|

|

|

|

|||||

|

|

|

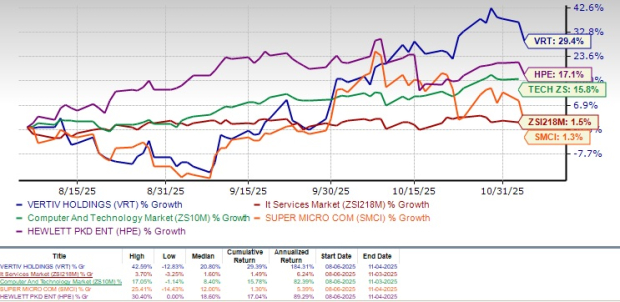

Vertiv VRT shares have gained 29.4% in the past three months, outperforming the broader Zacks Computer and Technology sector’s increase of 15.8% and the Zacks Computers - IT Services industry’s rise of 1.5%.

Vertiv’s shares have also outperformed its peers, which include Super Micro Computer SMCI and Hewlett-Packard Enterprise HPE, both of which are expanding their capabilities to serve hyperscale and enterprise AI data center deployments. Hewlett-Packard and Super Micro Computer shares have gained 17.1% and 1.3%, respectively, in the past three months.

The outperformance can be attributed to VRT’s extensive product portfolio, which spans thermal systems, liquid cooling, UPS, switchgear, busbars, and modular solutions. Acquisitions have also played an important role in expanding Vertiv’s portfolio.

In the trailing 12 months, organic orders grew approximately 21%, with a book-to-bill of 1.4 times for the third quarter of 2025, indicating a strong prospect. Backlog grew 12% sequentially and 30% year over year to $9.5 billion. This growth is primarily driven by the rapid adoption of AI and the increasing need for data centers to support the digital transformation.

Vertiv is expanding its product portfolio through acquisitions, which is noteworthy. It is a leading provider of thermal and power management solutions for data centers that consume immense amounts of power. The company’s energy-efficient power and cooling solutions have been a major growth driver of its success.

Building on this momentum, Vertiv recently announced that it will acquire Purge Rite Intermediate from Milton Street Capital for about $1.0 billion in cash, with up to $250 million in potential earn-outs.

This deal improves Vertiv’s thermal management and liquid cooling services for AI and high-performance data centers. It also strengthens the company’s position as a leader in next-generation thermal chain solutions.

Further expanding its footprint, in August, Vertiv announced its acquisition of Waylay NV to enhance AI-driven monitoring, predictive maintenance and optimization capabilities for its power and cooling systems.

Vertiv’s partnership with NVIDIA NVDA is a plus. In October, Vertiv introduced its gigawatt-scale reference architectures for the NVIDIA Omniverse DSX Blueprint.

These architectures aim to speed up generative AI deployment by up to 50% through its OneCore platform, improved power and cooling systems and flexible options for large-scale AI factory setups.

Vertiv also announced progress in its collaboration with NVIDIA, advancing 800 VDC power architectures to engineering readiness for next-generation AI factories.

Vertiv is benefiting from its strong portfolio and rich partner base, which will continue to benefit the company’s top-line growth.

For fourth-quarter 2025, revenues are expected to be between $2.81 billion and $2.89 billion.

Organic net sales are expected to increase in the 18% to 22% range.

VRT expects fourth-quarter 2025 non-GAAP earnings per share between $1.23 and $1.00.

For 2025, revenues are now expected to be between $10.16 billion and $10.24 billion. Organic net sales growth is expected to be between 26% and 28%.

The Zacks Consensus Estimate for fourth-quarter 2025 earnings is currently pegged at $1.28 per share, which has increased 3.22% over the past 30 days. The figure indicates a year-over-year increase of 29.29%.

The Zacks Consensus Estimate for Vertiv’s fourth-quarter 2025 revenues is pegged at $2.86 billion, suggesting growth of 22.09% year over year.

The Zacks Consensus Estimate for Vertiv’s 2025 revenues is pegged at $10.21 billion, suggesting growth of 27.47% year over year.

The Zacks Consensus Estimate for 2025 earnings is currently pegged at $4.11 per share, which has increased 7.31% over the past 30 days. This indicates a 44.21% increase from the 2024 reported figure.

Vertiv Holdings Co. price-consensus-chart | Vertiv Holdings Co. Quote

Vertiv is currently overvalued, as suggested by a Value Score of F.

In terms of the trailing 12-month Price/Book, Vertiv is currently trading at 19.70X, compared with the broader Computer and Technology sector’s 11.89X, Super Micro Computer’s and Hewlett Packard’s 4.47X and 1.27X, respectively.

Vertiv is benefiting from its strong portfolio and rich partner base, which are driving order growth. These factors justify the company’s premium valuation.

Vertiv stock currently sports a Zacks Rank #1 (Strong Buy) and has a Growth Score of A, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 30 min | |

| 30 min | |

| 32 min | |

| 43 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite