|

|

|

|

|||||

|

|

|

McDonald’s Corporation MCD and Chipotle Mexican Grill, Inc. CMG stand as two bellwethers of the U.S. restaurant industry, each navigating a consumer environment defined by heightened price sensitivity, uneven traffic trends and rising input costs. While McDonald’s is leaning into value, scale and digital engagement to defend guest counts and earnings durability, Chipotle is working through a period of transaction pressure while investing heavily in operations, menu innovation and long-term expansion.

As investors weigh resilience against recovery potential, the contrasting strategies and near-term fundamentals of these two restaurant leaders set the stage for a compelling stock-to-stock comparison. Let’s dive deep and closely compare the fundamentals of the two stocks to determine which name is better situated today.

McDonald’s continues to demonstrate resilience in a challenging consumer environment, leveraging its scale, brand strength and disciplined execution to maintain traffic share gains relative to peers. The company’s strategy remains anchored in reinforcing everyday value, supported by strong marketing and targeted menu innovation, which together help sustain relevance across income cohorts even as industry-wide traffic remains pressured.

A key positive is the renewed focus on menu affordability highlighted by the relaunch of Extra Value Meals. These offerings represent a meaningful portion of U.S. transactions and are designed to rebuild value perception directly on the menu board. Management’s willingness to co-invest alongside franchisees underscores system alignment and reflects a longer-term view that traffic recovery ultimately strengthens unit economics. Over time, improved value perception is expected to support broader momentum in guest counts.

Menu innovation provides an additional growth lever. Chicken-focused launches, localized international offerings and early success from expanded beverage tests suggest McDonald’s is targeting incremental occasions and higher average checks without over-reliance on price increases. These initiatives reinforce the brand’s ability to adapt to evolving consumer preferences while maintaining operational discipline.

That said, trade-offs remain. Elevated labor and commodity costs — particularly in beef — continue to pressure restaurant-level margins, and management has acknowledged that margin expansion depends on stronger, sustained top-line growth. Consumer behavior also remains bifurcated, with higher-income traffic holding up well while lower-income consumers remain under pressure, limiting near-term traffic acceleration in certain dayparts.

Overall, McDonald’s presents a profile of defensive durability paired with intentional investment. The company is prioritizing traffic, affordability and brand trust over near-term margin optimization, positioning the business to emerge stronger when consumer conditions stabilize.

Chipotle is navigating a more challenging near-term operating backdrop, marked by broad-based transaction pressure and heightened consumer sensitivity, particularly among lower- and middle-income cohorts that make up a meaningful share of its customer base. Management stated that recent softness reflects macro-driven frequency pullbacks rather than brand-specific share loss.

Operational consistency has also been an area of focus. Management acknowledged challenges in digital order accuracy, ingredient availability and maintaining uniform restaurant standards, particularly as digital and off-premise channels scale. These gaps prompted renewed training efforts and changes to incentive structures to better align teams with guest experience priorities.

Cost pressures are expected to intensify as inflation trends higher, caused largely by beef costs and tariffs. Management indicated that pricing actions will be measured and may not fully offset inflation in the near term, prioritizing value perception for guests. While this approach supports demand sensitivity, it also places near-term pressure on margins until underlying transaction trends improve.

Looking forward, Chipotle is leaning on a set of initiatives aimed at supporting longer-term growth, including equipment upgrades, increased menu innovation, loyalty enhancements and new sales occasions such as catering. Management characterized many of these efforts as still in early stages, with benefits expected to build over time. With unit expansion continuing amid a softer demand backdrop, near-term performance remains closely tied to the pace of consumer stabilization.

The Zacks Consensus Estimate for MCD’s 2026 sales and earnings per share (EPS) suggests year-over-year increases of 5.7% and 9.6%, respectively. In the past 60 days, earnings estimates for 2026 have declined 0.8%.

The Zacks Consensus Estimate for Chipotle’s 2026 sales and EPS suggests year-over-year increases of 9.7% and 4.7%, respectively. In the past 60 days, earnings estimates for 2026 have declined 12.2%.

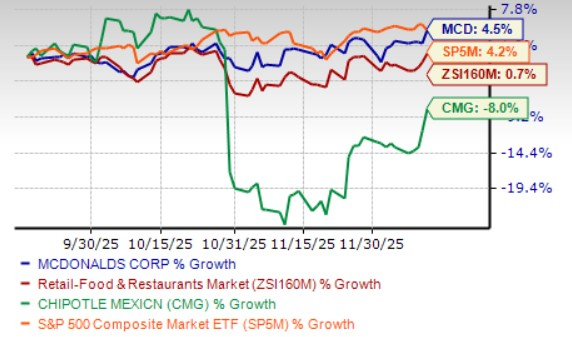

McDonald’s stock has gained 4.5% in the past three months, outperforming its industry's rise of 0.7% and the S&P 500’s growth of 4.2%. Meanwhile, Chipotle shares have dropped 8% in the same time frame.

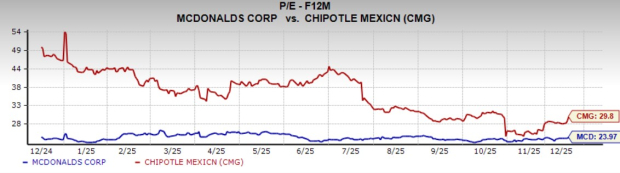

MCD is trading at a forward 12-month price-to-earnings (P/E) multiple of 23.97, below the industry average of 24.08 over the last year. Chipotle’s forward 12-month P/E multiple sits at 29.8 over the same time frame.

At this point, McDonald’s appears better positioned to deliver steadier performance and downside protection in a volatile consumer environment. Its emphasis on value, scale-driven efficiency and traffic stabilization provides a more predictable earnings profile, supported by comparatively modest estimate revisions and a valuation that sits below both Chipotle and the broader industry. The Zacks Consensus Estimate trends reinforce this view, signaling greater confidence in McDonald’s ability to generate consistent sales and earnings growth even as cost pressures persist.

Meanwhile, Chipotle faces a more challenging near-term setup. Ongoing transaction pressure, operational execution gaps and sharper downward earnings revisions point to a longer path toward stabilization. Until consumer demand firms and internal initiatives translate into measurable traffic and margin recovery, visibility remains limited. As a result, McDonald’s screens as the more compelling stock right now, offering a balance of resilience, valuation support and clearer near-term earnings durability. McDonald’s currently carries a Zacks Rank #3 (Hold), while Chipotle has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 51 min | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| Aug-10 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-07 |

Fast-Food Giant Posts Mixed Q2 Results. Papa John's Falls To 2012 Low.

MCD

Investor's Business Daily

|

| Aug-07 | |

| Aug-07 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite