|

|

|

|

|||||

|

|

|

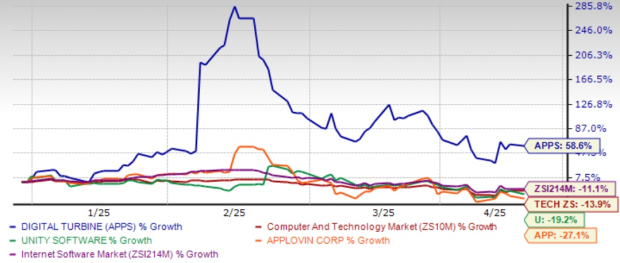

After witnessing a decent surge in the stock price and reaching a 52-week high of $6.86 on Feb. 13 following the annual outlook raise, shares of Digital Turbine APPS have experienced a decline amid broader market woes and tariff issues and are now trading much lower, closing at $2.68 on Monday on the Nasdaq.

However, despite the decline, APPS shares have been up 58.6% so far in the year and have outperformed the Zacks Computer & Technology sector and the Zacks Internet – Software industry.

APPS shares have also delivered stronger performance compared to its industry peers, such as Unity Software U and AppLovin APP. Unity Software and AppLovin are also actively expanding in the digital media and advertising space. So far in the year, shares of Unity and AppLovin have declined 19.2% and 27.1%, respectively. Digital Turbine’s strong performance is driven by solid international revenue growth, high advertiser demand and a broad network of partners.

Year-to-Date Price Performance

However, before making any hasty decision to add following this decline or shrugging off this stock from your portfolio, it would be prudent to understand the factors in detail to better analyze how to play the stock after the price decline.

Digital Turbine’s On-Device Solutions business has been a major growth driver. International On-Device revenues soared 100% year over year in the third quarter of fiscal 2025, fueled by strong advertiser demand and enhanced performance across its sales, product, technology and operations teams. Record-high revenue per device in both U.S. and international markets illustrates the efficiency of the APPS platform and its growing appeal among advertisers, a strong indicator of pricing power and monetization efficiency.

Digital Turbine has made significant strides in broadening its reach by forging strategic partnerships and integrating its platform with a growing number of device manufacturers. Strategic alliances with leading mobile brands like Motorola, Nokia, ONE Store, Xiaomi, Telecom Italia Brazil, T-Mobile US and TIM have played a crucial role in extending Digital Turbine’s footprint across various regions and device ecosystems.

These relationships enable Digital Turbine to integrate its SingleTap and Ignite technologies directly into devices across dozens of countries, giving advertisers scale and seamless app distribution. Digital Turbine has also advanced its alternative app distribution efforts, strengthening its ecosystem through continued partnerships with mobile carriers and app-centric service providers, including Verizon, Epic, Microsoft and Pinterest.

The company’s App Growth Platform (“AGP”), which consists of Advertising Solutions and Ad Monetization Solutions, has become a major growth engine. Continuing growth in spending from leading advertising agencies and brand advertisers is driving its App Growth Platform. As brands increasingly shift ad spend toward mobile, APPS is capturing that demand with first-party data capabilities and expanding brand relationships. The company has broadened its AGP supply, moving beyond the traditional reliance on game publishers to a more diversified mix that now includes a significant share of non-gaming. With mobile app usage continuing to surge globally, this segment is well-positioned for scalable, high-margin growth.

Additionally, the company stands to gain from its initiatives to streamline operations, improve cost efficiency, and capitalize on platform migrations and system integrations completed earlier.

Digital Turbine, Inc. price-consensus-chart | Digital Turbine, Inc. Quote

However, Digital Turbine is not free of challenges. Despite record revenue per device, the softness in U.S. device volumes remains a headwind. With hardware upgrade cycles lengthening and consumer demand fluctuating, a sustained drop in device activations could limit APPS’ ability to expand its reach, especially for On-Device installs.

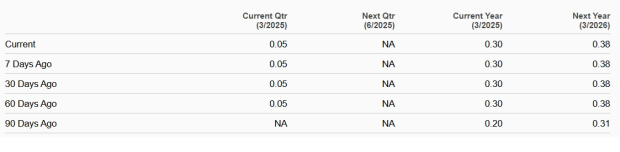

The recent estimate revision trends do not provide a clear direction. While the Zacks Consensus Estimate for APPS’ fiscal 2025 earnings has increased 50% over the past 90 days, there have been no revisions recently. Similar trends are also witnessed for fiscal 2026 earnings.

APPS’ earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 281.67%.(Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Magnitude - Consensus Estimate Trend

Digital Turbine is well-positioned for long-term growth, backed by strong advertiser demand and expanding global partnerships. Its On-Device Solutions and App Growth Platform remain key performance drivers, supported by operational efficiencies and strategic integrations. However, macroeconomic uncertainties and competitive pressures may limit the near-term upside. Given these mixed dynamics, a hold rating appears justified while awaiting clearer catalysts.

At present, Digital Turbine carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-20 | |

| Jul-14 | |

| Jul-13 | |

| Jul-13 |

AppLovin Stock Slides After Analyst Note On E-Commerce Ads Rollout

APP -12.65%

Investor's Business Daily

|

| Jul-13 | |

| Jul-13 | |

| Jul-10 | |

| Jul-10 | |

| Jul-08 | |

| Jul-08 | |

| Jul-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite