manufacturing capabilities and established relationships with key OEMs and Tier-1 suppliers provide a competitive edge as these industries continue their multi-year recovery cycle.

SIF’s recent results reflect substantial progress in driving efficiency across operations. Through tighter cost control, improved product mix and disciplined management of overhead expenses, SIFCO achieved stronger margins despite limited top-line growth. Initiatives like the sale of non-core European operations and the consolidation of production activities have helped streamline its structure, reduce fixed costs and enhance overall profitability. This operational focus positions SIFCO to better leverage future increases in demand.

SIFCO has seen notable improvements in raw material availability compared to earlier periods, which has eased production bottlenecks. At the same time, management reported constructive pricing discussions with customers, supporting a more stable revenue outlook. This combination of improved supply reliability and strengthened pricing dynamics enhances visibility into future quarters and suggests better resilience against cost fluctuations and supply disruptions.

SIFCO continues to encounter supply-chain and cost pressures, as volatility in raw material prices and the availability of skilled labor present ongoing challenges to maintaining production efficiency and margin stability. Although material availability has improved, disruptions in logistics and higher input costs remain key risks. Moreover, SIF’s reliance on a small number of major A&E customers heightens concentration risk — any reduction, delay or cancelation of orders from these core clients could significantly affect revenue visibility and earnings consistency.

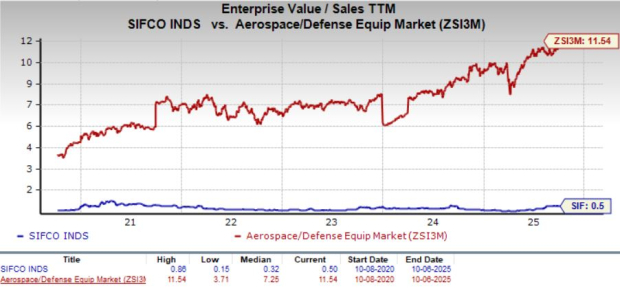

SIFCO’s trailing 12-month EV/Sales of 0.5X is lower than the industry’s average of 11.5X but higher than its five-year median of 0.3X.

Optex and Park Aerospace’s trailing 12-month EV/Sales currently stand at 2.2X and 5.2X, respectively, in the same time frame.

There is no denying that SIFCO sits favorably in terms of core business strength, earnings prowess, robust financial footing and global opportunities. The stock’s strong core growth prospects present a good reason for existing investors to retain shares for potential future gains. New investors may get motivated to add the stock following the current uptrend in share prices.

For those exploring to make new additions to their portfolios, the valuation indicates superior performance expectations compared with its industry peers. It is still valued lower than the industry, which suggests potential room for growth if it can align more closely with overall market performance. However, if investors are already holding the stock, it would be prudent to hold on to it at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-16 | |

| Jul-10 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 | |

| May-29 | |

| May-28 | |

| May-20 | |

| May-14 | |

| May-12 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite