|

|

|

|

|||||

|

|

|

Anheuser-Busch InBev SA/NV BUD, alias AB InBev, has strengthened its competitive edge by strategically focusing on premiumization and innovation across its global portfolio. Despite facing volume pressures in key markets like Brazil and China, the company’s emphasis on value-driven growth rather than volume-led expansion has delivered strong results. In the second quarter of 2025, EBITDA rose 6.5% year over year and margins expanded, reflecting the effectiveness of its premium offerings and disciplined revenue management. By investing in high-margin brands and leveraging consumer insights, AB InBev continues to shift its mix toward products that command pricing power and brand loyalty.

A cornerstone of this approach is the company’s global portfolio of megabrands, including Corona, Budweiser, Stella Artois and Michelob Ultra, which together anchor its premiumization strategy. AB InBev owns eight of the world’s 10 most valuable beer brands, according to Kantar BrandZ, underscoring its brand leadership. Corona’s revenues grew 7.7% outside of Mexico, while Michelob Ultra and Stella Artois climbed in global rankings. The company’s investment of more than $3.6 billion in marketing in the first half of 2025 illustrates its commitment to strengthening brand equity and enhancing consumer engagement. These sustained investments are helping BUD capture share in the fast-growing premium and super-premium beer categories worldwide.

Innovation has also been a crucial growth lever in maintaining BUD’s relevance with evolving consumer preferences. The company has successfully launched new offerings such as Michelob Ultra Zero — a zero-alcohol, low-calorie beer — and Busch Light Apple — a seasonal variant that became the industry’s top innovation in 2025. These products demonstrate how AB InBev is broadening its appeal among health-conscious and younger consumers seeking novel experiences. Its innovation focus is not limited to flavors but extends to developing “balanced choices” with no- and low-alcohol options, catering to a broader range of consumption occasions.

Digital transformation further supports the company’s innovation-driven competitiveness. Through platforms like the BEES marketplace and its direct-to-consumer digital ecosystem, AB InBev is digitizing its route-to-market and deepening customer relationships. In second-quarter 2025, BEES achieved a 63% year-over-year increase in gross merchandise value, reaching $785 million, while digital DTC platforms generated $134 million in revenues. These tools not only improve operational efficiency but also enable data-driven decision-making and personalized consumer experiences — key advantages in today’s competitive beverage landscape.

Looking ahead, AB InBev’s premiumization and innovation strategies appear well-positioned to sustain its market leadership. By continuously investing in brand equity, expanding its non-alcohol and premium portfolios and leveraging digital capabilities, the company is adapting to long-term consumer shifts and economic dynamics. While short-term volume softness in regions like Brazil and China remains a headwind, AB InBev’s strategic emphasis on value creation, innovation and premium growth is likely to keep it ahead of rivals and reinforce its global dominance in the beer and beverage industry.

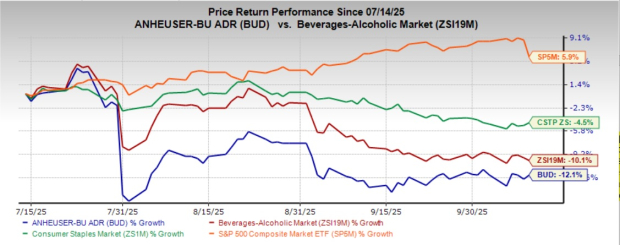

Shares of this Zacks Rank #3 (Hold) company have lost 12.1% in the past three months, underperforming both the industry and the broader Consumer Staples sector, which have declined 12% and 4.5%, respectively. The stock also lagged the S&P 500, which gained 5.9% in the same period.

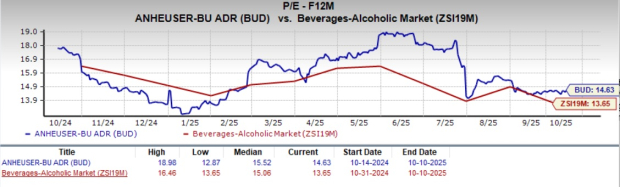

BUD currently trades at a forward 12-month P/E ratio of 14.63X, which is higher than the industry average of 13.65X. This valuation positions the stock at a premium relative to its industry peers, suggesting that investors may be pricing in stronger growth prospects, brand strength or operational efficiency compared with competitors.

United Natural Foods UNFI engages in the distribution of natural, organic, specialty, produce and conventional grocery and non-food products. It currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for United Natural Foods' current financial-year sales and earnings indicates growth of 2.4% and 167.6%, respectively, from the prior-year levels. UNFI delivered a trailing four-quarter earnings surprise of 416.2%, on average.

Zevia PBC ZVIA develops, markets and distributes zero-sugar sodas, energy drinks and organic teas across the United States and Canada under its flagship brand. The company currently flaunts a Zacks Rank #1.

The Zacks Consensus Estimate for Zevia’s 2025 sales and earnings implies growth of 3.8% and 51.6%, respectively, from the previous year’s reported numbers. ZVIA has a trailing four-quarter average earnings surprise of 45.9%.

Vital Farms VITL packages, markets and distributes shell eggs, butter and other products. It carries a Zacks Rank #2 (Buy) at present. VITL delivered a trailing four-quarter earnings surprise of 35.8%, on average.

The Zacks Consensus Estimate for Vital Farms’ current fiscal-year sales and earnings implies an increase of 27.3% and 16.1%, respectively, from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-03 | |

| Aug-01 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite