|

|

|

|

|||||

|

|

|

The ongoing uncertainties regarding the newly levied tariffs are concerning, especially for companies like RH RH, which sources products from international markets, including Vietnam, China, Indonesia, India, North America and Europe. Nonetheless, to counter the turbulent market, the company is continuously engaging in executing its in-house initiatives, including product transformation and platform expansion strategies accompanied by its focus on expanding its global market reach. Furthermore, its marketing efforts are acting as a catalyst, shifting market demand in its favor.

After declining on April 2, 2025, the firm’s stock price started moving upward in response to its fourth-quarter fiscal 2024 earnings release. On its earnings call, RH disclosed its upbeat fiscal 2025 views, which are likely to have fostered the uptrend alongside its supply-chain enhancement initiatives. The company’s supply chain management was aimed to reduce the pressures on its margins and cash flows compared to its industry peers.

RH stock has climbed 12.9% during Monday’s trading hours, indicating investors’ optimism about its growth prospects amid a risky macro environment.

The company highlighted the resourcing of the majority of its China production from Vietnam since the last Trump administration, wherein the 25% tariff on China was disclosed. RH currently sources about 35% of its products from Vietnam compared with 23% from China. Furthermore, the company has successfully resourced a significant amount of its China production to its factory in North Carolina.

In regards to Vietnam, RH remains optimistic about the potential negotiations on downsizing tariffs after the recent interaction between Donald Trump and To Lam, General Secretary of the Communist Party of Vietnam. The company believes that if the decision is in favor of Vietnam, it will prove incremental for its growth prospects in the upcoming period.

Backed by favorable in-house capabilities despite the ongoing market uncertainties, the company issued a stellar fiscal 2025 view, which boosted the sentiments of investors.

For the fiscal first quarter, RH expects revenue growth to be between 12.5% and 13.5%, with the adjusted EBITDA margin between 12.5% and 13%, which implies growth from 12.3% reported in the year-ago quarter. For fiscal 2025, the revenue growth is expected to be 10-13%, with adjusted EBITDA margin growth anticipated to be between 20% and 21%, which suggests growth from 16.9% reported in fiscal 2024. The adjusted operating margin expectations of 14-15% also indicate growth from 11.3% reported in fiscal 2024.

Notably, on April 4, 2025, RH announced its expectations for free cash flow of $250-$350 million in fiscal 2025 against the negative cash flow of $213.7 million reported in fiscal 2024.

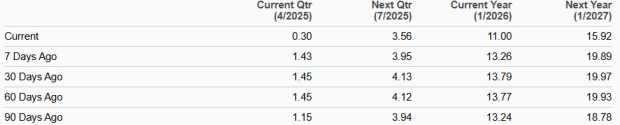

Given the ongoing uncertainties in the housing market due to tariffs on lumber and other building inputs, along with the high mortgage rate scenario and other macro headwinds, analysts’ sentiments are weak for this luxury home furnishing retailer. Earnings estimates for fiscal 2025 have moved down in the past seven days by 17%.

EPS Trend

However, RH’s in-house capabilities are partially offsetting these headwinds, indicating a year-over-year fiscal 2025 estimated growth of 104.1%. This trend outshines the earnings estimate growth rate of RH’s fellow industry players, including Ethan Allen Interiors Inc. ETD, Williams-Sonoma, Inc. WSM and The Lovesac Company LOVE. The earnings estimates for fiscal 2025 indicate a year-over-year decline of 6.8%, 3.1% and 73.1%, respectively, for Ethan Allen, Williams-Sonoma and Lovesac.

RH currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Williams-Sonoma: This San Francisco-based multi-channel specialty retailer of premium quality home products currently carries a Zacks Rank #3 (Hold). Its shares have lost 25.5% in the past three months.

The Zacks Consensus Estimate for fiscal 2025 earnings per share (EPS) has moved up in the past seven days to $8.52 from $8.45. The company’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 19.1%.

Ethan Allen: This Connecticut-based interior design company and manufacturer and retailer of quality home furnishings has lost 4.6% in the past three months. It currently carries a Zacks Rank of 3.

The Zacks Consensus Estimate for fiscal 2025 EPS has remained unchanged over the past 60 days at $2.32. The company’s earnings surpassed the Zacks Consensus Estimate in one of the trailing four quarters, missed on two occasions and met on the remaining occasion, with the average surprise being 0.2%.

Lovesac: This Connecticut-based retailer of home furnishing products carries a Zacks Rank of 3. Its shares have declined 48.8% in the past three months.

The Zacks Consensus Estimate for fiscal 2025 EPS has remained unchanged over the past 60 days at 39 cents. The company’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters and missed on the remaining occasion, with the average surprise being 9.1%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-17 | |

| Jul-10 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite