|

|

|

|

|||||

|

|

|

The U.S. economy is currently in a transition phase, characterized by easing financial conditions and steadily improving consumer sentiment. The recent rate cut by the Federal Reserve indicates a shift toward a more accommodative monetary policy, aimed at supporting economic growth as inflationary pressures moderate. Despite these improvements, households remain mindful of their budgets. Against this backdrop, discount retailers present attractive investment opportunities for 2026, benefiting from cautious spending habits and a gradual recovery in demand.

Although inflation has eased from its peak, the cost of essential items remains well above pre-pandemic levels. This has driven a “trade-down” effect, with consumers across income levels increasingly turning to value-oriented options. As a result, discount retailers continue to see steady foot traffic as shoppers seek affordable choices for both necessity and discretionary purchases.

Discount retailers also benefit from structural operating advantages. Lean store formats, efficient supply chains, digitization and rapid inventory turnover enable these companies to respond quickly to changes in consumer demand. Additionally, an emphasis on private-label products supports margin stability while enabling competitive pricing. Meanwhile, investments in data analytics and artificial intelligence are optimizing operations, personalizing customer experiences and driving efficiency.

Looking ahead to 2026, the outlook for the sector appears increasingly promising as the impacts of easing monetary policy gradually influence consumer spending and corporate profits. Given these factors, we've identified four discount retailers — Ross Stores, Inc. ROST, Dollar General Corporation DG, Costco Wholesale Corporation COST and Burlington Stores, Inc. BURL — to keep an eye on.

Ross Stores continues to demonstrate the strength of its off-price model, driven by compelling branded assortments, effective merchandising execution and strong customer engagement across regions. Management highlighted broad-based category momentum, improved vendor partnerships, and successful marketing initiatives that are enhancing traffic and basket trends. Store expansion and disciplined inventory management further reinforce its ability to capitalize on favorable buying opportunities. With a resilient value proposition and a proven operating playbook, Ross appears well-positioned to sustain market share gains and long-term growth.

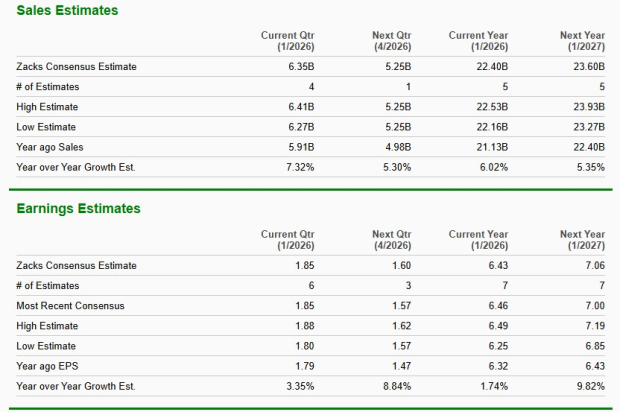

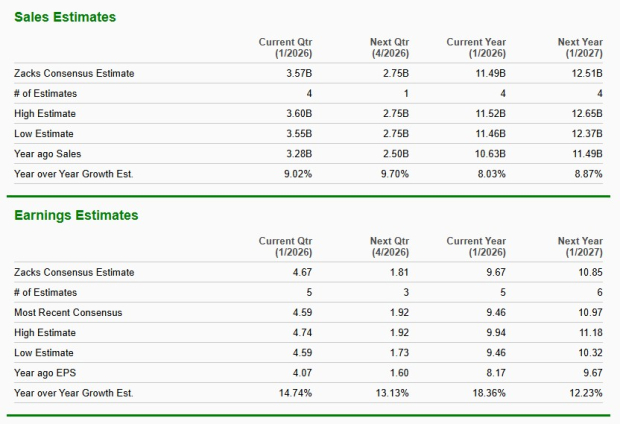

The Zacks Consensus Estimate for Ross Stores’ current financial-year sales and EPS implies growth of 6% and 1.7%, respectively, from the year-ago period’s actuals. For the next fiscal year, the consensus estimate indicates a 5.4% rise in sales and 9.8% growth in earnings. This Zacks #2 (Buy) Ranked company has a trailing four-quarter earnings surprise of 6.7%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Dollar General’s case rests on its powerful value-and-convenience proposition, expanding appeal across income cohorts, and consistent market share gains in both consumable and non-consumable categories. Strategic initiatives around pricing, private brands, shrink reduction, and operational execution are translating into stronger profitability and cash generation. The company’s dense store footprint, ongoing remodels and disciplined capital allocation support durable competitive advantages. As execution continues to improve, Dollar General is positioned to drive steady growth and reinforce its role as a defensive retail leader.

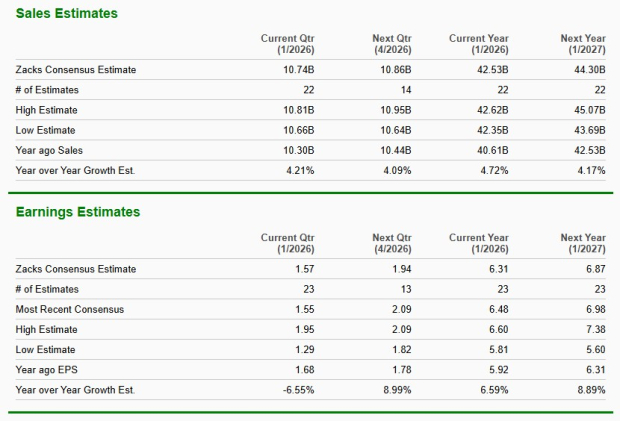

The Zacks Consensus Estimate for Dollar General’s current financial-year sales and EPS implies growth of 4.7% and 6.6%, respectively, from the year-ago period’s actuals. For the next fiscal year, the consensus estimate indicates a 4.2% rise in sales and 8.9% growth in earnings. This Zacks Rank #3 (Hold) company has a trailing four-quarter earnings surprise of 22.9%, on average.

Costco’s differentiated membership-driven model continues to fuel strong traffic, brand loyalty and market share gains, supported by a curated value-oriented assortment and expanding global footprint. The company’s investments in digital capabilities, personalization and operational technology, such as AI-enhanced inventory systems, are improving efficiency and elevating the member experience. Robust membership renewal rates and rising Executive penetration reinforce the strength of its ecosystem and recurring revenue base. Costco's disciplined expansion strategy and focus on quality, value and newness underscore its competitive moat.

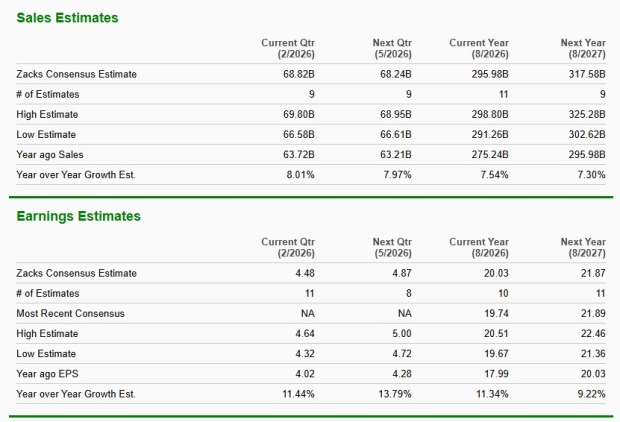

The Zacks Consensus Estimate for Costco’s current financial-year sales and EPS calls for growth of 7.5% and 11.3%, respectively, from the year-ago period’s actuals. For the next fiscal year, the consensus estimate indicates a 7.3% rise in sales and 9.2% growth in earnings. This Zacks Rank #3 company has a trailing four-quarter earnings surprise of 0.5%, on average.

Burlington Stores is making meaningful progress executing its off-price transformation, supported by margin expansion, disciplined cost control and improving merchandising capabilities. Management emphasized strong underlying demand, effective inventory flexibility and a robust pipeline of new store openings that continues to exceed expectations. Investments in supply chain efficiency and operational initiatives are strengthening profitability while preserving value leadership. As operational improvements scale alongside unit growth, Burlington appears well-positioned to deliver durable earnings power and long-term shareholder value.

The Zacks Consensus Estimate for Burlington Stores’ current financial-year sales and EPS implies growth of 8% and 18.4%, respectively, from the year-ago period’s actuals. For the next fiscal year, the consensus estimate indicates an 8.9% rise in sales and 12.2% growth in earnings. This Zacks Rank #3 company has a trailing four-quarter earnings surprise of 0.5%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite