|

|

|

|

|||||

|

|

|

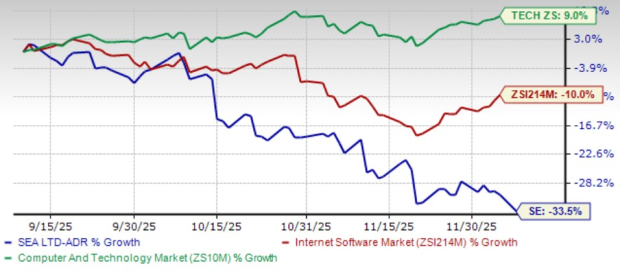

Sea Limited SE shares have lost 33.5% in the past three months, lagging the broader Zacks Computer & Technology sector’s growth of 9% and the Zacks Internet - Software industry’s decline of 10%.

The decline in share price is caused by weak logistics and value-added services revenues, indicating high competition and rising costs. Intense e-commerce competition continues to put pressure on margins. Currency fluctuations and softer economic conditions in emerging markets also hurt results.

Now the question arises: Should investors continue to hold the stock, or exit before losses deepen? Let’s assess the situation more thoroughly.

The competitive landscape is becoming increasingly challenging for Sea Limited as rivalry across e-commerce, digital entertainment and digital financial services continues to intensify across its key markets.

Shopee remains a leading platform but faces sustained pressure from Lazada, owned by Alibaba BABA, as Alibaba competes aggressively on pricing, logistics speed, seller incentives and technological capabilities. This forces Shopee to continue heavy spending on subsidies, delivery infrastructure and marketing to defend market share, raising costs and limiting margin expansion despite healthy GMV growth.

In digital financial services, Monee faces strong competition from regional fintech ecosystems and super-apps like Grab Holdings GRAB. Originally a ride-hailing and delivery platform, Grab Holdings has expanded aggressively into digital payments and financial services, positioning it as a direct, cross-segment competitor to SE’s fintech and digital-payments business. This rivalry increases user acquisition costs and regulatory and credit risk exposure. At the same time, merchant advertising and content-led commerce are becoming more competitive, with Alibaba and Grab Holdings strengthening their seller tools and media capabilities, increasing pressure on ad spend and engagement.

In the global gaming market, Garena competes directly with industry leaders, including Take-Two Interactive TTWO. With franchises such as Grand Theft Auto, Red Dead Redemption and NBA 2K, Take-Two Interactive sets high standards for content quality and engagement. Even with strong titles, Take-Two Interactive’s reliance on a few releases creates risk. Overall, Southeast Asia and Latin America remain fragmented and highly competitive markets where leadership is constantly challenged.

Rising cost structure is emerging as a significant risk for Sea Limited as expense growth continues and, in some cases, even outpaces revenue expansion. In the third quarter of 2025, the total cost of revenues rose more than 37% year over year, driven largely by higher logistics expenses in e-commerce as order volumes expanded and delivery services scaled across Southeast Asia.

Cost pressures are also evident in other segments. Digital entertainment saw higher payment channel fees and increased royalties tied to third-party IP collaborations, while digital financial services faced rising server, hosting and collection-related costs as the loan book expanded rapidly.

Additionally, sales and marketing expenses increased nearly 31% year over year, reflecting intensifying competition and ongoing investments to sustain growth, which could constrain margin expansion over the long term.

The Zacks Consensus Estimate for SE’s fourth-quarter 2025 earnings is pegged at 94 cents per share, down by 6.9% over the past 30 days.

Likewise, the consensus mark for first-quarter 2026 earnings has been revised down to $1.35 per share, reflecting a 9.4% decline over the past 30 days.

SE has struggled to deliver consistently strong quarterly performance. Its bottom line missed the Zacks Consensus Estimate in each of the trailing four quarters, the average negative surprise being 16.09%.

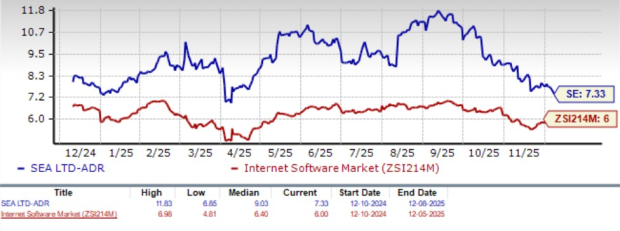

Sea Limited's stock appears to be overvalued at the moment, as indicated by its Zacks Value Score of F. Its trailing 12-month price-to-book (P/B) ratio of 7.33X stands well above the industry average of 6.0X, indicating that the stock is priced at a significant premium to its underlying book value.

This elevated valuation is largely driven by strong investor optimism around growth in terms of Shopee’s GMV expansion and a sharp rebound in Garena’s bookings. However, such optimism increases downside risk, since execution challenges, margin headwinds, or slower growth may lead to multiple contractions.

SE shares also look overvalued compared with key Southeast Asian competitors. Alibaba, Grab Holdings and JD.com trade at valuation multiples of 2.44X, 3.21X and 1.00X, respectively.

Given mounting competitive pressures, rising costs that are outpacing revenue growth, downward earnings revisions and a stretched valuation, Sea Limited’s risk-reward profile has weakened significantly. Persistent margin pressure in Shopee, intensifying fintech and gaming competition and consistent earnings misses further cloud near-term visibility. With modest upside potential and heightened downside risks in a challenging macro environment, SE no longer presents a compelling investment case.

SE currently carries a Zacks Rank #5 (Strong Sell), suggesting that investors should stay away from this stock right now.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 11 hours | |

| 17 hours | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite