|

|

|

|

|||||

|

|

|

Duolingo, Inc. DUOL has been facing heavy selling pressure, sliding 59% over the past six months. This sharp decline stands out when compared to the broader industry, which climbed 20% in the same period and the Zacks S&P 500 composite, which advanced 17%. The performance gap highlights just how much Duolingo has lagged behind the market and its peers.

Competitors like Coursera COUR and Chegg CHGG have been moving in the same direction. Coursera has declined 4% over the past six months, while Chegg has dipped 36%. The contrasting trajectories of Coursera and Chegg versus Duolingo point to significant shifts in investor sentiment within the online learning space.

This pullback raises the question: Is Duolingo setting up for a recovery, or could further weakness be ahead? With Duolingo sliding along with Coursera and Chegg, you need to carefully weigh whether now is the right time to consider the stock.

Let us help you…

DUOL’s rise as a dominant player in digital education is deeply rooted in its effective use of artificial intelligence and proprietary learner data. Unlike many tech firms that view AI as a long-term aspiration, Duolingo integrates it at the core of its business model, from content creation to cost management, making it both a product and a financial growth driver.

With one of the world’s largest datasets of language learners, Duolingo leverages data to refine personalization, improve user engagement, and expand new learning verticals such as music and chess. This data advantage forms a strong competitive moat, enabling Duolingo to deliver adaptive learning experiences that are difficult for rivals to replicate. AI not only enhances learner outcomes but also drives significant operational efficiencies.

Equally impressive is Duolingo’s ability to scale content creation. In April, it introduced 148 new language courses, its largest expansion ever. For perspective, the company took more than a decade to develop its first 100 courses, but AI-driven tools now allow it to produce nearly 150 within a single year. This acceleration in content development reinforces its brand leadership and deepens user trust by consistently offering new learning opportunities.

In essence, Duolingo’s synergy of AI-driven personalization, proprietary data and cost-efficient scalability positions it as a transformative force in education technology. As global demand for accessible digital learning continues to expand, Duolingo’s sustainable growth model and innovation-led profitability make it an attractive long-term investment opportunity.

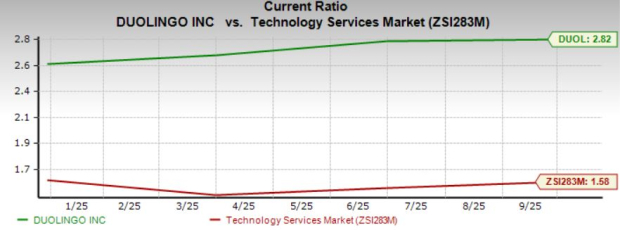

Duolingo's liquidity position is also robust, with a current ratio of 2.82 at the end of the third quarter of 2025 compared to the industry’s 1.58. A current ratio above 1 indicates that Duolingo is well-positioned to meet its short-term obligations, providing a buffer against potential financial challenges.

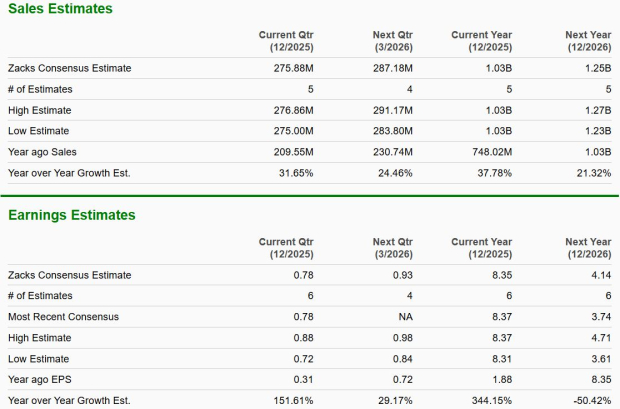

Looking ahead, the Zacks Consensus Estimate for Duolingo's 2025 earnings is set at $8.35, indicating an impressive 344% year-over-year increase. The company's sales are expected to grow 38% in 2025.

This positive outlook is reinforced by upward estimate revisions. In the past 60 days, six estimates for 2025 earnings have been revised upward with no downward revisions, reflecting strong analyst confidence in the company. The Zacks Consensus Estimate for 2025 earnings has increased by more than 100% during this period.

Despite Duolingo’s significant share-price decline over the past six months, its forward 12-month P/E ratio of 45.21X remains far above the industry’s 27.24X. This elevated multiple suggests the stock is still trading at a substantial premium relative to peers. When a valuation stays this stretched even after a meaningful correction, it raises the risk of further downside if revenue growth, user additions, or guidance show any softness. Until the multiple compresses closer to industry levels, DUOL may continue to face pressure as investors reassess how much premium future growth truly deserves.

Duolingo’s steep six-month decline makes the stock look tempting, but a balanced view suggests a hold is more appropriate for now. The company continues to benefit from strong AI integration, rapid content expansion, and a clear data advantage, all of which support long-term growth potential. However, the recent slide shows how sharply sentiment has shifted in the online learning space, and the stock still trades at a noticeably rich valuation even after the correction. This leaves room for additional volatility if growth trends soften or the market stays cautious toward ed-tech names. A wait-and-watch approach is prudent until valuation cools and market stability improves.

DUOL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite