|

|

|

|

|||||

|

|

|

Visa Inc. V has always been treated as a stock priced on belief rather than strict fundamentals. Investors paid a premium for the company’s long-term promise, trusting its ability to shape the digital payments era. For years, that optimism made sense. Visa did more than process transactions. It built the rails that enabled modern commerce, worked with governments, set standards for interoperability and helped create the idea of global digital payments. In many markets, the company became the default name people associated with cards, travel and secure online spending.

But the landscape around Visa is changing fast. Competition is rising from two ends: nimble fintechs with new models and upgraded legacy systems moving closer to real-time settlement. Both groups are attacking pricing power and pushing for more transparent economics. Governments are also trying to break the Visa and Mastercard Incorporated MA duopoly by encouraging domestic rails, QR systems and central bank pilots. The growth of stablecoins adds another threat. Recent reports that Walmart and Amazon explored issuing their own USD-pegged stablecoins show how large platforms could bypass traditional networks and keep settlement economics inside their own ecosystems.

Visa isn’t pretending the threat does not exist. Since 2020, it has handled more than $140 billion in crypto and stablecoin flows, including more than $100 billion tied to user purchases. Over 130 stablecoin-linked card programs now operate on Visa across more than 40 countries. The company chose absorption over resistance, integrating digital currencies into its stack and turning disruption into learning, distribution and long-term positioning. It wants relevance no matter which technology becomes the dominant settlement layer.

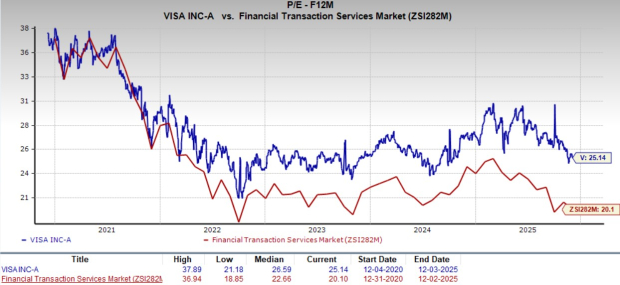

That leads to the core question for investors: Does today’s valuation still reflect the growth runway ahead? Visa trades at 25.14X forward 12-month earnings versus an industry average of 20.10X. It currently carries a Value Score of D, suggesting the stock is not cheap on paper. Yet the current level sits below the five-year median of 26.59X, which makes the valuation look more reasonable for long-term buyers than it did earlier. Relative to peers, Mastercard trades at 29.38X and American Express Company AXP at 21.17X, placing Visa squarely between premium and value.

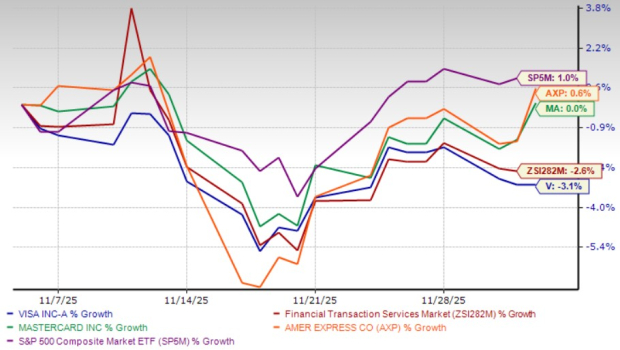

Over the past month, Visa shares have slipped 3.1%, trailing the industry’s 2.6% decline and the S&P 500’s 1% gain. Peers like Mastercard has remained stable, while American Expresshas risen 0.6% during this time.

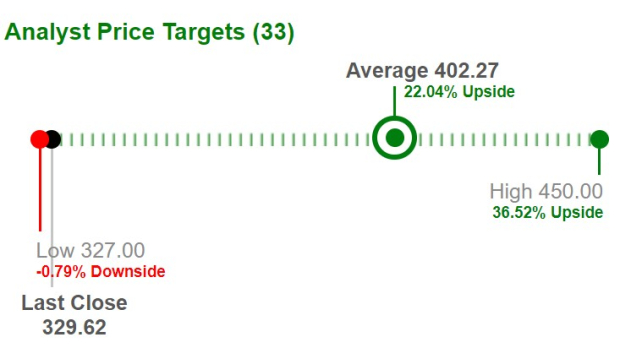

The pullback looks more like a reset after a strong performance rather than a shift in the story. The long-term narrative remains intact, supported by analyst targets.

Visa trades below the average analyst price target of $402.27, implying a potential upside of around 22%. The spread between the high target of $450 and the low target of $327 reflects different risk views, but the consensus direction remains positive.

Forecasts reinforce that optimism. The Zacks Consensus Estimate for fiscal 2026 and 2027 EPS suggests year-over-year growth of 11.7% and 13.3%, respectively. Revenue expectations show gains of 11% in 2026 and 10.6% in 2027. Visa beat earnings estimates in each of the past four quarters with an average surprise of 2.7%. The consistency comes from a model that monetizes transactions without taking credit risks.

Visa Inc. price-consensus-eps-surprise-chart | Visa Inc. Quote

Visa’s volume engine keeps pushing forward. In the last reported quarter, processed transactions rose 10% to 67.7 billion. Cross-border volumes increased 12%, driven by resilient travel demand, and payment volume climbed 9% on a constant-dollar basis. One of the fastest-growing segments is Value-Added Services (VAS). VAS revenues expanded 25% in constant currency to $3 billion. A few years ago, VAS was around 20% of Visa’s revenues. It is now approaching 30%, showing that the company is successfully diversifying beyond core processing into fraud tools, risk analytics, data and authentication.

Regulations, once a cloud over digital assets, may now work in Visa’s favor. The GENIUS Act created a framework for stablecoin settlement and clarified how companies can operate in the digital asset space. Visa now can settle across four stablecoins and four blockchains, which gives it a head start against banks constrained by legacy compliance systems. For smaller issuers, joining Visa’s network could become a shortcut to modernization without heavy infrastructure spending. Its network effects become stronger when regulation pushes complexity toward individual institutions, while Visa offers scale tools.

Visa continues to return capital. In the last reported quarter, it returned $6.1 billion to its shareholders, including $4.89 billion through buybacks and $1.2 billion via dividends. The remaining repurchase authorization stands at $24.9 billion. The dividend yield of 0.81% exceeds the industry average of 0.72%, and Visa’s history of dividend increases shows confidence in durable free cash flow.

Risks still exist. If Walmart and Amazon successfully launch stablecoins, others may follow and divert a slice of transaction volume, impacting interchange fees.

Visa also faces legal and legislative pressure. The U.S. DoJ’s antitrust lawsuit remains a cloud over the stock. Proposed legislation, such as the Credit Card Competition Act, couldreshape fee structures. Overseas, the U.K. tribunal ruling against interchange fees adds uncertainty. The U.K.'s Payment Systems Regulator is also looking for a fee cap to curb market concentration.

For now, the debate around Visa is mostly about timing. The competitive landscape is shifting fast, but the company’s adaptability, scale advantages and growing layer of value-added services give it a credible path to remain the backbone of global digital payments. The valuation premium may not have disappeared, but today it feels more earned than assumed. Even with a Zacks Rank #3 (Hold), the setup reflects a balanced view: near-term competitive pressures on one side and durable network economics on the other. New technologies are emerging, but trust, regulatory clarity, interoperability at scale and decades of partner integration still matter.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite