|

|

|

|

|||||

|

|

|

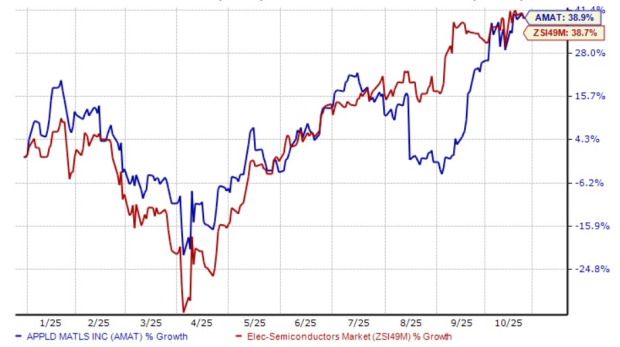

Applied Materials AMAT stock has gained 38.9% in the past three months, outperforming the Zacks Electronics - Semiconductors industry’s return of 38.7%.

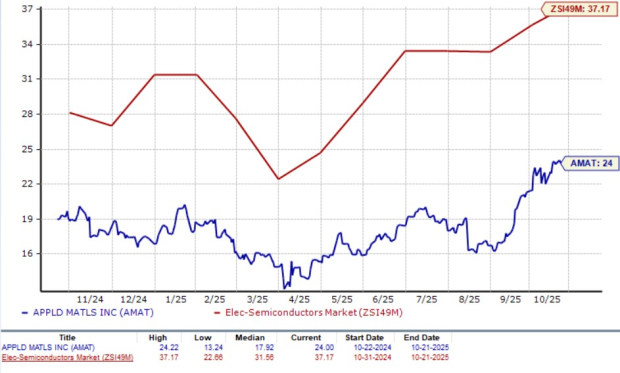

AMAT is currently trading at a lower valuation than its forward 12-month price-to-earnings (P/E) ratio at 24.00X, which is lower than the Zacks Electronics - Semiconductors industry’s average of 37.17X.

This rise in the share price of this semiconductor equipment vendor, while remaining undervalued, raises the question: Should investors hold on or exit the stock? Let’s break down the fundamentals, growth prospects, market challenges and valuation.

Applied Materials is benefiting from rising demand for AI infrastructure as the global data center, cloud and technology space moves toward AI integration. To capitalize on this trend, AMAT has introduced three new semiconductor manufacturing systems designed to power the next generation of AI chips. These systems include Kinex Bonding System, Centura Xtera Epi System and PROVision 10 eBeam Metrology System.

AMAT’s Logic and DRAM businesses are gaining traction on the back of rising demand for AI infrastructure. On the fiscal third-quarter 2025 earnings call, AMAT highlighted its leadership in both Logic and DRAM segments, each driven by major semiconductor transitions.

DRAM revenues grew approximately 50% year over year in the third quarter of fiscal 2025, surpassing $1 billion in etch sales, with next-generation gap fill Chemical Vapor Deposition and dielectric patterning wins positioning Applied Materials for vertical transistor and HBM growth, expected to continue robustly through fiscal 2026.

Applied Materials has been continuously ramping up its R&D investments. For instance, AMAT set up the Equipment and Process Innovation and Commercialization center for research, which is expected to be operational by 2026. The company is also collaborating with organizations like CEA-Leti and increasing its overall R&D expenses.

As discussed in its third-quarter fiscal 2025, the company is reducing its general and administrative expenses to offset the rising cost of R&D, which has effectively enabled AMAT to maintain its operating margin. AMAT’s non-GAAP operating margin expanded 190 basis points in the third quarter of fiscal 2025.

A major headwind for Applied Materials is increasing U.S.-China tensions and export restrictions on semiconductor manufacturing equipment. China remains a crucial market for Applied Materials, accounting for a significant portion of total revenues. However, U.S. government restrictions on selling advanced semiconductor equipment to Chinese manufacturers are hurting Applied Materials’ sales and growth outlook.

AMAT faces elevated uncertainty in China due to ongoing geopolitical tensions and regulatory scrutiny. If stricter export controls are imposed, Applied Materials’ long-term revenue potential could take a hit, as Chinese chipmakers are forced to turn to domestic alternatives or non-U.S. suppliers.

Moreover, the broader semiconductor market is recovering, but memory markets, including DRAM and NAND, remain weak. The company expects only a gradual recovery in memory-related semiconductor demand in 2025, which could weigh on Applied Materials’ revenue growth in the near term. Furthermore, the competition from players like KLA Corporation KLAC, Lam Research LRCX and ASML Holding ASML in the semiconductor supply chain market is also a concern for AMAT.

Lam Research’s memory segment, accounting for both Dynamic Random Access Memory and Non-Volatile Memory divisions, is gaining traction on the back of AI. Lam Research’s memory and Non-Volatile Memory division’s sales are gaining traction. The rising demand for AI chips is also ramping up the demand for advanced process control and process-enabling solutions provided by KLA Corporation.

KLAC’s advanced packaging solutions are also experiencing robust traction on the back of AI and high-performance computing. ASML Holding’s DRAM and logic customers are driving the demand for its products. These customers are ramping up leading-edge nodes using ASML’s NXE:3800E EUV systems. Additionally, ASML noted that multiple DRAM customers are adopting EUV lithography, which helps in shortening cycle time and lowering costs.

These factors have contributed to analysts lowering the estimates of earnings for the fiscal 2025. The Zacks Consensus Estimate for fiscal 2025 earnings has been revised downward by 2 cents in the past 30 days.

Although AMAT shares may appear discounted, weak fundamentals, macroeconomic headwinds, and U.S. tariff policies weigh on its attractiveness. However, tailwinds like DRAM and NAND revenue growth and AMAT’s AI strategy make us recommend investors retain this Zacks Rank #3 (Hold) stock.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 5 hours | |

| 10 hours | |

| 10 hours | |

| 12 hours | |

| 12 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite