|

|

|

|

|||||

|

|

|

The entertainment landscape continues to evolve rapidly, with streaming wars intensifying and traditional media companies redefining their models. Two giants leading this transformation are Disney DIS and Warner Bros. Discovery WBD — each commanding global scale, deep content libraries and multi-format distribution networks.

Disney remains a century-old entertainment powerhouse, spanning film studios, television, theme parks and streaming platforms. Warner Bros. Discovery, formed from the 2022 merger between WarnerMedia and Discovery, combines HBO, Warner Bros. Pictures, DC Studios, Discovery Network and CNN into one of the industry’s most diversified content ecosystems. Both companies are recalibrating their strategies around streaming profitability, sustainable growth and IP monetisation amid soft linear trends and high content costs.

Let’s delve deep and closely compare the two stocks to assess their strategic positioning.

WBD operates across Studios, Streaming, and Linear Networks, supported by one of the industry’s largest content libraries and global production footprints. Its mix of scripted, unscripted and live programming provides reach across platforms as consumer demand continues to shift toward streaming-first viewing.

The Studios division anchors WBD’s creative ecosystem. The Zacks Consensus Estimate for third-quarter 2025 Studio revenue is pegged at $2.77 billion, up 5.6% year over year, reflecting steady contributions from franchises such as Harry Potter, DC Universe and Dune. The company’s streaming platform, Max, complements this foundation and continues to scale across 77 markets. With a slate combining franchise IP and original storytelling, upcoming titles like Supergirl: Woman of Tomorrow, The Batman II, The Lord of the Rings: The Hunt for Gollum, Clayface and new seasons of The White Lotus and The Last of Us reinforce Max’s premium positioning and engagement depth.

The Global Linear Networks segment — which includes CNN, TNT Sports, Discovery Channel and HGTV- remains a stable cash contributor, though ongoing advertising softness limits growth. Its cash flow continues to support content investments and debt servicing, with leverage still near $30 billion.

However, WBD is entering a complex restructuring phase following its announced separation into two focused entities — Warner Bros. (Studios & Streaming) and Discovery Global Media (Linear Networks) — while exploring a potential sale of select studio assets. These moves aim to simplify operations and unlock value, but could pressure margins as restructuring and divestiture costs weigh on results. The Zacks Consensus Estimate for third-quarter 2025 loss is pegged at 5 cents per share, improving by 3 cents over the past month but marking a 200% decline from earnings of 5 cents a year earlier. The consensus mark for 2025 EPS is pegged at 36 cents, up 3 cents in the past 30days and reflecting a turnaround from a loss of $4.62 per share last year — suggesting gradual recovery potential, though sustained profitability will depend on execution discipline and market conditions over the next few quarters.

Warner Bros. Discovery, Inc. price-consensus-chart | Warner Bros. Discovery, Inc. Quote

Disney is progressing through a broad transformation aimed at restoring earnings momentum and strengthening its dual growth engines — streaming and Experiences. The company is pursuing a disciplined approach to cost management, content monetisation and capital efficiency across its Entertainment, Sports and Experiences segments.

The Direct-to-Consumer (DTC) business remains a major growth driver, anchored by Disney+, Hulu and ESPN+. Together, these platforms position Disney as a leader in global streaming, spanning family entertainment, general content and premium sports. The Zacks Consensus Estimate for fourth-quarter 2025 DTC revenue is pegged at $6.3 billion, reflecting 9.01% year-over-year growth, driven by subscriber additions and improved monetisation. The consensus mark for Disney+, Hulu and ESPN+ paid subscribers is pegged at 71.3 million, 60.7 million and 24.5 million, respectively. Broader adoption of ad-supported tiers, rising international engagement, and a steady slate of major releases such as Mufasa: The Lion King, Captain America: Brave New World, Moana 2 and Inside Out 2 are expected to sustain momentum and accelerate the path to streaming profitability.

The Experiences segment, encompassing Parks, Resorts and Cruises, continues to anchor Disney’s earnings. The Zacks Consensus Estimate for fourth-quarter 2025 Experiences revenue is pegged at $8.22 billion, reflecting solid attendance, strong guest spending and healthy bookings. Expansion initiatives, including the upcoming resort and theme park on Yas Island in Abu Dhabi, Disney’s first in the Middle East, highlight its global reach and long-term growth potential.

The Zacks Consensus Estimate for 2025 EPS is pegged at $5.87, unchanged over the past 30 days and representing 18.11% year-over-year growth. Improving DTC margins, consistent performance in Experiences and prudent cost management are expected to support Disney’s earnings recovery and strengthen its long-term investment appeal.

The Walt Disney Company price-consensus-chart | The Walt Disney Company Quote

Both Disney and Warner Bros. Discovery carry a Value Score of B, suggesting attractive valuations relative to their fundamentals. Disney’s forward P/S of 2.04X is higher than WBD’s 1.33X, reflecting market confidence in its diversified business mix and steadier earnings outlook. While both stocks trade below historical averages, Disney’s broad exposure across streaming, content, sports and experiences offers greater earnings stability and long-term visibility. In contrast, WBD’s heavier reliance on advertising-driven linear networks and its ongoing restructuring efforts create higher cyclicality and execution risk.

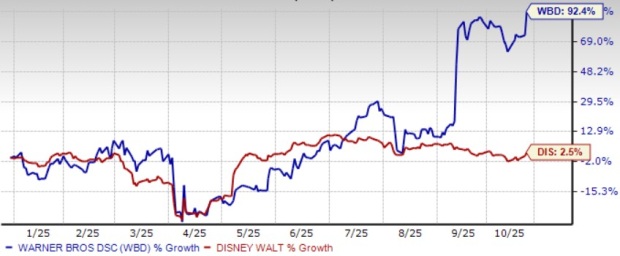

WBD’s shares have soared 92.4% year to date, largely outperforming Disney’s modest 2.5% appreciation during the same period. WBD’s rally has been fueled by investor speculation surrounding restructuring and potential asset divestitures, though much of this optimism now appears priced in amid limited earnings visibility. In contrast, Disney’s steadier performance reflects a more fundamental recovery trajectory, supported by improving streaming economics, resilient park operations and upcoming international expansion.

Both Disney and WBD continue to evolve as the media landscape shifts toward streaming-first business models and diversified monetisation. WBD’s content depth and improving streaming performance highlight operational progress, yet its heavy exposure to advertising and ongoing restructuring introduces higher volatility and earnings uncertainty. Disney, in comparison, offers a steadier trajectory supported by improving DTC margins, resilient Parks and Experiences revenue and global expansion plans. With multiple growth drivers still unfolding and balanced cash flow visibility, DIS appears better positioned to deliver sustainable long-term value. Both DIS and WBD currently carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 34 min | |

| Jul-25 | |

| Jul-24 |

Paramount agrees to delay Warner Bros. merger amid claims of antitrust violations

WBD

The Spokesman-Review, Spokane, Wash.

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite