|

|

|

|

|||||

|

|

|

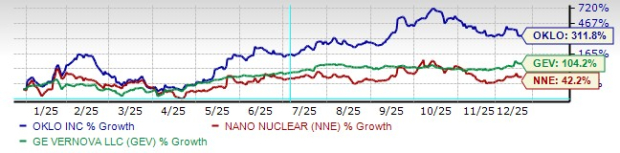

Oklo Inc. OKLO has delivered one of the most eye-catching rallies in the market this year, climbing more than 300% as investors rushed into advanced nuclear names tied to artificial intelligence (AI)-driven power demand. The surge has pushed OKLO into the spotlight, but it has also widened the gap between valuation and current fundamentals.

As construction begins and timelines come into focus, the stock’s risk-reward profile increasingly depends on investor horizon and tolerance for volatility. Adding to this challenge is rising competition from NANO Nuclear Energy NNE and the safer investment option that investors see in GE Vernova GEV, putting OKLO at a difficult but pivotal turning point.

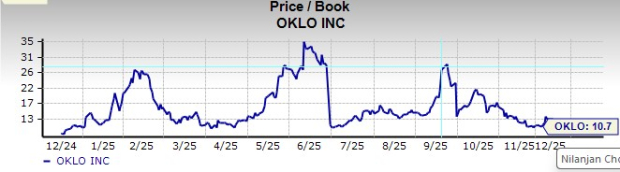

OKLO’s rally has been driven more by long-term hopes than by current results. The company is still pre-revenue and reported a loss of 20 cents per share in the third quarter of 2025, yet the stock has traded near 11 times book value, showing how much future success is already priced in. Its surge has also far outpaced peers such as NANO Nuclear and GE Vernova. That contrast is telling, as GE Vernova benefits from a broad energy portfolio and rising earnings, while NANO Nuclear advances its microreactor plans with a solid balance sheet and less near-term funding pressure.

This matters because, as OKLO moves from concept to construction, investors will focus more on costs and timelines. Any overruns or delays could quickly pressure the stock, given the high expectations already embedded.

Even so, OKLO continues to ride strong narrative support. Selection for three Department of Energy (DOE) reactor pilot projects and early work at the Aurora-INL site signal real progress, easing regulatory risk and supporting premium valuations, at least i

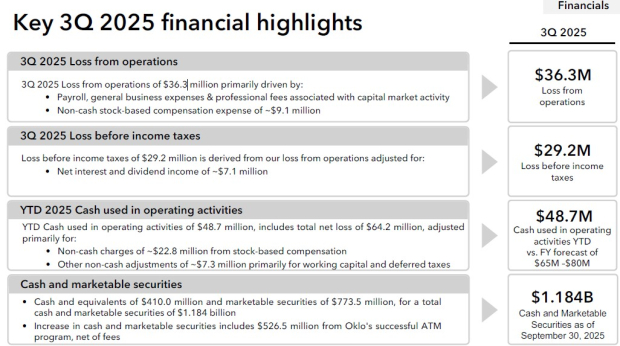

OKLO enters its most capital-intensive phase with a strong balance sheet. As of the third quarter of 2025, the company held about $1.2 billion in cash and marketable securities. Management expects full-year cash used in operations to range between $65 million and $80 million.

This liquidity provides a multi-year runway and reduces the risk of near-term financial stress. This cash cushion gives OKLO several years of funding and lowers the chance that it will need to raise money in a hurry or on unfavorable terms as spending ramps up.

That financial flexibility has come with meaningful dilution. OKLO raised roughly $540 million through at-the-market (ATM) equity sales during 2025 and authorized up to $1.5 billion in additional ATM capacity. However, investors must carefully consider the risk of dilution. Because OKLO is issuing a large number of new shares through this avenue, its financial filings clearly point out that this could reduce the immediate and future value of existing shares.

In simple terms, the frequent issuance of new shares can make it difficult for the stock price to keep rising, especially when much of the valuation is already based on expectations far into the future. This dynamic contrasts with more established nuclear players like GE Vernova, where dilution risk is far lower.

Operating losses remain significant, with a third-quarter operating loss of $36.3 million. Importantly, Aurora-INL will initially operate under DOE authorization as a prototype, not as a grid-connected commercial plant. As a result, meaningful power revenues remain several years away.

For investors focused on near-term earnings inflection points, this pushes the payoff further into the future. The stock is now underwriting multiple years of cash burn before commercial revenues begin.

Construction is historically the most challenging phase for nuclear projects. OKLO has begun ordering long-lead components and advancing site work, but has deferred detailed capital cost estimates until 2026.

Any unexpected delays, cost overruns, or problems with government approvals during this critical construction phase could hurt the stock's valuation. This happens because investors would immediately start to doubt the company's ability to build the reactors affordably and on schedule, long before it ever generates its first dollar of sales.

OKLO’s current setup may appeal to long-term, risk-tolerant investors willing to absorb dilution and volatility in exchange for exposure to advanced nuclear power. Investors seeking nearer-term cash flow, earnings visibility, or valuation support may find the stock less compelling after its massive run.

At present, OKLO carries a Zacks Rank #3 (Hold), reflecting a balance between strong long-term optionality and meaningful near-term risks tied to dilution, execution and the absence of revenues.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite