|

|

|

|

|||||

|

|

|

Colgate-Palmolive Company CL is at a pivotal moment as global category growth slows and consumer uncertainty persists. While the company continues to demonstrate resilient pricing power, volume recovery remains a challenge across several key markets, particularly in developed economies where demand softness and trade-down behaviors are more pronounced. Against this backdrop, Colgate is leaning heavily on its enhanced innovation model, one it describes as faster, more science-driven and more deeply integrated with AI and digital capabilities.

A major driver of optimism lies in the global relaunch of Colgate Total, which management repeatedly highlighted as a strong catalyst for premiumization and share gains. The new regimen, spanning toothpaste, toothbrush and mouthwash, has been rolled out across numerous markets and is helping Colgate strengthen its competitive position in Oral Care.

Even in regions where temporary challenges emerged, such as Latin America due to flavor-related consumer irritation in select variants, the company notes that market shares are recovering as reformulated products re-enter shelves. In Asia, the innovation has been particularly effective, supporting the case that premium, science-based launches can stimulate category growth and household penetration when executed well.

Beyond Oral Care, Colgate’s innovation agenda is expanding aggressively across its portfolio. The company is deploying new AI-enabled tools to accelerate product development, improve concept validation and enhance demand-generation effectiveness. This includes applying advanced data analytics to sharpen price-pack architecture, refine media content and tailor marketing by channel.

In Pet Nutrition, Hill’s continues to outperform its categories thanks to a rich pipeline of therapeutic and science-driven products that are gaining share across wet, dry, treats and prescription diets. These innovation-led gains demonstrate the company’s ability to use differentiated value and not deep discounting to drive consumer choice even in periods of macro weakness.

Still, the path to restoring broad-based volume momentum is not without obstacles. Consumer pressures in North America, GST transitions and urban softness in India, competitive intensity in China’s premium e-commerce space and lingering category sluggishness across developed markets remain real hurdles.

Innovation can help offset these headwinds but only if paired with calibrated pricing, targeted channel strategies and effective execution at scale. Colgate’s leadership believes the company is at a strategic inflection point, with new capabilities, stronger digital infrastructure and a more agile operating model enabling faster cycles of innovation and commercialization.

Colgate’s shares have lost 13.7% year to date compared with the industry’s 13.2% dip.

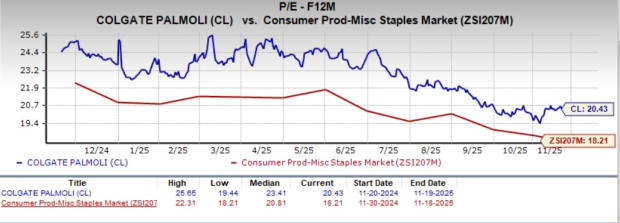

From a valuation standpoint, CL trades at a forward price-to-earnings ratio of 20.43X compared with the industry’s average of 18.21X.

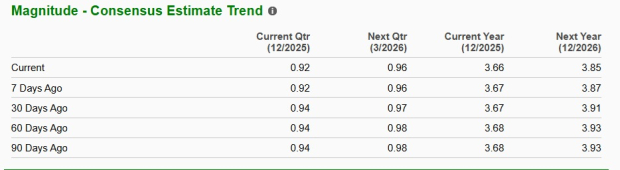

The Zacks Consensus Estimate for CL’s 2025 and 2026 EPS indicates year-over-year growth of 1.7% and 5.2%, respectively. The company’s EPS estimates for 2025 and 2026 have moved south in the past seven days.

Colgate currently carries a Zacks Rank #4 (Sell).

The Chefs' Warehouse, Inc. CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East and Canada. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for The Chefs' Warehouse’s current financial-year sales and earnings indicates growth of 8.1% and 29.3%, respectively, from the prior-year levels. CHEF delivered a trailing four-quarter earnings surprise of 14.7%, on average.

Lamb Weston Holdings, Inc. LW engages in the production, distribution and marketing of frozen potato products in the United States, Canada, Mexico and internationally. It sports a Zacks Rank #1 at present. Lamb Weston delivered a trailing four-quarter earnings surprise of 16%, on average.

The Zacks Consensus Estimate for Lamb Weston's current fiscal-year sales indicates growth of 1.3% from the prior-year levels.

Ollie's Bargain Outlet Holdings, Inc. OLLI, a leading off-price retailer of brand-name household products, currently carries a Zacks Rank #2 (Buy). OLLI has a trailing four-quarter earnings surprise of 4.2%, on average.

The Zacks Consensus Estimate for Ollie's Bargain’s current financial-year sales and EPS suggests growth of 16.4% and 15.3%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 6 hours | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-03 | |

| Aug-01 | |

| Aug-01 | |

| Aug-01 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite