|

|

|

|

|||||

|

|

|

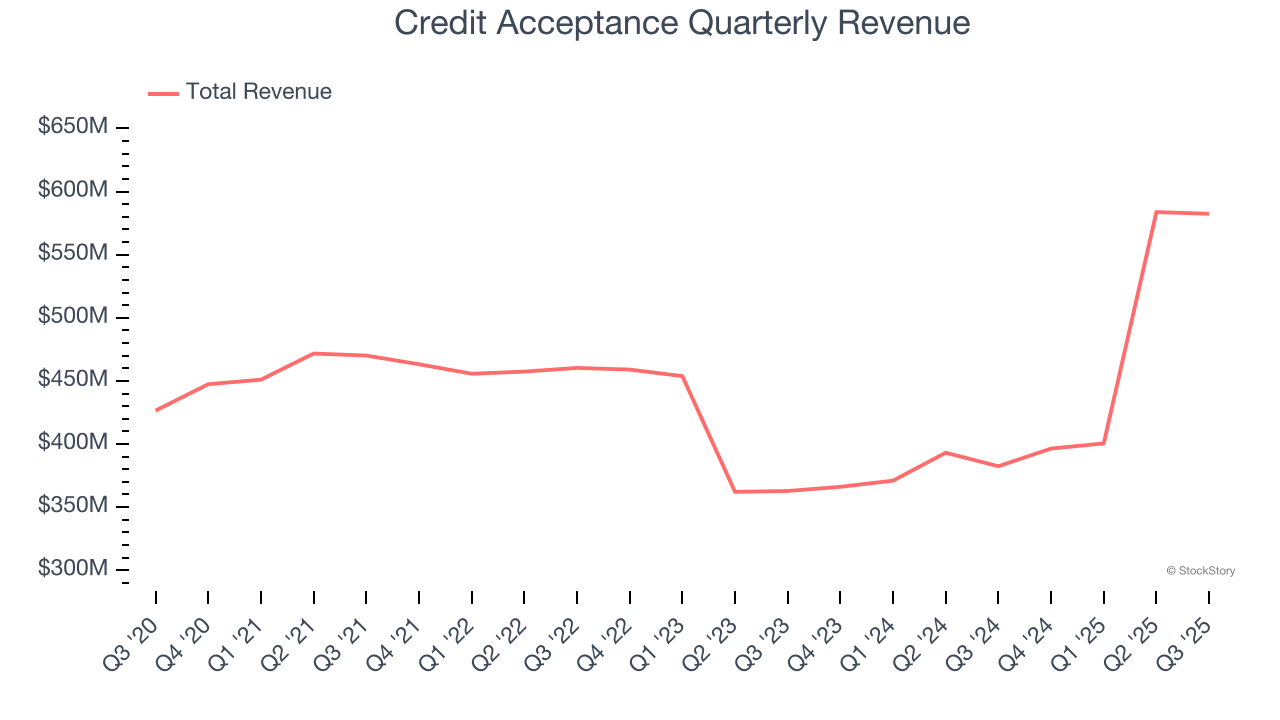

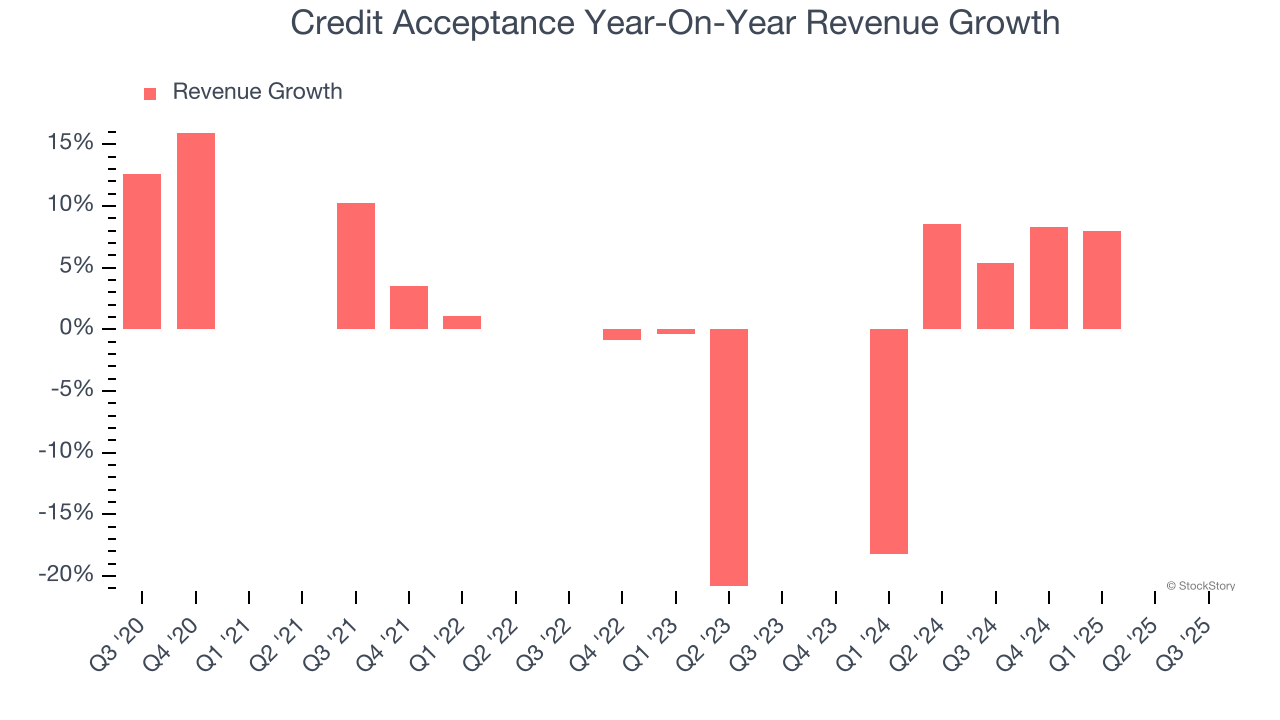

Auto financing company Credit Acceptance (NASDAQ:CACC) announced better-than-expected revenue in Q3 CY2025, with sales up 52.3% year on year to $582.4 million. Its non-GAAP profit of $10.28 per share was 8.8% above analysts’ consensus estimates.

Is now the time to buy Credit Acceptance? Find out by accessing our full research report, it’s free for active Edge members.

Founded in 1972 by Donald Foss to serve customers overlooked by traditional lenders, Credit Acceptance (NASDAQ:CACC) provides auto financing solutions that enable car dealers to sell vehicles to consumers with limited or impaired credit histories.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Credit Acceptance’s 4.1% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the financials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Credit Acceptance’s annualized revenue growth of 9.5% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Credit Acceptance reported magnificent year-on-year revenue growth of 52.3%, and its $582.4 million of revenue beat Wall Street’s estimates by 15.6%.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

We were impressed by how significantly Credit Acceptance blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $452.38 immediately after reporting.

Is Credit Acceptance an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-28 | |

| Jul-27 | |

| Jun-10 | |

| Jun-09 | |

| Jun-05 | |

| May-06 | |

| May-05 | |

| May-05 | |

| May-05 | |

| Apr-28 | |

| Apr-27 | |

| Apr-09 | |

| Apr-02 | |

| Mar-19 | |

| Mar-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite