|

|

|

|

|||||

|

|

|

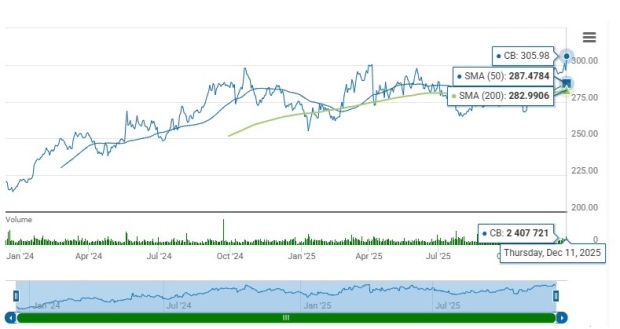

Shares of Chubb Limited CB closed at $305.98 on Thursday, near its 52-week high of $308.31. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

The stock is trading above the 50-day and 200-day simple moving averages (SMA) of $286.99 and $283.90, respectively, indicating solid upward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

With a market capitalization of $121.99 billion, the average volume of shares traded in the last three months was 1.8 million.

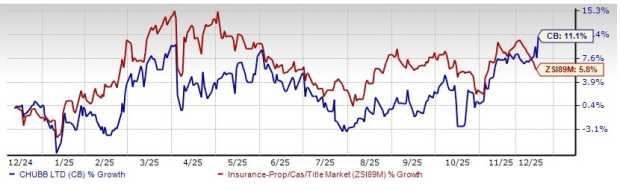

Shares of Chubb have gained 11.1% in the past year, outperforming its industry’s growth of 5.8%.

Shares of Chubb are trading at a premium compared with the Zacks Property and Casualty Insurance industry. Its forward price-to-book value of 1.55X is higher than the industry average of 1.48X.

Shares of The Travelers Companies, Inc. TRV, W.R. Berkley Corporation WRB, and Kinsale Capital Group, Inc. KNSL are trading at a multiple higher than the industry average.

The Zacks Consensus Estimate for Chubb’s 2025 earnings per share indicates a year-over-year increase of 5.1%. The consensus estimate for revenues is pegged at $59.77 billion, implying a year-over-year improvement of 6.3%.

The consensus estimate for 2026 earnings per share and revenues indicates an increase of 8.9% and 6.5%, respectively, from the corresponding 2025 estimates.

One of the 11 analysts covering the stock has raised estimates for 2025 and 2026 over the past 30 days. Thus, the Zacks Consensus Estimate for 2025 earnings has moved up 0.6% in the past 30 days, and for 2026, the same has moved north 0.2% in the same time frame.

Based on short-term price targets offered by 23 analysts, the Zacks average price target is $310.65 per share. The average indicates a potential 4.7% upside from the last closing price.

Chubb Limited’s bottom line surpassed earnings estimates in each of the last four quarters, the average being 13.37%.

Return on equity in the trailing 12 months was 12.9%, better than the industry average of 8%. Return on equity, a profitability measure, reflects how effectively a company is utilizing its shareholders.

Also, return on invested capital (ROIC) has been increasing over the last few quarters amid capital investments made over the same time frame. This reflects CB’s efficiency in utilizing funds to generate income. ROIC in the trailing 12 months was 8.5%, better than the industry average of 6.2%.

Chubb Limited remains focused on capitalizing on the potential of middle-market businesses (both domestic and international) as well as enhancing traditional core packages and specialty products for long-term growth. In its efforts to accelerate growth, Chubb Limited is also making strategic investments in various initiatives.

CB pursues strategic mergers and acquisitions to diversify its portfolio, add capabilities and synergies, and expand its geographic footprint. Recently, Chubb Limited agreed to acquire the insurance businesses of Liberty Mutual in Thailand and Vietnam. Acquisitions have also improved premium revenues. Premiums should also benefit from commercial P&C rate increases, new business, and strong renewal retention. An impressive inorganic growth story helps to achieve a higher long-term return on equity.

Investment income should benefit from improved operating cash flow. Chubb Limited expects the Investment income run rate to continue to grow, as the company reinvests the cash flow at higher rates. Chubb Limited expects adjusted net investment income to be $1.775 billion in the fourth quarter and $1.81 billion in first-quarter 2026.

Chubb Limited has a strong capital position and sufficient cash-generation capabilities, which support wealth distribution to shareholders and growth initiatives.

Being a P&C insurer, CB is exposed to catastrophe events, which induce volatility in underwriting profitability and affect the combined ratio. Given the uncertainty surrounding the magnitude of cat loss, higher losses could drain earnings.

Also, Chubb’s leverage and times interest earned compare unfavorably with the industry.

Chubb Limited’s market-leading position, compelling portfolio, strong renewal retention, positive rate increases, solid capital position, and better return on capital pave the way for long-term growth.

The strong capital and liquidity position enable Chubb Limited to distribute wealth to its shareholders via share buybacks and dividend payouts. The company’s current dividend yield of 1.2% is better than the industry average of 0.2%. The recent 6.6% increase in dividends marks the 32nd straight year of dividend increase. Chubb Limited has a solid track record of dividend hikes, with the metric witnessing a 10-year CAGR of 3.8%. This makes the stock an attractive pick for investors looking for a safe and steady flow of cash.

However, given its premium valuation, we prefer to stay cautious on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite