|

|

|

|

|||||

|

|

|

DRDGOLD Ltd. DRD and Gold Fields Ltd. GFI are two prominent South Africa–based gold mining companies, each playing distinct roles in the global gold industry. DRD operates primarily in the niche segment of surface retreatment, recovering residual gold from old mine dumps and tailings storage facilities around the Johannesburg region. Its operations are mainly through Ergo and Far West Gold Recoveries, which focus on sustainable, low-cost extraction, emphasizing environmental rehabilitation and efficient resource utilization.

Gold Fields, on the other hand, is a globally diversified gold producer with large-scale mining operations and development projects across South Africa, Ghana, Australia, Peru and Chile.

DRDGOLD and Gold Fields represent two contrasting but complementary approaches within the gold sector, one specializing in tailings retreatment and the other in large-scale global production.

Let’s dive deep and closely compare the fundamentals of these two gold stocks to determine which one is a better investment option in the current gold pricing and demand environment.

DRDGOLD’s operations reflect a strategic balance between profitability and sustainability. The company’s core business is the surface retreatment of historical mine dumps and tailings, positioning it uniquely in the gold mining sector as an environmentally restorative operator rather than a traditional underground miner.

DRDGOLD is advancing its flagship FWGR Phase II expansion project, which includes the construction of a new Regional Tailings Storage Facility (RTSF) and the DP2 Plant expansion. This capital program is designed to extend life-of-mine production, lower long-term unit costs and unlock higher throughput capacity.

In the first quarter of 2026, which ended Sept. 30, 2025, DRDGOLD reported a relatively stable operating performance, buoyed by a strong gold price and slightly improved yield. Revenues rose about 2% quarter on quarter to R 2,254.9 million (roughly $124.24 million), driven by gold sales of 37,231 ounces and an average selling price of $3,429 per ounce.

DRDGOLD reported that it remained debt-free as of Sept. 30, 2025. Cash and cash equivalents at the quarter's end were R 1,049.1 million (roughly $57.80 million), down from R 1,306.2 million (approximately $72 million) on June 30, 2025. In the first quarter of fiscal 2026, DRDGOLD incurred capital expenditure of R 751.8 million (roughly $41.42 million). A substantial portion of this growth capex is geared toward the FWGR Phase II infrastructure.

Its growth potential is constrained by its single-region exposure in South Africa and reliance on tailings retreatment yields. Any disruption in processing operations or a dip in recovered grades can significantly affect margins. Additionally, its limited project pipeline makes it more dependent on prevailing gold prices to drive earnings growth.

Gold Fields delivered a strong operational performance in the second quarter of 2025, supported by higher output from its core assets and continued ramp-up progress at the new Salares Norte mine in Chile. Salares Norte remained the standout project with full ramp-up targeted for early 2026. Gold Fields’ ESG and decarbonization efforts gained further traction during the quarter. The group advanced solar and hybrid renewable projects at several sites, particularly in Australia and South Africa, aimed at reducing energy costs and carbon emissions.

In the second-quarter results, the company reported producing approximately 2,518 kg of gold (roughly 81,000 ounces), up around 12% sequentially. This increase was primarily driven by improved throughput and grade recovery at the Australian operations and the steady commissioning of Salares Norte.

At the end of June 2025, GFI’s cash and cash equivalents were around $1.05 billion, slightly lower than December 2024 levels of $1.12 billion. The debt-to-capital percentage was 35.44%. Capital expenditure in the first half of the year was about $665 million, with significant spending on ramp-up and growth and sustaining capital across operations.

It faces cost inflation pressures, particularly in energy and labor, as well as operational risks tied to weather disruptions and new project execution. Currency volatility across its operating regions and regulatory challenges in Africa and South America also pose potential headwinds.

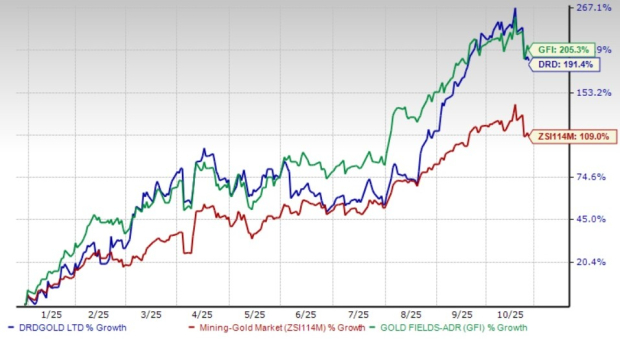

DRD stock is up 191.4% year to date, and GFI is up 205.3% compared with the Zacks Mining-Gold industry’s rise of 109%.

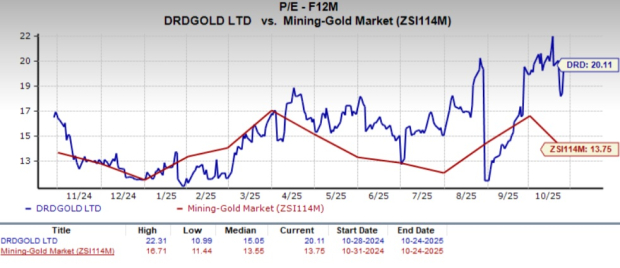

DRD is currently trading at a forward 12-month earnings multiple of 20.11X. This represents a roughly 46.2% premium when stacked up with the industry average of 13.75X.

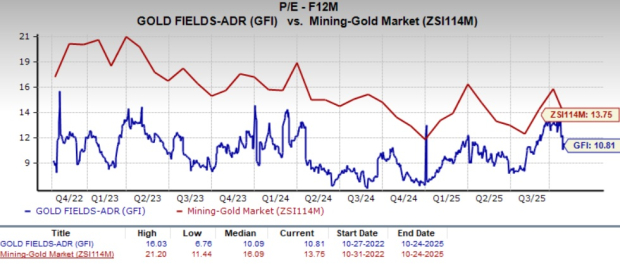

GFI is currently trading at a forward 12-month earnings multiple of 10.81X, below both the industry and DRD.

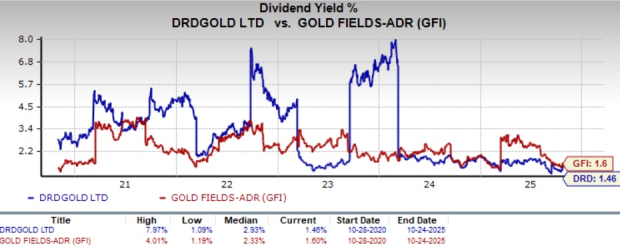

DRD currently offers a dividend yield of about 1.46%. It has increased the dividends seven times in the last five years, striking a balance between shareholder returns and business reinvestment. The 5-year annualized dividend growth is 9.61%.

GFI currently offers a dividend yield of about 1.60%. It has increased its dividends six times in the last five years. The 5-year annualized dividend growth is 17.51%. Gold Fields declared an interim dividend of ZAR 7.00 per share (roughly 39 cents per share), which is a 133% increase from the equivalent period in 2024.

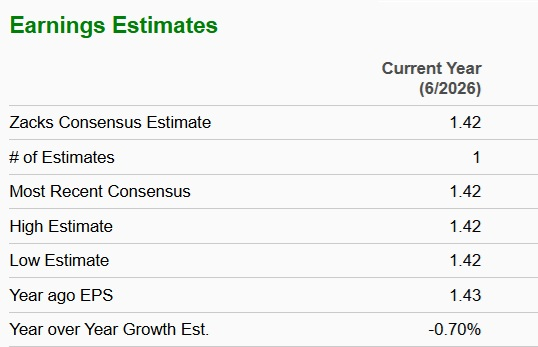

The Zacks Consensus Estimate for DRD’s fiscal 2026 sales implies year-over-year growth of 35.20%. The same for EPS suggests a 0.7% year-over-year rise. EPS estimates for fiscal 2026 have been trending higher over the past 60 days.

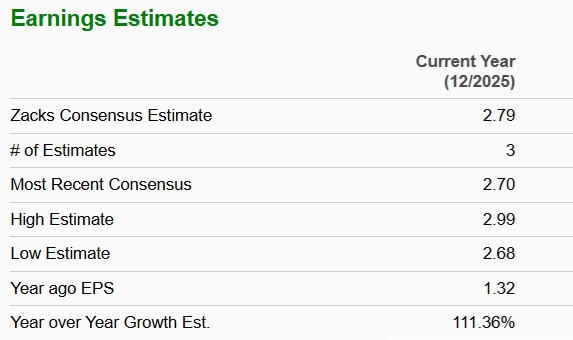

The consensus estimates for GFI’s fiscal sales and EPS imply a year-over-year rise of 69.44% and 111.36%, respectively. EPS estimates for 2025 have been trending northward over the past 60 days.

While DRDGOLD offers steady, low-risk production and a solid, debt-free balance sheet, its growth is limited by single-region exposure. Gold Fields, in contrast, delivers diversified global operations, rising output and robust cash generation, supported by the ramp-up of Salares Norte. The company’s moderate leverage, consistent dividends and operational efficiency provide both growth and stability. Expansion into renewable energy initiatives to support sustainable mining and lowering costs is also commendable. These factors make GFI the better choice for investors seeking stronger upside potential in the gold sector.

DRD currently has a Zacks Rank of #5 (Strong Sell) while GFI has a Zacks Rank of #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-08 | |

| Jun-04 | |

| Jun-01 | |

| May-26 | |

| May-04 | |

| Apr-08 | |

| Mar-10 | |

| Mar-06 | |

| Mar-03 | |

| Mar-03 | |

| Mar-03 | |

| Feb-27 | |

| Feb-27 | |

| Feb-23 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite