|

|

|

|

|||||

|

|

|

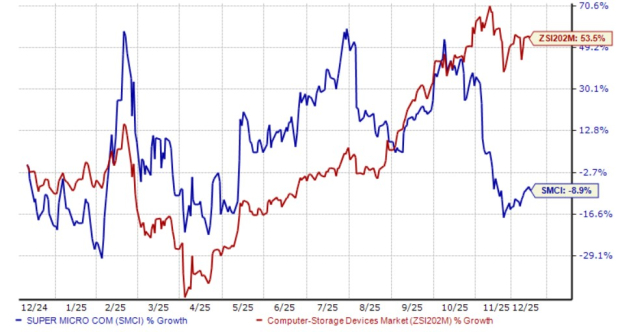

Super Micro Computer SMCI shares have lost 8.9% in the past year, underperforming the Zacks Computer- Storage Devices industry’s return of 53.5%. This decline in share price raises the question: Should investors hold the stock tight or exit it right now?

The decline in SMCI’s share price can be attributed to declining revenues and shrinking margins. SMCI’s first-quarter revenues and earnings declined 15.5% and 56%, respectively. However, this decline in first-quarter fiscal 2026 revenues occurred not because of demand weakness but mainly due to a revenue shift from the September quarter to the December quarter due to last-minute configuration upgrades as requested by SMCI’s customers.

Other problems faced by the company include SMCI’s customer concentration, and new deals with larger customers have also squeezed its margin, as it needs to retain these customers. These mega deals have also resulted in higher receivables, resulting in negative free cash flow of $950 million for the first quarter of fiscal 2026.

Super Micro Computer’s working capital problem also stems from the massive operational scale-up required to meet unprecedented AI rack demand. SMCI plans to roll out 6,000 racks/month, including 3,000 liquid-cooled racks and expand new facilities in Taiwan, the Netherlands, Malaysia, and the Middle East.

SMCI’s rapid expansion is also causing inventory accumulation. SMCI’s first-quarter fiscal 2026 closing inventory was $5.7 billion, up from $4.7 billion in the previous quarter. This situation has spiked its cash conversion cycle from 96 days to 123 days.

SMCI’s bottom-line decline was due to a combination of these factors. SMCI projects a sequential decline of 300 basis points in its gross margin in the second quarter of fiscal 2026. The Zacks Consensus Estimate for Super Micro Computer’s second-quarter fiscal 2026 earnings is pegged at 49 cents per share, suggesting a year-over-year decline of 19.7%. The estimates have remained the same in the past 30 days.

Rising competition from the leading companies in the storage and server space, such as Pure Storage PSTG, Dell Technologies DELL and Hewlett Packard Enterprise HPE, is a concern for investors.

In the storage space, Pure Storage offers a range of modern storage solutions through its offerings like FlashArray, FlashBlade and Pure Cloud Block Store to serve the purpose of providing All-Flash performance, cloud integration, AI and simplified management.

In the AI-optimized server space, Dell Technologies is a strong competitor. Hewlett Packard Enterprise also offers a range of server services, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. Growing price competition and price adjustments are a concern for the company as competition rises. However, not everything is gloom and doom for the company.

Super Micro Computer’s high-performance and energy-efficient servers are gaining traction among AI data centers, HPC and hyperscalers. Partnerships with vendors like NVIDIA and Advanced Micro Devices position Super Micro Computer to deliver the latest GPU-powered platforms, which remain in high demand among cloud providers and sovereign AI projects. Expansion in Europe, Asia and the Middle East also offers additional growth avenues.

SMCI’s Data Center Building Block Solutions (DCBBS) solution is experiencing rapid growth in demand for its advanced AI compute and data center solutions, especially powered by NVIDIA’s Blackwell Ultra (GB300) and AMD MI350/355X platforms. On its first-quarter fiscal 2026 earnings call, SMCI reported that DCBBS is expected to carry more than 20% margins and become a major long-term profit contributor in its business.

SMCI has also been the first to ship next-generation AI systems, such as the NVIDIA B300 and GB300, introducing DCBBS, DLC-2 and more than 30 new solutions optimized for the latest NVIDIA and AMD architectures. Furthermore, in 2025, it introduced new product families like SuperBlade and MicroBlade high-density server systems focused on AI inference, visual computing, EDA, data analytics, HPC, cloud, and enterprise workloads.

SMCI has also launched edge systems on display with an integrated NVIDIA Jetson Orin NX AI computer. They are SYS-112D-42C-FN8P and ARS-E103-JONX. SMCI has also introduced DLC-2, which lowers power and water consumption by up to 40%, operates at significantly reduced noise levels of approximately 50 decibels, and reduces the total cost of ownership by 20%. With all these products in line, SMCI aims for $36 billion in fiscal 2026 revenues.

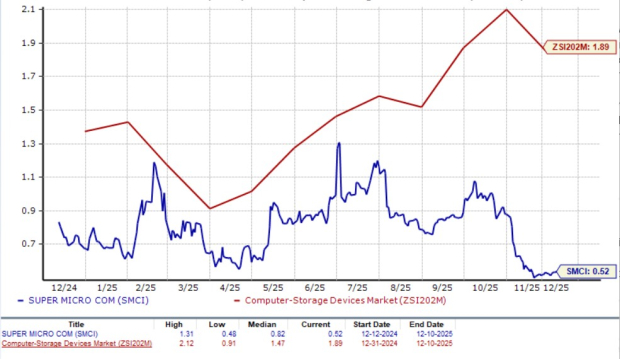

Super Micro Computer is currently trading at a discounted valuation, with its forward 12-month price-to-earnings (P/S) ratio at 0.52X, which is lower than the Zacks Computer and Technology sector’s average of 1.89X. This is also reflected in the Zacks Value Score of the stock, as it carries a Value Score of B.

Super Micro Computer is facing several near-term challenges while pursuing long-term growth across server, storage and cooling products. Although the company has returned massively in the year-to-date period and is still favorably valued, considering its margin compression, we suggest investors retain this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 10 hours |

Stocks to Watch: Berkshire Hathaway, Super Micro Computer, Sunrise Energy

SMCI

The Wall Street Journal

|

| 10 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 12 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite