|

|

|

|

|||||

|

|

|

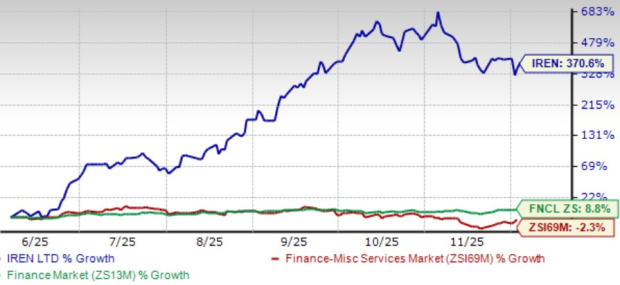

IREN Limited IREN shares have skyrocketed 370.6% over the past six months, outpacing the broader Zacks Finance sector’s return of 8.8% and the Financial - Miscellaneous Services industry’s fall of 2.3%.

IREN’s explosive run might look enticing, yet rapid momentum often masks underlying risks. Let’s examine if the stock’s heightened strength presents an opportune moment to shift risk-off and secure gains.

IREN's long-term profitability is facing significant pressure due to exceptionally high capital expenditure requirements associated with its rapid AI cloud expansion. The Microsoft MSFT deal alone requires $5.8 billion in GPU capital expenditures, with an additional $1.4 billion that must be sourced from cash, operating flow, equity, convertible notes and corporate debt. Since a large portion of future recurring revenues depends on this single Microsoft agreement, any delay, change or cancellation could significantly impact revenue stability and long-term earnings.

Even after 20% customer prepayments, IREN will need to secure approximately $2.5 billion in financing against the GPU and compressed cash flow, which will increase future interest obligations and balance-sheet risk.

Beyond that, accelerated construction at Childress — which includes Tier-3 design upgrades, liquid-cooling infrastructure and high-density racks — introduces significant incremental construction costs with long payback cycles. Additional expansion plans across British Columbia and Sweetwater further increase long-term capital needs, requiring ongoing funding to complete multi-phase sites through 2026 and beyond.

These extensive and recurring capex obligations elevate financing risk and may compress free cash flow, placing sustained pressure on long-term profitability.

IREN’s aggressive expansion into AI cloud and high-performance computing introduces heightened execution risk, given the company’s limited operating experience in these emerging markets. Management acknowledges this gap, noting that IREN is still in the early stages of AI cloud and HPC services and must operate in rapidly changing industries where customer needs, technology cycles and pricing structures evolve rapidly.

The transition of entire sites from Application-Specific Integrated Circuit mining to GPU-based AI infrastructure further adds operational risk, as large-scale deployments across British Columbia and Childress require new capabilities in liquid cooling, cluster orchestration and high-density data-center management. Success depends on building and consolidating a new customer base and managing counterparty risk, especially since future ARR targets depend on deals that have not yet been fully secured or demonstrated at scale.

The shift to AI and HPC puts IREN Limited in direct competition with several rapidly advancing players. Applied Digital APLD and TeraWulf WULF are both transitioning from crypto mining to AI infrastructure and becoming major competitors in the AI/HPC market. Applied Digital is strengthening its position with purpose-built AI and HPC data centers and a major partnership with CoreWeave.

At the same time, TeraWulf is expanding its high-performance computing footprint through a partnership with Fluidstack, an AI cloud platform focused on HPC clusters. Applied Digital and TeraWulf are growing fast, and IREN must keep up. With TeraWulf and Applied Digital moving quickly into AI data centers, competition is getting tougher.

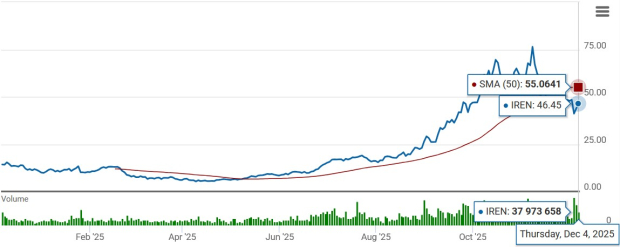

IREN Limited is also trading below the 50-day moving average, indicating a bearish trend, suggesting limited upside in the near-term momentum for the stock.

The Zacks Consensus Estimate for IREN’s fiscal 2025 earnings is currently pegged at 79 cents per share, reflecting a strong 36.2% upward revision over the past 30 days. However, this optimism is tempered by a sharp 70% downward revision to fiscal 2026 earnings, highlighting a mixed trend in the company’s earnings outlook.

Over the trailing four quarters, the company’s earnings missed the Zacks Consensus Estimate thrice and beat once, the average negative surprise being 26.52%.

Despite IREN’s impressive rally and long-term potential, the near-term setup remains unfavorable. The company faces substantial capex commitments, mounting financing needs, execution risks in its rapid transition to AI/HPC markets and growing competition from peers scaling even faster. Earnings estimates also reflect uncertainty, with sharp downward revisions for fiscal 2026. Combined with operational risks, customer concentration and a bearish technical trend, the stock’s risk-reward profile is tilted to the downside. Until IREN successfully executes its large-scale AI strategy, investors may find it prudent to stay away from this Zacks Rank #5 (Strong Sell) stock for now.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite