|

|

|

|

|||||

|

|

|

Dover Corporation DOV has reported third-quarter 2025 adjusted earnings per share (EPS) from continuing operations of $2.62, beating the Zacks Consensus Estimate of $2.50. In the year-ago quarter, the company reported an adjusted EPS of $2.27. On a reported basis, Dover has delivered an EPS (from continuing operations) of $2.20 in the quarter, down 3% year over year.

Total revenues in the third quarter were $2.08 billion, up 4.8% from the year-ago quarter. The top line missed the Zacks Consensus Estimate of $2.09 billion. Organic growth was 0.5% in the quarter.

Dover Corporation price-consensus-eps-surprise-chart | Dover Corporation Quote

The cost of sales rose 2% year over year to $1.24 billion in the reported quarter. Gross profit was up 9.2% year over year to $834 million. The gross margin was 40.1% compared with the year-ago quarter’s 38.5%.

Selling, general and administrative expenses grew 6.3% to $456 million from the prior-year quarter. Adjusted EBITDA rose 12% year over year to $543 million. The adjusted EBITDA margin was 26.1% in the quarter compared with the prior-year quarter’s 24.4%.

The Engineered Products segment’s revenues were down 5.5% year over year to $280 million in the quarter. The reported figure fell short of our estimate of $293 million. The segment’s adjusted EBITDA increased 2.9% year over year to $63 million. The figure beat our estimate of $61 million.

The Clean Energy & Fueling segment’s revenues were $541 million compared with the prior-year quarter’s $501 million. The figure beat our estimate of $538 million. The segment’s adjusted EBITDA was $127 million, up from the prior-year quarter’s $108 million. The figure topped our estimate of $115 million.

The Imaging & Identification segment’s revenues moved up 5.3% year over year to $299 million. The reported figure beat our estimates of $284 million. The segment’s adjusted EBITDA was $86 million, up from the year-ago quarter’s $81 million. The figure beat our estimate of $84 million.

The Pumps & Process Solutions segment’s revenues rose 16.6% year over year to $551 million in the third quarter and surpassed our estimate of $516 million. The adjusted EBITDA of the segment totaled $183 million, up 21.1% from the year-ago quarter’s $151 million. The reported figure beat our projection of $172 million.

The Climate & Sustainability Technologies segment’s revenues fell 5.2% to $409 million from $431 million in the year-earlier quarter. We had predicted revenues of $455 million for this segment. The segment’s adjusted EBITDA totaled $83.6 million compared with $83.1 million in third-quarter 2024. The figure was lower than our estimate of $87 million.

Dover’s bookings at the end of the third quarter were around $2 billion compared with the prior-year quarter’s $1.85 billion. Total booking missed our estimate of $1.97 billion.

The company had a free cash inflow of $370 million in the third quarter compared with the year-ago quarter’s $315 million. Cash flow from operations amounted to $424 million in the quarter under review compared with the prior-year quarter’s $353 million.

Backed by solid end-market demand, the company raised its 2025 outlook. It has raised the adjusted EPS view to $9.50-$9.60 for 2025 from $9.35-$9.55. The company anticipates year-over-year revenue growth of 4-6%.

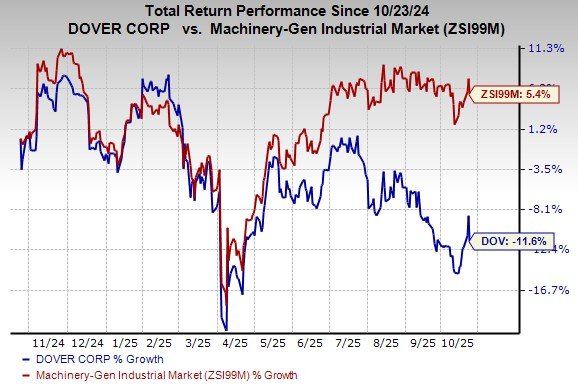

Dover’s shares have lost 11.6% in the past year against the industry’s 5.4% growth.

Dover currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Graco Inc. GGG reported adjusted EPS of 73 cents in third-quarter 2025, which missed the Zacks Consensus Estimate of 75 cents. The bottom rose 3% year over year.

Revenues increased 4.6% year over year to $543 million. The top line missed the Zacks Consensus Estimate of $562 million.

Flowserve Corporation FLS is scheduled to release its third-quarter 2025 results on Oct. 28. The Zacks Consensus Estimate for Flowserve’s third-quarter 2025 earnings is pegged at 80 cents per share, suggesting year-over-year growth of 29%.

The Zacks Consensus Estimate for Flowserve’s top line is pegged at $1.21 billion, indicating an increase of 6.6% from the prior year’s actual. FLS has a trailing four-quarter average surprise of 5.5%.

Crane Company CR, scheduled to release third-quarter 2025 results on Oct. 27, has a trailing four-quarter average surprise of 7.5%. The Zacks Consensus Estimate for Crane’s third-quarter 2025 earnings is pegged at $1.46 per share, suggesting year-over-year growth of 5.8%.

The Zacks Consensus Estimate for Crane’s top line is pegged at $576 million, indicating a decrease of 3.5% from the prior-year reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-05 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite