|

|

|

|

|||||

|

|

|

CorMedix’s CRMD lead therapy, DefenCath (taurolidine + heparin), is currently the company’s majority revenue driver.

The FDA approved DefenCath in late 2023 as the first and only antimicrobial catheter lock solution available in the United States. It is indicated to lower the risk of catheter-related bloodstream infections (CRBSIs) in adults with kidney failure undergoing chronic hemodialysis via a central venous catheter.

CRBSIs can delay treatment and raise healthcare costs through extended hospital stays, intensive therapies and higher mortality. With DefenCath, CorMedix aims to meet this critical unmet medical need. DefenCath was launched in 2024 in both the hospital inpatient and outpatient hemodialysis settings.

In the first nine months of 2025, DefenCath recorded $167.6 million in net sales, reflecting strong market adoption. Importantly, DefenCath holds a unique market position as the only FDA-approved therapy for a niche condition, supported by patent protection through 2033. This exclusivity offers a long runway for revenue generation.

Heading into the new year, sales are expected to grow steadily as CRMD expands its commercial footprint and strengthens its marketing infrastructure, driving continued momentum for DefenCath. CorMedix is also planning future potential label expansion of DefenCath into total parenteral nutrition to increase its customer base.

Besides DefenCath, CorMedix is also gaining momentum from its $300 million acquisition of Melinta Therapeutics — a strategic move designed to expand its revenue streams and deepen its footprint in hospital acute care and infectious disease markets. The transaction brought in seven approved products, including Rezzayo, which is currently in late-stage studies for preventing invasive fungal infections.

These acquired products from Melinta contributed $12.8 million to CRMD’s top line during the third quarter of 2025, representing its partial quarter sales.

Reflecting the growing momentum with DefenCath and early Melinta portfolio contributions, the company raised its full-year 2025 pro forma net revenue guidance to $390-$410 million, up from the prior expectation of at least $375 million.

Though CorMedix is riding on the success of DefenCath, stiff competition looms due to the presence of larger players already active in the heparin market.

DefenCath combines taurolidine, an antimicrobial agent, with heparin in a fixed-dose formulation tailored for a specific subset of kidney failure patients. Although CorMedix currently holds a first-mover advantage in the United States with DefenCath, the broader competitive environment still poses risks. Major players such as Pfizer PFE, Amphastar Pharmaceuticals AMPH, B. Braun, Baxter and Fresenius Kabi USA already market heparin for multiple uses. Given their stronger pipelines, larger manufacturing capabilities and greater financial resources, these companies could quickly become significant competitors if they decide to target CRBSI-related indications — a move that could challenge CorMedix’s market advantage and affect its long-term growth outlook.

Pfizer, which markets Heparin Sodium Injection for a wide range of clinical applications — including dialysis, surgical procedures, and thrombosis management — could use its global scale and clinical expertise to move into the CRBSI prevention segment. Amphastar Pharmaceuticals, meanwhile, manufactures Enoxaparin and controls its entire production chain from API to finished product, giving it the operational efficiency and technical capabilities to pursue similar opportunities. If either Pfizer or Amphastar expands its anticoagulant portfolio into catheter-related infection prevention, CorMedix could encounter significant competitive pressure within its primary therapeutic space.

Shares of CorMedix have rallied 31.3% so far this year compared with the industry’s growth of 19.9%. The stock has also outperformed the sector and the S&P 500 index during the same time frame, as seen in the chart below.

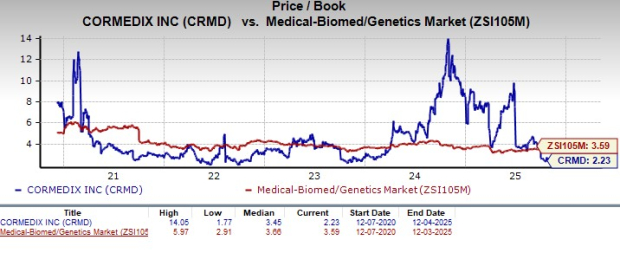

From a valuation standpoint, CorMedix is trading at a discount to the industry. Going by the price/book ratio, the company’s shares currently trade at 2.23, lower than 3.59 for the industry. The stock is also trading below its five-year mean of 3.45.

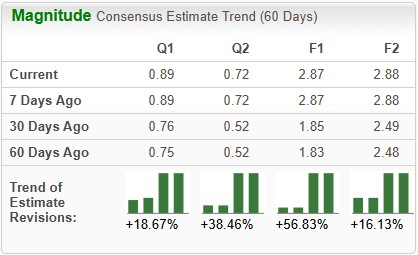

Estimates for CorMedix’s 2025 earnings have improved from $1.83 to $2.87 per share in the past 60 days, and estimates for 2026 earnings have improved from $2.48 to $2.88 over the same timeframe.

CorMedix currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite