|

|

|

|

|||||

|

|

|

Dutch Bros Inc. BROS and CAVA Group, Inc. CAVA may serve very different customer cravings — one energizing America through its vibrant drive-thru beverage culture, the other fueling healthy lifestyles with Mediterranean-inspired bowls — but both share a common goal: to build next-generation brands that resonate with millennials and Gen Z while scaling rapidly across the United States.

Each represents the evolution of fast-casual dining, experience-driven, community-focused and digitally connected. Yet their growth paths are unfolding in distinct ways. Dutch Bros is accelerating expansion with impressive shop productivity and deepening loyalty engagement, while CAVA is executing a disciplined, operations-led growth strategy anchored in strong unit economics and menu consistency. For investors, the question is: which upstart has the stronger growth trajectory from here, Dutch Bros or CAVA? Let’s find out.

Dutch Bros has positioned itself as a high-growth, culture-centric brand that blends speed, friendliness, and community with a scalable operating model. Its focus on drive-thru convenience, menu innovation, and digital engagement continues to differentiate it in the competitive beverage space.

The brand’s loyalty program remains a powerful growth engine, driving repeat visits and deepening customer relationships. A growing portion of sales now stems from digital channels, supported by mobile ordering and targeted marketing. The company’s expanding food pilot program also signals a strategic effort to capture incremental revenue during the morning daypart, a move that could meaningfully boost average check sizes and daypart utilization over time.

On the operational front, Dutch Bros’ disciplined expansion strategy stands out. Management has maintained a clear emphasis on site selection, throughput optimization and training, ensuring new units open with strong sales trajectories and high retention rates. The company’s regionalized development strategy, combined with a proven franchising infrastructure, supports long-term scalability while preserving brand culture.

However, near-term headwinds could weigh on profitability. Rising occupancy and preopening costs are pressuring shop-level margins amid accelerated expansion. Additionally, coffee tariffs and commodity volatility pose risks, as coffee accounts for about 10% of the total cost of goods sold. While most coffee prices are secured through 2025, tariff impacts could intensify later in the year.

CAVA is rapidly emerging as a leader in the health-driven fast-casual category, pairing strong brand appeal with disciplined operational execution. Its Mediterranean-inspired menu has resonated with younger consumers seeking flavor, freshness and convenience, a combination that has fueled solid sales momentum and strong unit-level returns. The company’s digital ecosystem continues to enhance frequency and engagement, while efficiency efforts in kitchen design and labor scheduling are improving throughput during peak hours.

Operational discipline remains central to CAVA’s strategy. The company opened 21 new restaurants last quarter and plans around 100 new units in 2025, reinforcing confidence in its long-term potential to surpass 1,000 domestic locations. Recent investments in supply chain infrastructure and process optimization are aimed at supporting scale and maintaining consistency across markets. These efforts, combined with a healthy balance sheet and growing brand equity, position CAVA as one of the most promising concepts in the fast-casual space.

However, the company’s rapid expansion comes with challenges that could pressure near-term profitability. Food inflation, wage growth, and elevated occupancy costs are weighing on margins, while ongoing reinvestments in product quality and brand marketing are increasing expense intensity. Management also noted sales softness in select urban markets, as well as higher training and opening costs tied to its aggressive growth pipeline. Though the company continues to post healthy restaurant-level margins, the pace of new openings and inflationary volatility in core ingredients like grains and proteins could limit incremental flow-through in the short term.

To protect profitability, CAVA is focused on building operational capacity before accelerating expansion further. The company’s disciplined approach to site selection and cost control should help mitigate risks, but near-term margin recovery is likely to be gradual given persistent inflation, rising labor costs, and growing competitive intensity in the healthy fast-casual category. While the long-term growth story remains compelling, execution consistency and cost discipline will be critical in determining whether CAVA can sustain its strong performance as it scales.

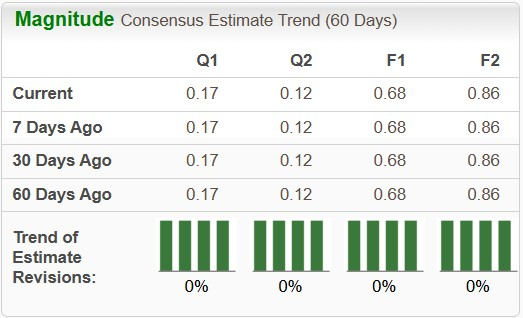

The Zacks Consensus Estimate for Dutch Bros’ 2025 sales and earnings per share (EPS) suggests year-over-year increases of 25% and 38.8%, respectively. In the past 60 days, earnings estimates for 2025 have remained unchanged.

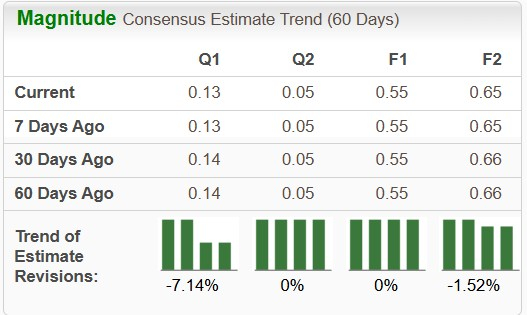

The Zacks Consensus Estimate for CAVA’s 2025 sales and EPS suggests year-over-year increases of 22.7% and 31%, respectively. In the past 60 days, earnings estimates for 2025 have remained unchanged.

Dutch Bros’ stock has declined 13.4% in the past three months compared with the industry’s fall of 8% and the S&P 500’s growth of 7%. Meanwhile, CAVA shares have declined 26.5% over the same time.

Dutch Bros trades at a forward 12-month price-to-sales (P/S) ratio of 4.77, above the industry average of 3.48 over the last year. In contrast, CAVA commands an even higher forward P/S of 5.34.

Overall, both Dutch Bros and CAVA are executing credible growth strategies in the fast-casual space. Yet, Dutch Bros’ accelerating unit expansion, deepening loyalty ecosystem, and strong digital engagement give it a near-term edge in driving traffic and revenue growth. CAVA’s disciplined operations and healthy unit economics remain compelling, but inflationary pressures and rising costs could temper its profitability trajectory. Thus, for investors, Dutch Bros appears better positioned to sustain stronger momentum in the near to medium term.

Dutch Bros currently carries a Zacks Rank #3 (Hold), while CAVA has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 22 min | |

| 32 min | |

| 2 hours | |

| 6 hours | |

| 6 hours |

CAVA Earnings Prediction Market Preview: What Will Brett Schulman Say?

CAVA

Benzinga Prediction Markets

|

| 11 hours | |

| 12 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite