|

|

|

|

|||||

|

|

|

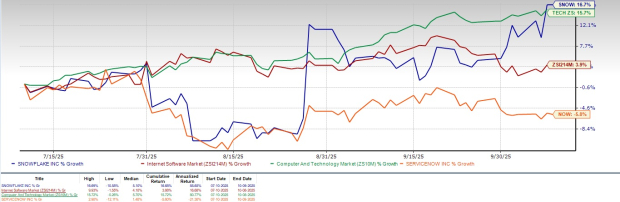

Snowflake SNOW shares have soared 16.7% in three months, outperforming the Zacks Computer and Technology sector’s growth of 15.7% and the Zacks Internet Software industry’s increase of 3.9% over the same time frame.

The company’s shares have also outperformed its peers, including ServiceNow NOW, which is also expanding its presence in enterprise-grade AI workflows. ServiceNow shares have lost 5.8% in the past three months.

The outperformance in SNOW stock is driven by its strong portfolio and an expanding partner base. The company also benefits from strong adoption and increasing usage of its platform, as reflected by the net revenue retention rate of 125% in the second quarter of fiscal 2026.

Snowflake reported 19% year-over-year growth in the number of customers, reaching 12,062 in the second quarter of fiscal 2026. The company now has 654 customers with trailing 12-month product revenues greater than $1 million and 751 Forbes Global 2000 customers.

Snowflake’s expanding portfolio has been a significant growth driver. The company launched approximately 250 new capabilities in the first half of fiscal 2026, including Snowflake Intelligence, Cortex AI SQL, Gen2 warehouses, Snowflake Postgres and Snowflake OpenFlow. These innovations simplify data management, enhance performance and enable AI-driven insights.

Snowflake’s investments in artificial intelligence and machine learning, including the introduction of Cortex AI and its integration with models from OpenAI and Anthropic, drove customer engagement. In the second quarter of fiscal 2026, the company announced that more than 6,100 customers are using Snowflake’s AI and ML technology weekly.

Further expanding its portfolio and building on this momentum, SNOW recently launched Cortex AI for Financial Services and a managed Model Context Protocol Server, enabling financial institutions to securely deploy AI models, agents and apps using unified proprietary and third-party data within Snowflake’s AI Data Cloud.

SNOW’s strong partner base, which includes major players like Microsoft MSFT, Amazon’s cloud computing platform Amazon Web Services (AWS), NVIDIA, Meta Platform, ServiceNow, Fiserv, EY, LTMindtree, Next Pathway, and S&P Global, has been a significant growth driver of its success.

Snowflake’s collaboration with OpenAI, Anthropic and Microsoft Azure is expanding its reach and enhancing its AI capabilities. Microsoft Azure was the fastest-growing cloud for Snowflake, with 40% year-over-year growth in the second quarter of fiscal 2026.

Snowflake’s rich partner base, expanding clientele and an innovative portfolio are expected to drive the company’s top-line growth.

For the third quarter of fiscal 2026, Snowflake expects product revenues in the range of $1.125-$1.13 billion. The projection range indicates year-over-year growth between 25% and 26%. The operating margin is expected to be 9% for the fiscal third quarter.

The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is currently pegged at $1.18 billion, indicating 25.27% year-over-year growth. The consensus mark for earnings is currently pegged at 31 cents per share, which has remained unchanged over the past 30 days. This suggests an increase of 55% year over year.

Snowflake Inc. price-consensus-chart | Snowflake Inc. Quote

Snowflake is facing stiff competition from the likes of Amazon AMZN in the AI Data Cloud space. The company, through its respective cloud platform, Amazon Web Services (AWS), offers compelling solutions that directly compete with Snowflake’s offerings.

Amazon is expanding its footprint with Redshift, its fully managed, petabyte-scale cloud data warehouse service offered by Amazon Web Services (AWS), to provide faster analytics and seamless SQL-based integration for enterprise customers.

Snowflake shares are currently overvalued, as suggested by its Value Score of F.

The SNOW stock is trading at a premium with a forward 12-month Price/Sales of 15.98X compared with the Internet Software industry’s 5.49X, and ServiceNow’s 12.69X.

Despite SNOW’s robust portfolio, stiff competition from hyperscale cloud providers remains a headwind. Stretched valuation also remains a concern.

Elevated infrastructure spending, particularly on GPUs to support AI-driven initiatives, is adding to cost pressures. Snowflake now expects non-GAAP operating margin to be 9%, suggesting a 200-bps sequential decline.

SNOW currently carries a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point in the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 34 min | |

| 42 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite