|

|

|

|

|||||

|

|

|

DICK'S Sporting Goods, Inc. DKS delivered strong comps momentum, driven by robust category trends and disciplined execution, in third-quarter fiscal 2025. The DICK’S business posted a 5.7% comparable sales (comps) increase in the fiscal third quarter, driven by a 4.4% rise in average ticket and a 1.3% increase in transactions. This momentum was broad-based across footwear, apparel and hardlines, categories that continue to benefit from heightened focus on sport, active lifestyles and back-to-sport demand.

Management highlighted that consumers remain deeply engaged in athletic and lifestyle categories, fueling healthy average ticket and transaction growth. The retailer’s access to premium and emerging brands, paired with high-performing vertical labels, is keeping its assortment fresh and relevant.

However, category strength alone isn’t the only engine sustaining momentum. DICK’S has been actively reinforcing the fundamentals behind its comp outperformance. Transformative real estate concepts, including House of Sport and Field House, are lifting engagement and productivity, while helping the company extend its reach into experience-led retail. The retailer opened 13 House of Sport locations in the fiscal third quarter, the largest quarterly rollout to date, alongside six new Field House stores, bringing the total stores to 35 and 42, respectively.

These next-generation formats are also unlocking deeper partnerships with national brands, enhancing product flow and exclusivity. The expansion of trading cards and collectibles, a fast-growing category introduced through Fanatics, adds another high-energy growth pillar.

Complementing store growth, the company’s multibillion-dollar e-commerce business remains another structural driver, reinforcing DICK’S Sporting’s omnichannel strength. Digital gains are outpacing the overall business through enhancements such as app-exclusive launch reservations, app-led engagement, better personalization capabilities and increased youth sports engagement through GameChanger.

The company’s raised full-year guidance underscores confidence that these drivers can sustain performance even as the macro environment remains fluid. Management expects fiscal 2025 comps growth of 3.5–4% for the DICK’S business, up from the prior 2–3.5% growth, citing confidence in assortment quality and holiday execution. DKS now expects DICK’S business EPS of $14.25–$14.55, with operating margin around 11.1% at the midpoint, underscoring continued profitability even as the company invests heavily in digital capabilities, marketing and store growth.

While strong category momentum provides a favorable backdrop, it is DICK’S strategic execution, differentiated assortment and omnichannel strength that ultimately cement its comps trajectory. Combined, these factors suggest DKS can continue defending, and potentially expanding, its comps advantage heading into fiscal 2026.

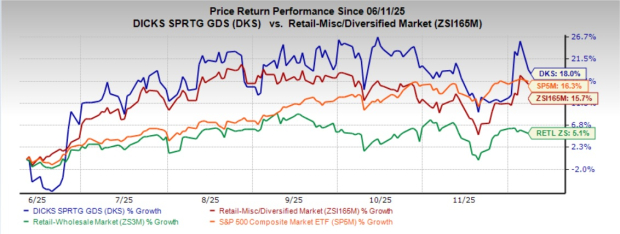

Shares of this Zacks Rank #3 (Hold) company have gained 18% in the past six months, outperforming the industry’s 15.7% growth, the broader Retail-Wholesale sector’s 5.1% increase and the S&P 500’s 16.3% growth.

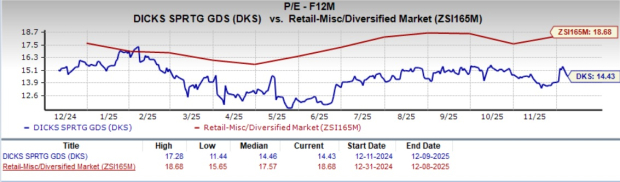

DKS shares are currently trading at a forward 12-month price-to-earnings (P/E) multiple of 14.43X, a discount compared with the industry’s average of 18.68X. At this level, DKS is offering compelling value to investors looking for exposure to the retail sector.

American Eagle Outfitters AEO operates as a multi-brand specialty retailer in the United States and internationally, and currently sports a Zacks Rank #1 (Strong Buy). AEO delivered a trailing four-quarter earnings surprise of 35.1%, on average. You can see the complete list of today's Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for American Eagle’s current fiscal-year sales indicates a rise of 1.8% from the year-ago period reported number. Meanwhile, the consensus mark for EPS suggests a decline of 25.3%.

Boot Barn Holdings BOOT operates specialty retail stores in the United States and internationally, and carries a Zacks Rank #2 (Buy) at present. BOOT delivered a trailing four-quarter earnings surprise of 5.4%, on average.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales and earnings indicate growth of 16.2% and 20.5%, respectively, from the year-ago reported numbers.

Stitch Fix, Inc. SFIX engages in the provision of clothing and accessories in the United States, and currently carries a Zacks Rank of 2. SFIX delivered an average earnings surprise of 37.7% in the last four quarters.

The Zacks Consensus Estimate for Stitch Fix’s current financial-year sales and EPS indicates a growth of 6.4% and 4.6%, respectively, from the year-ago figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-10 | |

| Jul-09 | |

| Jul-06 | |

| Jul-03 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 | |

| Jul-01 | |

| Jul-01 | |

| Jul-01 | |

| Jun-26 | |

| Jun-24 | |

| Jun-22 | |

| Jun-19 | |

| Jun-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite