|

|

|

|

|||||

|

|

|

Costco Wholesale Corporation’s COST October sales results demonstrate how its value-driven business model continues to connect with consumers in a cautious environment. Net sales for the four weeks ending Nov. 2, 2025 increased 8.6% year over year to $21.75 billion, supported by a 6.6% rise in comparable sales. This follows comparable sales growth of 5.7% in September and 6.3% in August, indicating strong member loyalty and positive value perception.

The impressive sales performance can be credited to product quality and everyday low prices, which lead to high member retention. The renewal rate in the United States and Canada was 92.3%, with the global rate at 89.8% in the fourth quarter of fiscal 2025. The total number of paid members increased 6.3% to 81 million, highlighting the robustness of its membership model.

A key element of this value proposition is the Kirkland Signature (“KS”) private label brand. KS products generally offer members a 15% to 20% price advantage over national brands of similar or superior quality. The ongoing growth of KS penetration helps counter inflationary pressures. Costco is also actively working to source closer to end markets and increase domestically sourced products to keep prices competitive.

Moreover, Costco’s digital platform exhibited the same value-focused trend, with online sales rising 16.6% during the month. Members are responding positively to this combination of convenience and affordable pricing.

These elements collectively explain why Costco’s consistent sales results reaffirm that its value edge remains effective.

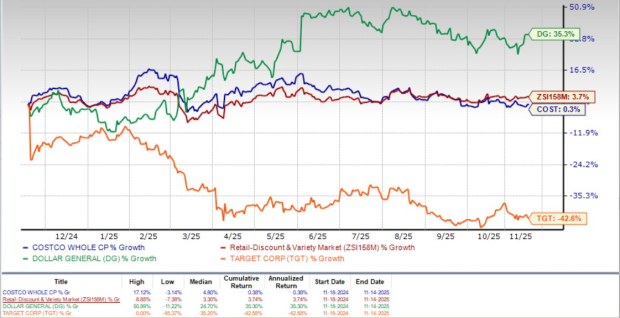

Costco, which competes with Dollar General Corporation DG and Target Corporation TGT, has seen its share rise 0.3% in the past year against the industry’s growth of 3.7%. While shares of Dollar General have rallied 35.3%, Target shares have dropped 42.6% during the period mentioned above.

From a valuation standpoint, Costco's forward 12-month price-to-earnings ratio stands at 45.36, higher than the industry’s ratio of 29.89. COST carries a Value Score of D. Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 11.39) and Dollar General (15.94).

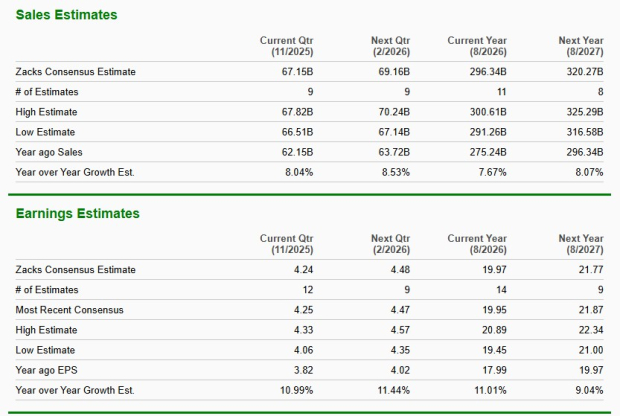

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 7.7% and 11%, respectively.

Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 |

Costco Gas Pumps Are So Popular the Retailer Is Building Stand-Alone Stations

COST

The Wall Street Journal

|

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite