|

|

|

|

|||||

|

|

|

Costco Wholesale Corporation’s COST first-quarter fiscal 2026 performance once again highlighted the strength of the membership business model. Membership income has been one of the company’s most resilient and predictable revenue streams. Membership fees jumped 14% to $1,329 million, gaining from strong renewal rates and the annualized benefit of the recent membership fee increase. Excluding the membership fee increase and FX, membership income rose 7.3% year over year.

Sustained membership growth has been the primary driver of the increase in membership fees. The total number of paid households rose 5.2% to 81.4 million from the prior-year period, while total cardholders grew 5.1% to 145.9 million. A key contributor to membership income was the 9.1% year-over-year increase in executive memberships to 39.7 million. Executive members now represent 74.3% of total sales.

By prioritizing value and quality, the company has built strong customer loyalty, leading to an impressive membership renewal rate of 92.2% in the United States and Canada, and 89.7% worldwide in the quarter. While both renewal rates declined 10 basis points sequentially due to a mix shift toward new online sign-ups, proactive communication efforts aimed at improving retention helped offset some of the pressure.

The quarter highlighted how Costco’s membership income continues to be stable and recurring. The combination of pricing leverage, expanding paid households and executive upgrades reinforces the role of membership fees as a dependable earnings contributor even when the sales environment is not conducive.

BJ’s Wholesale Club Holdings, Inc.’s BJ membership fee income jumped 9.8% to $126.3 million during the third quarter of fiscal 2025, reflecting strength in member acquisition, retention and higher-tier penetration. BJ’s Wholesale highlighted tenured renewal rates of roughly 90% with a strong higher-tier penetration of 41%. BJ’s Wholesale benefits from rising higher-tier membership adoption, which improves the quality and predictability of membership income.

Walmart Inc. WMT reported global membership fee income growth of 17% during the third quarter of fiscal 2026, reflecting momentum across Walmart+ and Sam’s Club. Walmart noted double-digit growth in Walmart+ fee income in the United States, while Sam’s Club delivered growth in member counts, renewal rates and premium Plus membership penetration. As a result, Walmart continues to diversify profit streams by embedding membership income more deeply into its broader omnichannel model, reinforcing its role as a steady and recurring contributor alongside core retail operations.

Costco stock has declined 10.9% over the past year against the industry’s growth of 1.7%.

From a valuation standpoint, Costco's forward 12-month price-to-earnings ratio stands at 42.99, higher than the industry’s ratio of 30.15. COST carries a Value Score of C.

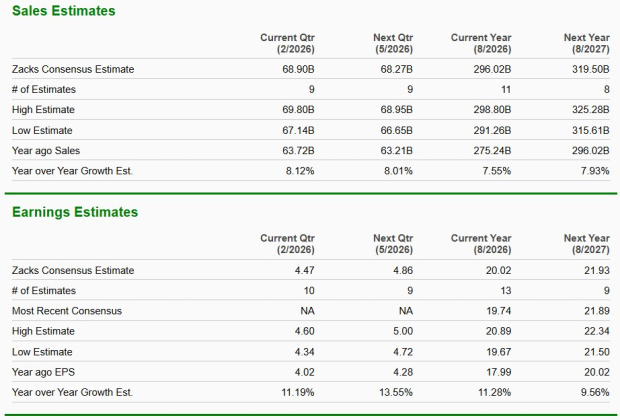

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 7.6% and 11.3%, respectively.

Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-19 | |

| Jul-18 | |

| Jul-18 |

Costco Gas Pumps Are So Popular the Retailer Is Building Stand-Alone Stations

COST

The Wall Street Journal

|

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite