|

|

|

|

|||||

|

|

|

Since May 2025, Sportsman's Warehouse has been in a holding pattern, posting a small loss of 4.5% while floating around $1.90. The stock also fell short of the S&P 500’s 10.4% gain during that period.

Is now the time to buy Sportsman's Warehouse, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We're cautious about Sportsman's Warehouse. Here are three reasons there are better opportunities than SPWH and a stock we'd rather own.

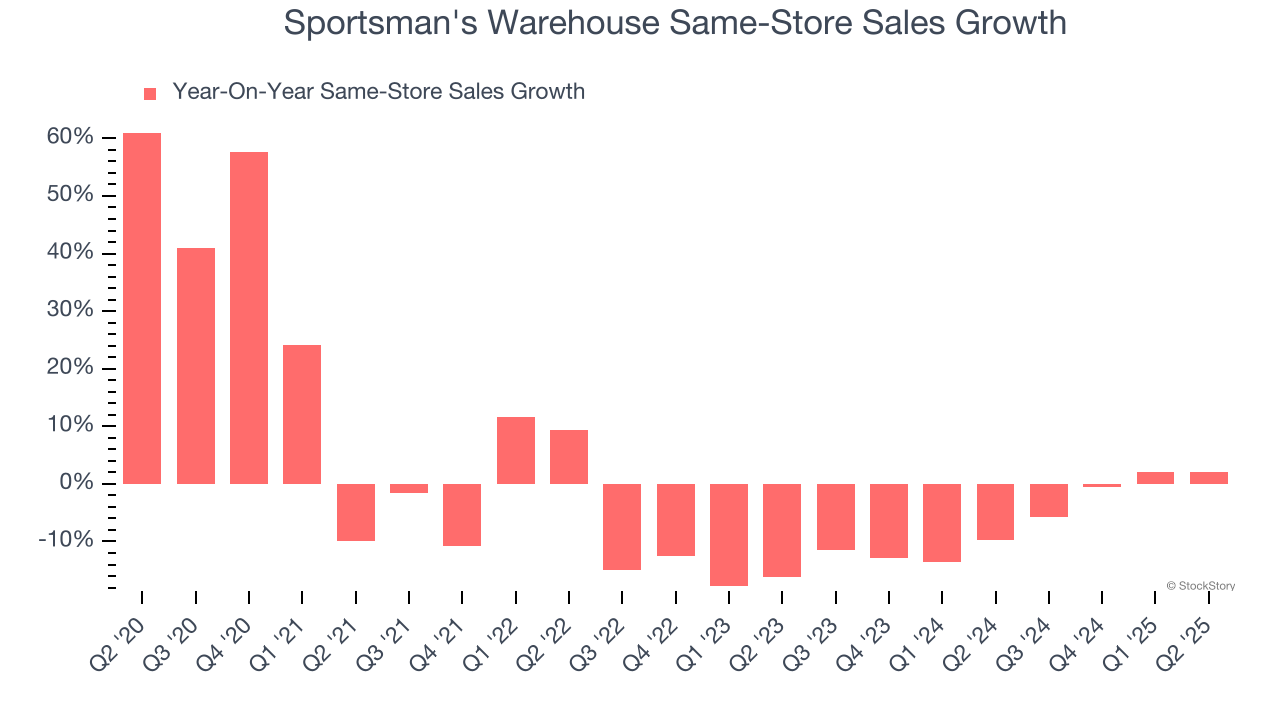

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Sportsman's Warehouse’s demand has been shrinking over the last two years as its same-store sales have averaged 6.2% annual declines.

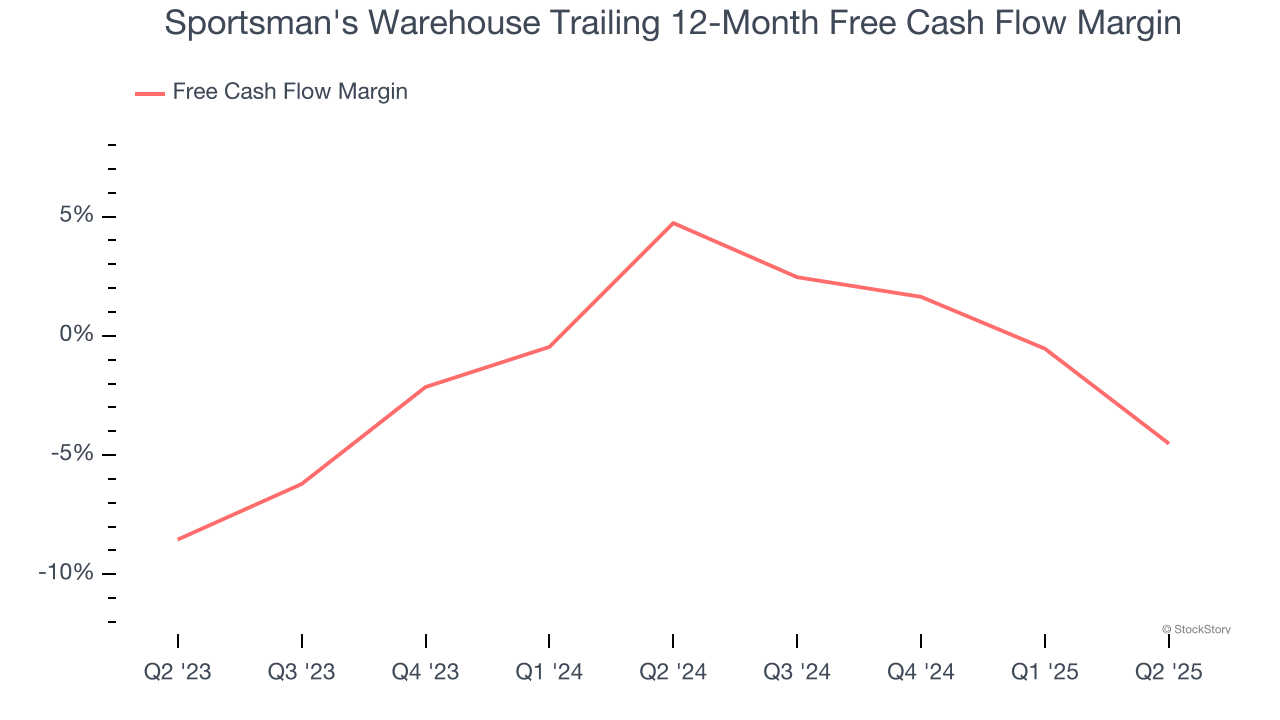

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Sportsman's Warehouse’s margin dropped by 9.2 percentage points over the last year. This decrease warrants extra caution because Sportsman's Warehouse failed to grow its same-store sales. Its cash profitability could decay further if it tries to reignite growth by opening new stores.

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

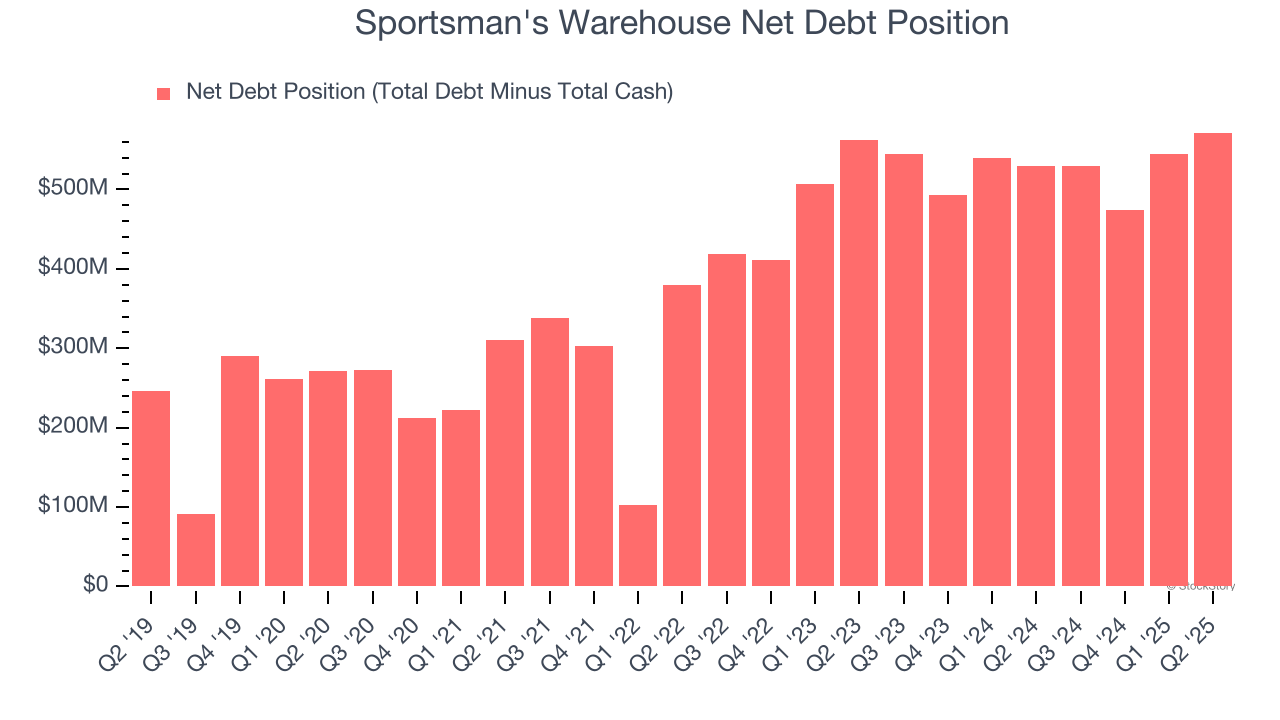

Sportsman's Warehouse burned through $54.57 million of cash over the last year, and its $573.4 million of debt exceeds the $1.80 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Sportsman's Warehouse’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Sportsman's Warehouse until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

We see the value of companies helping consumers, but in the case of Sportsman's Warehouse, we’re out. With its shares underperforming the market lately, the stock trades at 1.8× forward EV-to-EBITDA (or $1.90 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Jun-03 | |

| Jun-02 | |

| Jun-02 | |

| Jun-02 | |

| May-19 | |

| May-15 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-17 | |

| Mar-10 | |

| Mar-06 | |

| Mar-03 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite