|

|

|

|

|||||

|

|

|

PVH Corporation PVH posted third-quarter fiscal 2025 results, wherein both revenues and earnings topped the Zacks Consensus Estimate. However, the bottom line fell year over year, while the top line increased.

PVH delivered a solid third quarter, surpassing guidance on reported revenues, operating margin and EPS, with constant-currency revenues matching expectations. Results reflected disciplined execution of the PVH+ Plan and sustained brand strength across Calvin Klein and Tommy Hilfiger, supported by stepped-up product innovation and impactful global marketing initiatives.

Management reaffirmed its full-year constant-currency revenue and margin outlook and narrowed projections for reported revenues and non-GAAP EPS toward the high end of prior ranges, signaling confidence in its brand momentum and ongoing cost-efficiency gains. Notably, PVH continues to benefit from SG&A savings unlocked through its multi-year Growth Driver 5 program.

Looking ahead, PVH is focused on accelerating innovation within core product categories, expanding globally resonant marketing campaigns and enhancing marketplace execution across key regions. These initiatives, coupled with a strengthened demand-driven supply chain, are expected to reinforce brand relevance through the back half of 2025 and support the company’s long-term strategic growth framework.

PVH Corp reported adjusted earnings of $2.83 per share, down 6.6% from the year-ago quarter's $3.03. However, the bottom line surpassed the Zacks Consensus Estimate of earnings of $2.56 per share and the company’s guidance of $2.35-$2.50.

PVH Corp. price-consensus-eps-surprise-chart | PVH Corp. Quote

Revenues jumped 2% year over year (down 1% at constant currency) to $2.29 billion and beat the consensus mark of $2.26 billion.

Direct-to-consumer revenues were flat compared with the prior-year period’s figures (down 1% on a constant-currency basis). Revenues in PVH Corp’s owned and operated also delivered flat growth, though revenues declined 2% in constant currency, as gains in APAC were outweighed by softer results in the Americas and EMEA. Meanwhile, owned and operated digital commerce grew 1%, and was flat in constant currency, with increases in the Americas and APAC offset by declines in EMEA.

Wholesale revenues climbed 4% from the prior-year period (up 1% on a constant-currency basis), buoyed by growth in the Americas, partially offset by decreases in EMEA and APAC.

The company’s gross profit of $1.29 billion dipped 1.81% year over year. The gross margin contracted 210 basis points to 56.3% due to the higher U.S. tariffs, elevated promotional environment, margin pressure from bringing previously licensed women’s categories in-house and increased freight costs, along with added discounts tied to Calvin Klein delivery delays.

Adjusted selling, general and administrative expenses were $1.09 billion, up 0.8% year over year. The company’s adjusted earnings before interest and taxes totaled $202.3 million, down 14.5% from the prior-year quarter.

EMEA revenues increased 4% year over year to $1.11 billion. However, on a constant-currency basis, revenues declined 2% due to softness in both the direct-to-consumer and wholesale businesses. The consensus estimate for EMEA revenues was pegged at $1.09 billion.

Americas revenues rose 2% year over year to $682.8 million, driven by growth in the wholesale business, somewhat offset by a decline in the direct-to-consumer business. Wholesale gains reflected the shift of previously licensed women’s categories in-house, though this was partially offset by last year’s wholesale shipments being more concentrated in the back half of the year. The consensus estimate for Americas revenues was pegged at $676 million.

APAC revenues decreased 1% year over year to $391.9 million (flat on a constant-currency basis). In constant currency, direct-to-consumer growth was fully offset by a decline in the wholesale business. The consensus estimate for APAC revenues was pegged at $383 million.

Licensing revenues fell 11% year over year due to the transition of some previously licensed women’s product categories in-house.

Revenues for the Calvin Klein segment increased 2% year over year (flat on a constant-currency basis).

Revenues for the Tommy Hilfiger brand rose 1% year over year (down 2% on a constant-currency basis).

The Heritage Brands segment’s revenues fell 3.1% year over year.

PVH Corp ended the fiscal third quarter with cash and cash equivalents of $158.2 million, long-term debt of $2.25 billion and stockholders’ equity of $4.87 billion. Inventories were up 3% year over year, marking a meaningful improvement versus the increase seen in the second quarter of 2025. The current increase also includes a 2% impact from higher tariffs.

As part of its plan to return extra cash to shareholders, the company bought back 5.4 million shares for $561 million in the first quarter using accelerated share repurchase (ASR) programs and open-market purchases. In the third quarter, those ASR programs were finalized, and the company received another 2.3 million shares. Altogether, PVH repurchased 7.7 million shares in the first nine months of 2025. The company did not spend any money on share buybacks in the second or third quarters.

For the fiscal fourth quarter, revenues are expected to rise modestly, reaching low single-digit growth compared to the fourth quarter of 2024, though it will be slightly lower on a constant-currency basis.

Adjusted earnings per share are expected to be $3.20-$3.35 compared with the $3.27 earned in the year-ago quarter. This EPS outlook reflects an estimated net negative impact from current U.S. tariffs, including an unmitigated impact of roughly $0.60, partially offset by planned mitigation actions, as well as an estimated positive impact of about $0.20 from foreign currency translation.

Interest expenses are projected to increase to $20 million from the $14 million reported in the fourth quarter of fiscal 2024 due to the impacts of funding the accelerated share repurchase agreements. The adjusted effective tax rate is projected to be 22%.

For fiscal 2025, PVH is narrowing its revenue outlook to low single-digit growth, reaffirming expectations for flat to slightly higher revenues on a constant-currency basis. It anticipates the adjusted operating margin to be 8.5%, whereas it reported 10% in fiscal 2024.

Management envisions an adjusted EPS of $10.85-$11.00, up slightly from the previous range of $10.75 to $11.00, whereas it delivered $11.74 in fiscal 2024. The EPS guidance for fiscal 2025 reflects an unfavorable impact of $1.05 from tariffs, partly offset by a favorable impact of about 45 cents from foreign-currency translation.

Interest expenses are projected to increase to $80 million from the $67 million reported in 2024 due to the impacts of funding the accelerated share repurchase agreements. The adjusted effective tax rate is projected to be 22%.

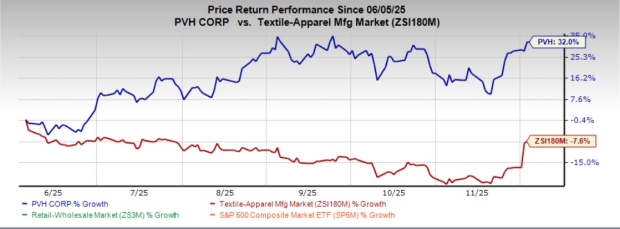

This Zacks Rank #4 (Sell) company’s stock has gained 32% in the past six months against the industry's 7.6% drop.

Ralph Lauren Corporation RL designs, markets and distributes lifestyle products in North America, Europe, Asia and internationally. It currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for RL’s current fiscal-year sales and earnings indicates growth of 9.5% and 24.9%, respectively, from the year-ago reported figures. Ralph Lauren delivered a trailing four-quarter average earnings surprise of 9.8%.

Revolve Group, Inc. RVLV operates as an online fashion retailer for millennial and Generation Z consumers in the United States and internationally. It carries a Zacks Rank #2 at present. Revolve Group delivered a trailing four-quarter average earnings surprise of 61.7%.

The Zacks Consensus Estimate for RVLV’s current fiscal-year revenues implies growth of 6.8% from the year-ago actuals.

Kontoor Brands, Inc. KTB, a lifestyle apparel company, designs, produces, procures, markets, distributes and licenses denim, apparel, footwear and accessories. It currently carries a Zacks Rank #2. KTB delivered a trailing four-quarter earnings surprise of 14%, on average.

The Zacks Consensus Estimate for Kontoor Brands’ current financial-year sales and earnings indicates growth of 19.4% and 12.5%, respectively, from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-28 | |

| Jul-28 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-16 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite