|

|

|

|

|||||

|

|

|

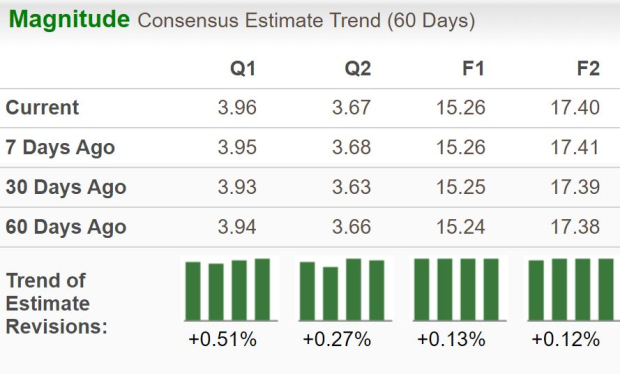

American Express Company AXP is set to report third-quarter 2025 results on Oct. 17, 2025, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $3.96 per share and the same for revenues is pinned at $17.99 billion.

The third-quarter earnings estimate witnessed three upward revisions over the past 60 days against one downward movement. The bottom-line prediction indicates a year-over-year increase of 13.5%. The Zacks Consensus Estimate for quarterly revenues implies year-over-year growth of 8.2%.

For the full-year 2025, the Zacks Consensus Estimate for AmEx’s revenues is pegged at $71.41 billion, implying a rise of 8.3% year over year. Meanwhile, the consensus mark for the current year EPS is pegged at $15.26, implying growth of 14.3% on a year-over-year basis.

AmEx beat the consensus estimate in each of the last four quarters, with the average surprise being 4.6%.

American Express Company price-eps-surprise | American Express Company Quote

However, our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is not the case here.

AXP has an Earnings ESP of -0.77% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

American Express is expected to have witnessed a rise in network volumes during the third quarter, continuing the trend. This uptick is likely attributable to the resilient consumer spending of AXP’s premium customer base, which is less impacted by economic volatilities. The Zacks Consensus Estimate for third-quarter total network volumes indicates 7.4% year-over-year growth from $441 billion.

Discount revenues, a key source of revenues for AmEx, are likely to have benefited from rising network volumes. The Zacks Consensus Estimate for third-quarter Discount revenues indicates 6.6% year-over-year growth. Billed businesses in U.S. Consumer Services and Commercial Services are expected to witness growth of 8% and 2.3% year over year, respectively.

Cards-in-force are likely to have witnessed an uptick in the quarter under review due to expanding product offerings and enhancing mobile platforms, which improve the customer experience. The Zacks Consensus Estimate for third-quarter total cards-in-force indicates 4% year-over-year growth. The consensus estimate for Average Card Member loans also implies an 8.2% year-over-year increase.

AmEx’s interest income, another major revenue contributor, is likely to have risen on higher loan receivables. The Zacks Consensus Estimate for AXP’s net interest income implies an upside of 7.9% from the year-ago reported figure.

The factors mentioned above are expected to have positioned American Express for year-over-year growth in the third quarter. However, an increase in customer engagement and operating costsis likely to have partially offset the positive impacts.

Third-quarter client engagement costs are likely to have increased due to expanding Card Member spending and higher usage of travel-related benefits. Also, the Zacks Consensus Estimate for pre-tax income from International Card Services (“ICS”) indicates a 22.9% decline from a year ago.

While an earnings beat looks uncertain for AmEx, here are some companies from the broader Finance space that you may want to consider, as our model shows that these have the right combination of elements to post an earnings beat this time around:

Bridgewater Bancshares, Inc. BWB has an Earnings ESP of +4.88% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Bridgewater’s bottom line for the to-be-reported quarter is pegged at 41 cents per share, which indicates a 51.9% jump from a year ago. The consensus estimate for Bridgewater’s revenues is pegged at $37.1 million, a 36.8% year-over-year increase.

Ameriprise Financial, Inc. AMP has an Earnings ESP of +3.38% and a Zacks Rank of 2.

The Zacks Consensus Estimate for Ameriprise Financial’s bottom line for the to-be-reported quarter is pegged at $9.55 per share, which indicates 8.2% year-over-year growth. The consensus estimate for Ameriprise Financial’s revenues is pegged at $4.51 billion, a 3.6% increase from a year ago.

Bread Financial Holdings, Inc. BFH has an Earnings ESP of +0.54% and a Zacks Rank of 3.

The Zacks Consensus Estimate for Bread Financial’s bottom line for the to-be-reported quarter is pegged at $2.24 per share, a 21.7% jump from a year ago. The consensus estimate for Bread Financial’s revenues is pegged at $966.95 million.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite