|

|

|

|

|||||

|

|

|

Shares of NIKE Inc. NKE have lost momentum in recent months, pushing it below industry thresholds and portraying a bearish sentiment from a technical standpoint. As a result, the NKE stock slipped below its 200-day simple moving average (SMA) yesterday. Notably, the stock closed at $68.91 on Oct. 8, 2025, moving below the 200-day SMA of $69.13.

A drop below the 200-day SMA typically signals weakness, suggesting a shift from long-term bullish to bearish sentiment. It highlights fading investor confidence and slower buying interest, especially after months of underperformance.

Additionally, the sportswear behemoth sloped below its 50-day SMA on Sept. 5, 2025, and continues to trade below the mark since then, indicating a short-term downward trend.

SMA is an essential tool in technical analysis that helps investors evaluate price trends by smoothing out short-term fluctuations. This approach also provides a clearer perspective on a stock's long-term direction.

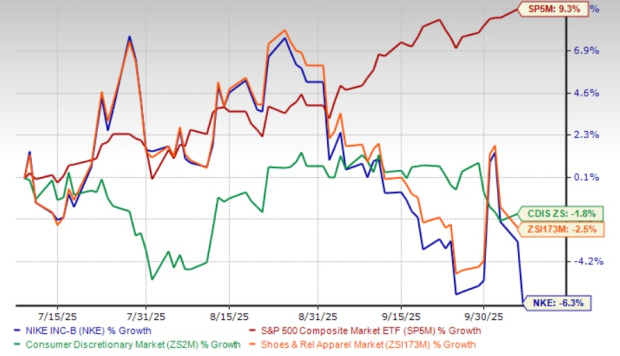

NIKE has shown a lackluster performance, with its shares losing 6.3% in the past three months compared with the Zacks Shoes and Retail Apparel industry’s decline of 2.5%. The NKE stock has also underperformed the broader Zacks Consumer Discretionary sector’s fall of 1.8% and the S&P 500's growth of 9.3% in the same period.

NKE’s performance is notably weaker than that of its competitors, Wolverine World Wide WWW and Steven Madden SHOO, which have rallied 29% and 30.2%, respectively, in the past three months. However, the NKE stock has outperformed adidas AG’s ADDYY decline of 12.8% in the same period.

At its current price of $68.91, the NKE stock trades 31.8% above its 52-week low mark of $52.28 and 18.7% below its 52-week high mark of $84.76.

NIKE’s first-quarter fiscal 2026 results underscored the depth of its ongoing transition, as the company navigates a strategic reset amid weakening consumer demand and intensified competition. The “Win Now” strategy, aimed at rebalancing the product mix away from aging classics like Air Force 1, Dunk and Jordan 1 toward innovation-led performance products, continues to weigh on near-term results. This portfolio shift, while strategically sound, has created a multibillion-dollar revenue headwind as NIKE clears aged inventory through value channels to restore full-price momentum.

In the fiscal first quarter, revenue declines were particularly pronounced in North America and Greater China, both critical markets under pressure from promotional activity, macroeconomic softness and local brand competition. Digital traffic fell in the double-digits in the fiscal first quarter as NIKE repositioned its online platforms toward premium, full-price offerings. The gross margin contracted further, reflecting elevated discounting, channel mix headwinds and the early impacts of newly imposed U.S. tariffs on China-sourced footwear.

Meanwhile, SG&A expenses rose due to sustained investment in demand creation and marketplace activations, limiting operating leverage. Management emphasized that these elevated costs are vital to reigniting brand energy and strengthening wholesale relationships, even at the expense of short-term profitability. Despite ongoing softness in lifestyle franchises and cautious consumer spending, bright spots emerged in performance categories like Running and Global Football.

Overall, NIKE’s dismal quarter reflects deliberate short-term pain for long-term gain. By resetting its marketplace, restoring pricing power and focusing on sport-led innovation, NIKE aims to rebuild sustainable growth momentum beyond fiscal 2026.

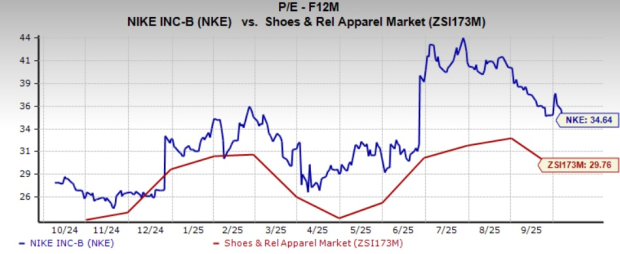

While NIKE remains fundamentally strong, backed by its decisive actions to reposition itself for sustainable and profitable long-term growth, its current forward 12-month price-to-earnings (P/E) multiple of 34.64X raises concerns about whether the stock's valuation is justified. This multiple is higher than the Zacks Shoes and Retail Apparel industry average of 29.76X and the S&P 500’s average of 23.65X, making the stock appear relatively expensive.

At 34.64X P/E, the Swoosh brand owner is trading at a much higher valuation than its competitors. Its peers, such as Wolverine, Steven Madden and adidas, are delivering solid growth and trade at more reasonable multiples. Wolverine, Steven Madden and adidas have forward 12-month P/E ratios of 16.45X, 18.84X and 19.41X — all significantly lower than NIKE. At such levels, NKE’s valuation seems out of step with its growth trajectory, especially given the recent decline in its stock price.

The stock's elevated valuation reflects high investor expectations for growth. However, NIKE looks increasingly vulnerable in an environment wherein market participants are growing cautious about overpriced Consumer Discretionary stocks. The company’s ability to meet or exceed these lofty expectations is crucial in justifying its premium pricing.

Despite near-term turbulence, NIKE’s underlying fundamentals remain resilient. The company continues to leverage its global scale, powerful brand equity and innovation engine to navigate a period of strategic reset. Management’s disciplined approach, managing down aged franchises, streamlining inventory and refocusing on performance-led products, reflects a long-term vision centered on restoring pricing power and profitability. Growth in key categories like Running, Global Football and Women’s underscores NIKE’s ability to reignite consumer engagement through sport and innovation.

NIKE retains strong balance sheet flexibility and operational discipline to absorb short-term shocks. While margins remain under pressure from promotional activity, tariffs and elevated SG&A, the company is positioning itself for healthier growth through cleaner inventories, improved product freshness and expanded wholesale partnerships. As the product pipeline strengthens and demand creation investments take hold, NIKE’s structural advantages may drive a durable rebound once market conditions stabilize.

The Zacks Consensus Estimate for NIKE’s fiscal 2026 and 2027 EPS moved up 1.2% and 0.8%, respectively, in the last 30 days. For fiscal 2026, the Zacks Consensus Estimate for NKE’s revenues implies 0.2% year-over-year growth, while the estimate for EPS suggests a 23.2% decline. The consensus mark for fiscal 2027 revenues and earnings indicates 5.7% and 56.4% year-over-year growth, respectively.

NIKE’s stock currently reflects a delicate balance between optimism about its long-term strategic reset and skepticism about its near-term execution risks. While management’s focus on innovation, cleaner inventories and a performance-driven product mix lays the groundwork for sustainable growth, the company’s short-term outlook remains clouded by soft consumer demand, margin pressure and elevated valuation levels. Trading below both its 50 and 200-day moving averages, NKE continues to exhibit bearish technical momentum, suggesting investor sentiment remains cautious.

Given its premium forward P/E multiple, significantly higher than peers, NIKE appears richly valued relative to its earnings trajectory. Although fundamentals such as brand equity and balance sheet strength provide support, the lack of near-term growth visibility tempers the bullish case. For now, investors may be better served by waiting for signs of revenue stabilization and margin recovery before taking a fresh position, as the stock is likely to remain range-bound in the near term.

The company currently has a Zacks Rank #3 (Hold). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite