|

|

|

|

|||||

|

|

|

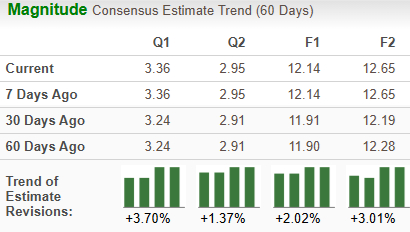

Earnings estimates for Qualcomm Incorporated QCOM for fiscal 2026 and fiscal 2027 have moved up 2% to $12.14 and 3% to $12.65, respectively, over the past 60 days. The positive estimate revision depicts bullish sentiments for the stock.

Qualcomm is increasingly benefiting from investments toward building a licensing program in mobile. The company is well-positioned to meet its long-term revenue targets driven by solid 5G traction, greater visibility and a diversified revenue stream. In addition, the chip manufacturer envisions solid growth opportunities within the mobile space, driven by the strength of its Snapdragon portfolio.

Leveraging processors with multi-core CPUs with cutting-edge features, amazing graphics and worldwide network connectivity, Qualcomm Snapdragon mobile platforms are fast with superb power efficiency. Smartphones and mobile devices built with Snapdragon mobile platforms enable immersive augmented reality and virtual reality experiences, brilliant camera capabilities, superior 4G LTE and 5G connectivity with state-of-the-art security solutions.

Qualcomm is currently foraying deeper into the realm of AI capabilities within the laptop and desktop business with the launch of the Snapdragon X chip for mid-range AI desktops and laptops. The strategy is aimed at moving beyond the slowing smartphone industry, which is its primary breadwinner. In addition to diversifying its revenue stream, this is likely to further extend QCOM’s AI footprint. The company intends to harness AI to meet increased demands for essential products and services that are the building blocks of digital transformation in a cloud economy.

The automotive telematics and connectivity platforms, digital cockpit and C-V2X solutions are fueling emerging automotive industry trends such as the growth of connected vehicles, the transformation of the in-car experience and vehicle electrification. Qualcomm is gaining traction in the vehicle-to-everything (V2X) communication systems market with the buyout of Autotalks. With seamless access to Autotalks’ comprehensive V2X expertise, Qualcomm has been able to offer an extensive suite of automotive-qualified global V2X solutions for installation in vehicles, as well as 2-wheelers and roadside infrastructure.

The company’s V2X chipsets offer production-ready standalone solutions that are purpose-built for global applications, resulting in direct communication becoming more pervasive. Automotive revenues rose 17% to a record high of $1.05 billion in fourth-quarter fiscal 2025, driven by increased content in new vehicle launches with the Snapdragon Digital Chassis platform, as automakers are deploying high-performance, low-power computing and connectivity chips to bring next-generation experience to consumers.

Qualcomm’s shares rose 9% over the past year compared with the industry’s growth of 71.2%. It has outperformed peers like Hewlett Packard Enterprise Company HPE, but lagged Broadcom Inc. AVGO. While Hewlett Packard was up 2.8%, Broadcom surged 122.6% over this period.

One-Year QCOM Stock Price Performance

The continued U.S.-China trade spat has dented Qualcomm’s growth potential. The chip-making firm has a significant presence in more than 12 cities in China, aiming to drive advancements in semiconductors and mobile telecommunications for the larger benefit. The company has been a key supplier of chips and other related components to local smartphone manufacturers like Xiaomi, Huawei and its spin-off brand Honor. However, it appears that Qualcomm is increasingly finding it difficult to maintain its operations in China.

The U.S. Commerce Department has long imposed various trade restrictions against China that banned the sale of high-tech equipment, chips, components and related technology to develop high-end smartphones and AI-enabled chips. As Washington tightens trade restrictions, Beijing has intensified its push for self-sufficiency in critical industries. This shift poses a dual challenge for QCOM, as it faces potential market restrictions and increased competition from domestic chipmakers. In addition, weaker spending across consumer and enterprise markets, especially in China, resulted in elevated customer inventory levels.

To add to the woes, Qualcomm's margins have declined over the years due to high operating expenses and R&D (research & development) costs. The company expects softness in the handset market and a weaker overall mix of devices to continue in the near future. The shift in the share among original equipment manufacturers at the premium tier has reduced the near-term opportunity to sell integrated chipsets from the Snapdragon platform.

In addition, Qualcomm faces stiff competitive pressures from rivals Broadcom and Hewlett Packard. Aggressive competition from low-cost chip manufacturers and established players in the mobile phone chipset market is also likely to hurt Qualcomm's profits. Although the global smartphone market is expected to maintain its momentum over the next three to four years, a major portion of this growth is likely to come from the low-cost emerging markets, which may weigh on Qualcomm's margins.

With robust automotive and Snapdragon traction, Qualcomm appears to be relatively better placed in terms of its portfolio strength. A strong emphasis on quality, diligent execution of operational plans and continuous portfolio enhancements are driving more value for customers. With rising earnings estimates, the stock is witnessing positive investor sentiment.

However, stiff competition and softness in key end markets are likely to put pressure on the bottom-line growth. High R&D costs erode its profitability to a large extent. Qualcomm is facing a tough operating environment in China amid escalating tariffs, raising questions about its long-term viability plans in the communist country. With a Zacks Rank #3 (Hold), Qualcomm appears to be treading in the middle of the road, and investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite