|

|

|

|

|||||

|

|

|

Nutrien Ltd. NTR is gaining from healthy demand for crop nutrients, its actions to reduce costs and strategic acquisitions. Higher fertilizer prices are providing further support. However, exposure to volatile input costs and supply tightness could pressure margins.

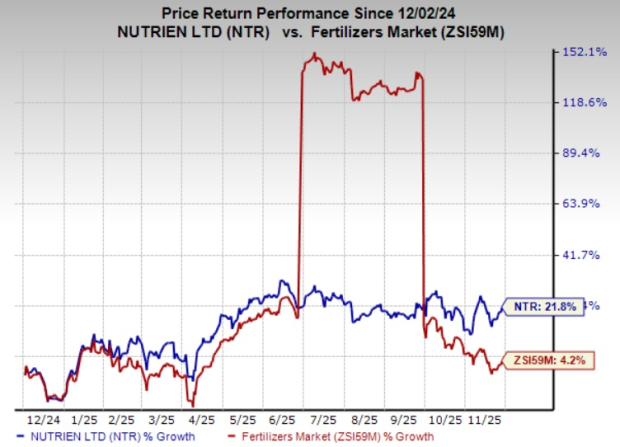

The NTR stock has gained 21.8% over the past year, compared with the Zacks Fertilizers industry’s 4.2% rise.

Let’s find out why NTR stock is worth retaining at the moment.

Nutrien is well-placed to benefit from higher demand for fertilizers, backed by the strength in global agriculture markets. It is seeing healthy fertilizer demand in its major markets. Tight inventories are expected to support crop commodity prices in 2025. Strong demand and supply tightness have also led to an uptick in fertilizer prices this year.

Favorable farmer economics, improved affordability and low inventory levels are expected to drive potash demand globally. The phosphate market is also supported by low producer and channel inventories. Restricted exports from China have also led to supply tightness in this market. Demand for nitrogen fertilizer also remains healthy in major markets. Global nitrogen requirement is driven by demand in North America, India and Brazil. A resurgence in industrial nitrogen demand also bodes well.

The company expects record crop production prospects in the United States and sees strong demand for crop inputs. NTR saw record potash sales volumes in the first nine months of 2025, driven by favorable potash affordability and robust consumption in North America and major offshore markets. Third-quarter volumes also rose due to strong demand in North America and offshore. NTR has raised potash sales volume guidance for 2025 to 14-14.5 million tons, driven by anticipated higher global demand.

NTR should also gain from acquisitions and increased adoption of its digital platform. It continues to expand its footprint in Brazil through acquisitions. It is expected to continue pursuing targeted opportunities in its core markets. The company expects to utilize part of its free cash flow for incremental growth investments, including tuck-in acquisitions in the retail business in 2025.

Cost and operational efficiency initiatives are also expected to aid the company’s performance. NTR remains focused on lowering the cost of production in the potash business. It has announced several strategic actions to reduce its controllable costs and boost free cash flow. NTR has accelerated operational efficiency and cost savings initiatives, and anticipates achieving around $200 million of total savings in 2025. The company is ahead of schedule on this cost-reduction goal.

Nutrien uses sulfur and natural gas as key inputs. Supply disruptions from Russia amid the war with Ukraine contributed to the rise in natural gas prices. Plant shutdowns and maintenance also resulted in a tight supply of these inputs, which, coupled with strong demand, pushed up their prices. The company saw higher sulfur input costs and natural gas prices in the third quarter, leading to a higher cost of goods sold per ton in phosphate and nitrogen businesses, respectively. The company remains exposed to a volatile input cost environment amid supply tightness.

NTR currently carries a Zacks Rank #3 (Hold).

Better-ranked stocks in the Basic Materials space are Kinross Gold Corporation KGC, Fortuna Mining Corp. FSM and Harmony Gold Mining Company Limited HMY. At present, KGC sports a Zacks Rank #1 (Strong Buy), while FSM and HMY carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Kinross Gold’s current-year earnings is pegged at $1.65 per share, indicating a year-over-year rise of 142.7%. KGC’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters, with an average surprise of 17.4%.

The Zacks Consensus Estimate for FSM’s current fiscal-year earnings stands at 83 cents per share, reflecting an 80.4% year-over-year increase. FSM’s shares have surged 123% in the past year.

The Zacks Consensus Estimate for HMY’s fiscal 2026 earnings is pegged at $2.68 per share, indicating a rise of 111% from the year-ago levels. HMY’s shares have rallied roughly 120% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-01 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite