|

|

|

|

|||||

|

|

|

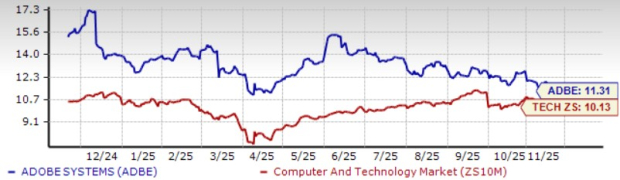

Adobe’s ADBE shares have declined 36.3% in the trailing 12 months, underperforming the Zacks Computer and Technology sector’s return of 23.9% and the Zacks Computer – Software industry’s appreciation of 9.5%. This underperformance reflects modest growth prospects due to stiff competition in the AI and generative AI space from the likes of Microsoft MSFT-backed OpenAI, Alphabet GOOGL, Salesforce CRM, Midjourney, Canva and others.

Adobe shares have underperformed Microsoft, Alphabet and Salesforce in the past year. While shares of Microsoft and Alphabet have returned 17.3% and 68.3%, respectively, Salesforce has declined 30%.

However, Adobe’s strategy of infusing AI into its portfolio is driving growth, as reflected by the third quarter of fiscal 2025 results. Adobe AI influenced annual recurring revenues (ARR), which surpassed $5 billion, and management expects it to continue to rise as a percentage of Adobe’s business. ARR from new AI-first products, including Firefly, Acrobat AI Assistant and GenStudio for performance marketing, hit Adobe’s end-of-year target of more than $250 million. Will this help Adobe recover? Let’s find out.

Adobe is benefiting from strong demand for AI-powered Creative Cloud Pro and Acrobat, as well as AI-first products, Firefly and Acrobat AI Assistant. The monthly active users of Acrobat and Express grew approximately 25% year over year within the Business Professionals and Consumers segment. Adobe has been successfully monetizing Acrobat offerings, including the AI assistant and the Acrobat Studio.

The Creative Professionals business is benefiting from increasing demand and usage of AI in Photoshop, Premiere Pro and Illustrator as part of the new Creative Cloud Pro offering. The addition of Firefly and third-party models in Creative Cloud Applications is driving generative AI (Gen AI) usage. The Marketing professionals’ business benefits from the strong demand for Adobe Experience Platform (AEP) and native applications. The addition of Google Gemini Flash 2.5, Veo and Imagen models, along with models from OpenAI, Black Forest Labs, Runway, Pika, Ideogram and others into Adobe applications is driving clientele.

Workfront, Frame, AEM Assets, Firefly Services and GenStudio for performance marketing products, which comprises the integrated GenStudio solution, now exceed $1 billion in ARR and are growing more than 25% year over year. One Adobe deal saw 60% year-over-year growth, reflecting an improving footprint among enterprises.

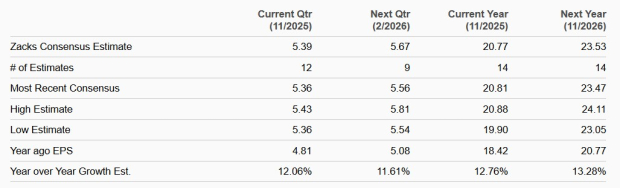

Adobe now expects fiscal 2025 revenues between $23.65 billion and $23.7 billion ($21.51 billion in fiscal 2024), up from the previous guidance range of $23.5-$23.6 billion. Fiscal 2025 non-GAAP earnings are now expected between $20.80 per share and $20.85 per share ($18.42 per share in fiscal 2024), higher than the previous guidance of $20.50-$20.70 per share.

For fiscal 2025, the Zacks Consensus Estimate for revenues is currently pegged at $23.67 billion, suggesting 10.1% growth from 2024’s reported figure. The Zacks Consensus Estimate for earnings is pegged at $20.77 per share, unchanged over the past 30 days. The figure indicates 12.8% growth from fiscal 2024’s reported figure.

Adobe’s AI business is minuscule compared with the likes of Microsoft, Alphabet and Salesforce. Microsoft’s Intelligent Cloud revenues are benefiting from growth in Azure AI services and a rise in the AI Copilot business. Alphabet’s focus on infusing AI heavily across its offerings, including Search and Google Cloud, has been a major growth driver. Salesforce’s strategy of continuous expansion of Gen AI offerings is helping it tap growth opportunities.

Meanwhile, Adobe has a Value Score of C, which suggests a stretched valuation. In terms of price/book, Adobe is trading at 11.31X higher than the broader sector’s 10.13X, Microsoft’s 9.97X, Alphabet’s 9.13X and Salesforce’s 3.54X.

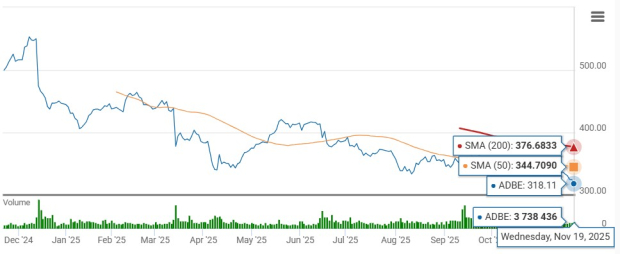

Adobe shares are now trading below the 50-day and 200-day moving averages, indicating a bearish trend.

Adobe’s focus on improving monetization of its AI-powered solutions is a positive for investors already holding the stock. However, a stretched valuation, macroeconomic challenges, and stiff competition make the stock a risky bet right now.

ADBE currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite