|

|

|

|

|||||

|

|

|

United Parcel Service UPS and Expeditors International of Washington EXPD are two major players in the Zacks Transportation sector. Despite ongoing economic uncertainty, both companies increased dividends this year, highlighting their commitment to rewarding shareholders.

Dividend-paying stocks offer a dependable income stream and are generally less prone to sharp price fluctuations. They are often considered reliable options for building wealth, as their payouts can help cushion the impact of economic instability — much like the conditions we are experiencing now.

In February, UPS’ board of directors authorized a dividend increase, raising the quarterly cash payout from $1.63 to $1.64 per share ($6.56 annually, up from $6.52).

United Parcel Service, Inc. dividend-yield-ttm | United Parcel Service, Inc. Quote

In May, Expeditors’ board approved a 5.5% boost to its semi-annual dividend, lifting the payment from 73 cents to 77 cents per share. The company maintains a payout ratio of 25. It has achieved a five-year dividend growth rate of 8%.

Expeditors International of Washington, Inc. dividend-yield-ttm | Expeditors International of Washington, Inc. Quote

UPS’ latest dividend increase certainly underscores the shareholder-friendly stance, but it also raises doubts about how sustainable that dividend is. The company’s high dividend payout ratio — the share of net income distributed as dividends — intensifies worries about its ability to keep funding payouts over the long run.

Investors may recall that during the early 2020s, when UPS benefited from booming business fueled by pandemic-era e-commerce growth, it returned substantial cash to shareholders through hefty dividends. However, free cash flow has been trending downward since reaching a peak of $9 billion in 2022.

UPS' elevated dividend payout is hurting its operational flexibility. By the end of 2024, free cash flow stood at $6.3 billion, only slightly above dividend payments of $5.4 billion. In the first nine months of 2025, the company generated only $2.7 billion in free cash flow and paid more than $4 billion in dividends. In contrast, EXPD’s much lower payout ratio suggests there are no similar concerns about the long-term durability of its dividend.

Having reviewed the dividend strength of these two transportation stocks, let’s now take a closer look at other key metrics to assess whether EXPD or UPS is the more attractive investment at this time.

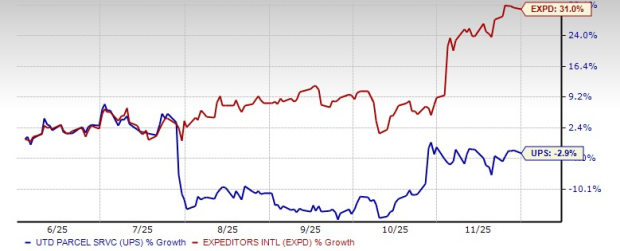

EXPD has navigated the recent tariff-induced stock market volatility well, registering a 31% gain over the past six months, while UPS stock has performed disappointingly in the same period.

UPS’ subdued stock performance is largely attributed to soft revenue trends, as geopolitical tensions and elevated inflation continue to weigh on consumer confidence and dampen growth expectations. The weakened demand environment has resulted in lower package-shipping volumes.

Conversely, EXPD’s recent momentum is supported by an improving airfreight landscape, with tonnage rising 4% year over year in the September quarter. The company’s cost-cutting measures have further strengthened its position. Expeditors is also benefiting from the expansion of the e-commerce and technology industries, underscoring its solid business fundamentals.

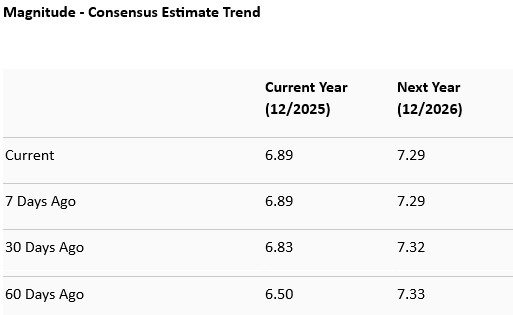

The Zacks Consensus Estimate for EXPD’s 2025 sales estimate implies a 3.9% year-over-year increase, while the same for 2026 indicates a 2.2% year-over-year decrease. The consensus mark for EXPD’s 2025 EPS estimate highlights a 3.5% year-over-year increase. The same for 2026 implies a 0.6% year-over-year increase.

The Zacks Consensus Estimate for UPS’ 2025 sales estimate implies a 3.4% year-over-year decrease, while the same for 2026 indicates a 0.07% year-over-year reduction. The consensus mark for UPS’ 2025 EPS estimate highlights a 10.7% year-over-year decrease. The same for 2026 implies a 5.7% year-over-year increase.

EXPD is trading at a forward sales multiple of 1.77X, with a Value Score of D. Meanwhile, UPS has a Value Score of B, with its forward sales multiple at 0.9X.

EXPD’s expensive valuation versus UPS indicates that investors are willing to pay a premium for this major transportation-sector player. While both companies emphasize dividends, EXPD’s lower dividend payout ratio eases worries about dividend sustainability, in contrast to UPS.

EXPD’s stronger price performance and upward earnings estimate revisions suggest that improving air freight tonnage — along with its cost-cutting measures — are yielding positive results. With better prospects overall, EXPD appears to be a more attractive choice than UPS at this time.While EXPD sports a Zacks Rank #1 (Strong Buy), UPS currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite