|

|

|

|

|||||

|

|

|

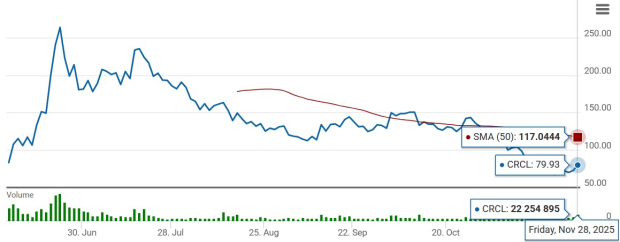

Circle Internet Group CRCL shares have tumbled 33.5% over the past three months, underperforming both the Zacks Financial-Miscellaneous Services industry and the Zacks Finance sector. While the industry has declined 9.5%, the broader sector has managed a 2.3% gain.

CRCL shares have also trailed key peers, including IREN Limited IREN, Cleanspark CLSK and PayPal PYPL. Over the same period, IREN and Cleanspark have rallied 64.2% and 56.6%, respectively, while PayPal has declined 9.5%.

The decline in Circle’s share price can be attributed to rising competitive pressures in the stablecoin market, margin headwinds from higher distribution and operating costs, regulatory uncertainty around the GENIUS Act and concerns over execution risks tied to Arc network development and heavy investment spending.

CRCL is also trading below the 50-day moving average, indicating a bearish trend, suggesting limited upside in the near-term momentum for the stock.

Surging operating costs are becoming a concern as CRCL now expects adjusted operating expenses to rise to $495-$510 million, up from previous guidance of $475-$490 million, reflecting increased investments and higher payroll taxes linked to stock-based compensation. In the third quarter, adjusted operating expenses grew 35% year over year due to headcount expansion and higher general and administrative costs. Additionally, the company’s global expansion efforts are further raising the overall cost structure.

Although the near-term picture looks challenging, Circle still holds potential. Let us dig deep to find out.

Despite the above-mentioned concerns, the growth and adoption of USD Coin (USDC) remain Circle’s primary value driver. In the third quarter of 2025, USDC in circulation surged 108% year over year, supported by accelerating institutional demand and deeper blockchain integration. Engagement on the company’s platform strengthened as on-platform USDC expanded nearly 14 times to $10.2 billion, reflecting rising participation from major financial institutions building directly on Circle’s infrastructure.

USDC’s utility also broadened significantly. On-chain transaction volume skyrocketed 580% year over year, supported by increased usage across payments, trading and cross-chain transfers. Circle’s Cross-Chain Transfer Protocol reinforced USDC’s role as a key liquidity asset, with volume jumping 640% and representing nearly half of major bridge activity in the quarter.

These trends led to strong market share gains. USDC’s share of USD-backed stablecoins climbed to 29%, up 643 basis points, while Visa data indicates USDC captured 40% of all stablecoin transaction volume.

Circle Payments Network (“CPN”) continues to gain a strong grip, supported by rapid global expansion and rising institutional adoption. The network now includes 29 enrolled financial institutions, with 55 more undergoing eligibility reviews and a pipeline of 500 institutions evaluating integration. CPN has also expanded live payment corridors across major markets, including Brazil, Canada, China, Hong Kong, India, Mexico, Nigeria and the United States.

Momentum is also strengthened by accelerating payment activity, with trailing 30-day annualized transaction volume reaching $3.4 billion, representing more than 100x growth in five months. Circle has also broadened CPN’s product suite with CPN Console for self-service onboarding and CPN Payouts for automated stablecoin payouts, improving scalability and operational efficiency.

The Zacks Consensus Estimate for CRCL’s fourth-quarter 2025 earnings is currently pegged at 18 cents per share, revised upward by 3 cents over the past 30 days.

The consensus mark for the full-year 2025 loss is pegged at 87 cents per share, reflecting a substantial year-over-year improvement of $1.07.

In terms of the forward 12-month price/sales (P/S), CRCL is trading at 5.93X, lower than its median of 8.88X and the Zacks Finance sector’s 8.9X. This is reflected in its Value Score of D. The company’s strong USDC growth and expanding network position suggest a meaningful upside for investors.

Despite recent share-price weakness and rising operating costs, CRCL’s long-term fundamentals remain encouraging, supported by accelerating USDC adoption, strong CPN network momentum and improving earnings estimates. Its lower valuation also suggests potential upside. Given these factors, holding the stock appears to be the sensible approach.

Circle currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a better entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite