|

|

|

|

|||||

|

|

|

Shares of Pfizer PFE dropped more than 3% on Tuesday after the company announced its financial outlook for the full year 2026, which fell short of investor expectations. The company is expected to have a soft financial performance over the next three years, owing to waning demand for COVID-19 products and a rising loss of exclusivity (LOE) across its portfolio.

Pfizer expects total revenues for 2026 to be between $59.5 billion and $62.5 billion, which includes $5 billion from the sales of its COVID-19 products. While this outlook is in line with the Zacks Consensus Estimate of $61.83 billion, it implies modest growth compared with the company’s revised 2025 revenue expectation of around $62 billion (previous guidance: $61-$64 billion).

The company also issued guidance for adjusted EPS for 2026, which stood at $2.80-$3.00. This guidance, however, fell short of the Zacks Consensus Estimate of $3.08 per share. Adjusted R&D expenses are expected to be in the range of $10.5 to $11.5 billion in 2026, while adjusted SI&A spending is targeted between $12.5 billion and $13.5 billion. The adjusted effective tax rate is expected to be approximately 15% in 2026.

During the conference call, Pfizer noted that it exceeded its cost-saving targets for 2025 and reaffirmed plans to deliver $7.2 billion in cumulative cost reductions by 2027, with the majority of savings expected to be realized in 2026.

Apart from sales, Pfizer reiterated the rest of its 2025 guidance. The company expects to close this year with adjusted EPS between $3.00 and $3.15. Adjusted R&D and SI&A expenses are expected to be in the ranges of $10.0-$11.0 billion and $13.1-$14.1 billion, respectively. The adjusted effective tax rate is expected to be approximately 11% in 2025.

Looking beyond 2026, Pfizer does not expect a return to robust growth until toward the end of this decade. On the COVID-19 front, the company is targeting total COVID-19 product sales of about $6.5 billion in 2025, but expects this figure to decline by roughly $1.5 billion in 2026. During the conference call, management noted that sales of antiviral Paxlovid are expected to fall more sharply than those of its COVID-19 vaccine.

At the same time, Pfizer faces an escalating patent cliff. While the company expects to bear a $1.5 billion hit from LOEs next year, revenue losses are projected to exceed $3 billion in 2027 and more than $6 billion in 2028.

Excluding COVID-19 products and LOE-impacted drugs, Pfizer is still targeting about 4% year-over-year operational revenue growth. However, management acknowledged that new launches and pipeline contributions will not fully offset these pressures in the near term, delaying a meaningful growth inflection until 2029.

This guidance outlook has raised concerns among investors, who have questioned Pfizer’s investment choices over the past few years, ranging from the $43 billion Seagen acquisition in 2023 to the recent $10 billion buyout of Metsera, which was completed last month.

Pfizer has currently sharpened its strategic focus on two key growth pillars — obesity and oncology. Through the Metsera acquisition, Pfizer is building an early-stage obesity pipeline aimed at eventually competing with market leaders Eli Lilly LLY and Novo Nordisk NVO. However, since the Metsera candidates are still in early- to mid-stage development, any meaningful revenue contribution from obesity is unlikely over the next few years.

On the oncology front, Pfizer is prioritizing development of its recently licensed PD-1×VEGF bispecific antibody from China-based 3SBio, positioning it as a potential next-generation immuno-oncology therapy. However, competition in this space is intensifying. Summit Therapeutics SMMT is advancing its PD-1/VEGF candidate, ivonescimab, in partnership with Akeso, while BioNTech and Bristol Myers Squibb are jointly developing a similar bispecific therapy called BNT327.

Shares of Pfizer have underperformed the industry year to date, as shown in the chart below.

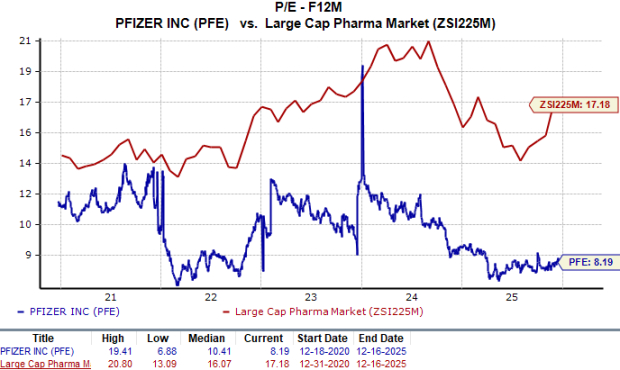

From a valuation standpoint, Pfizer appears attractive relative to the industry and is trading below its 5-year mean. Going by the price/earnings ratio, the company’s shares currently trade at 8.19 times forward earnings, lower than 17.18 for the industry and the stock’s 5-year mean of 10.41.

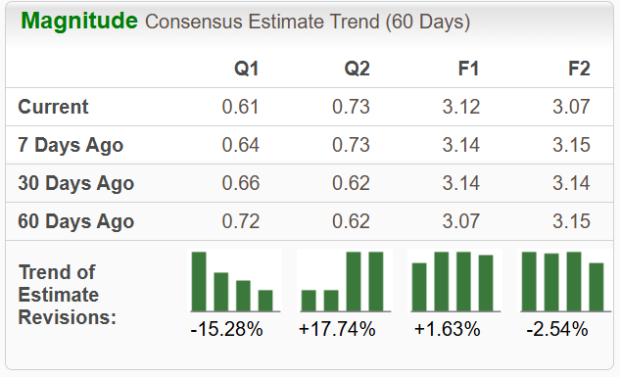

EPS estimates for 2025 and 2026 have declined over the past 30 days.

Pfizer currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 15 min | |

| 36 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours |

Pfizer Hikes 2026 Sales Outlook By $500 Million On Second-Quarter Beat

PFE

Investor's Business Daily

|

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite