|

|

|

|

|||||

|

|

|

Digital Turbine APPS and PubMatic PUBM are both part of the digital advertisement market, serving two different verticals. Digital Turbine is deeply integrated as an on-device advertising and app-distribution platform. PubMatic serves as a sell-side platform enabling advertisement publishers to sell their advertising inventory programmatically.

As the AdTech market is expected to grow at a 14.4% rate from 2025 to 2030, per a report by Grand View Research, both companies are going to capitalize on this trend. Let's dive deeper and compare these companies to uncover growth prospects and strategies so investors can make an informed bet.

Digital Turbine’s App Growth Platform (AGP), which connects demand-side platforms (DSPs) with publishers through a programmatic marketplace, is experiencing massive traction due to growth in its distribution of SDK footprint, non-gaming inventory and robust performance in the APAC region.

In the second quarter of fiscal 2026, APPS’ AGP supply volumes experienced a surge in impressions by 30% year over year. APPS’ AGP platform, which operates on cost per mile or cost per install models based on control of ad slots, is now being improved with the implementation of AI and ML to improve targeting and return on ad spend.

APPS is leveraging its Ignite Graph, which is a first-party data engine and DTiQ, an AI/machine learning prediction platform. APPS is improving ad targeting, return on ad spend and user experience. APPS’ AGP segment grew 20% year over year, delivering $44.7 million in revenues.

APPS’ On Device Solutions is also benefiting from strong advertiser demand, which has led to more than 30% year-over-year growth in revenue per device across the U.S. and international markets for the ODS business. Improved pricing, fill rates and premium placements are also a tailwind for the company.

PubMatic is leveraging CTV, AI-driven automation, and sell-side data intelligence to drive its growth amid the macro pressures and reduced spend from legacy DSP customers. The company is aggressively expanding and diversifying its DSP mix, reducing dependence on legacy buyers and concentrating on mid-tier DSP partners.

Mid-tier DSP partners have become a powerful growth engine, with ad spend from these partners rising more than 25% year over year as performance marketers and agencies adopt PubMatic’s AI-enabled tools. The company has onboarded more than 25 new DSP partners in 2025 and has broadened demand optionality.

Additionally, the company launched Programmatic Guaranteed with a top-three DSP, enabling more efficient execution around CTV and premium video deal Supply Path Optimization (SPO), driving Higher Platform Engagement. SPO represented more than 55% of all platform activity in the third quarter of 2025.

PubMatic has heavily invested in AI, building a three-layered AI system across infrastructure, application, and transactions, creating a defensible moat. It has partnered with NVIDIA and is improving on a five times faster bid response speed, less auction timeout, serving three times more ad requests per server.

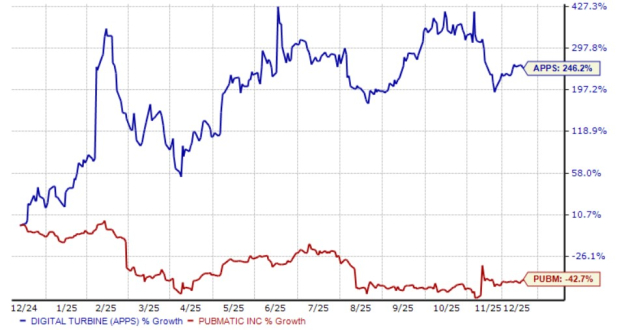

In the past year, APPS shares have skyrocketed 246.2% against the 42.7% decline in PUBM shares.

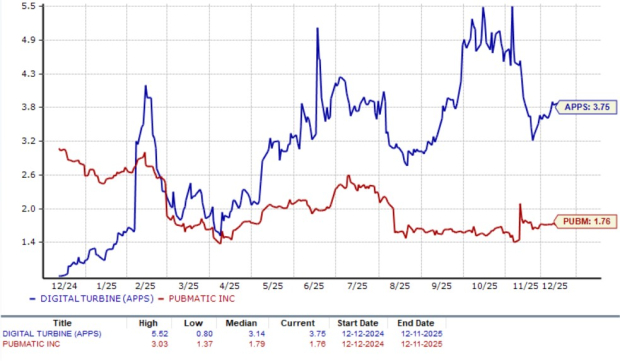

On the valuation front, APPS trades at a trailing 12-month P/B multiple of 3.75X, higher than PUBM’s 1.76X.

The Zacks Consensus Estimate for Digital Turbine’s fiscal 2026 earnings implies a year-over-year decline of 5.7%. The estimate for fiscal 2026 has been revised downward in the past 60 days.

Digital Turbine, Inc. price-consensus-chart | Digital Turbine, Inc. Quote

However, the Zacks Consensus Estimate for PUBM’s 2025 earnings is pegged at 19 cents per share, which has declined 75.6% year over year. The estimate for 2025 has been revised upward in the past 30 days.

PubMatic, Inc. price-consensus-chart | PubMatic, Inc. Quote

APPS benefits from strong on-device demand, expanding data capabilities and rapid revenue growth, while PUBM leverages CTV, AI innovation and a diversified DSP mix to strengthen its long-term moat. However, PUBM faces macro pressures and reduced spend from legacy DSP customers, leading it to change its business model.

Currently, APPS sports a Zacks Rank #1 (Strong Buy), making the stock a stronger pick than PUBM, which has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite