|

|

|

|

|||||

|

|

|

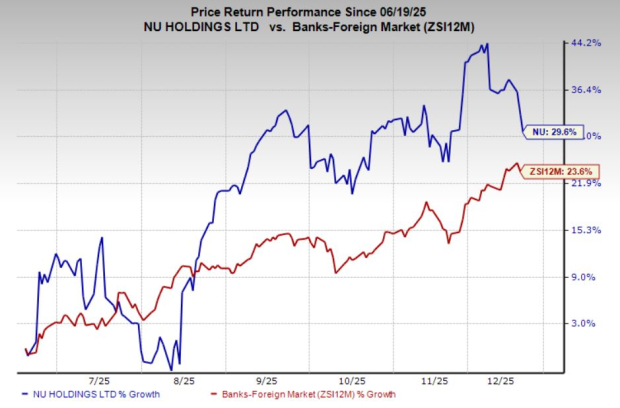

Nu Holdings Ltd. NU has witnessed a 30% rise in its stock price over the six months, outpacing the broader industry’s 24% rise.This piece examines NU’s recent performance and growth trajectory to determine whether the dip presents an attractive buying opportunity.

At this stage of its growth cycle, Nu Holdings’ most powerful differentiator is the growing durability of its revenues. The company has demonstrated a clear ability to translate its vast customer base into recurring, multi-product income streams that are far less exposed to macroeconomic swings. In the third quarter of 2025, Nu sustained strong momentum by expanding its customer base to 127 million, adding more than 4 million new users, while maintaining an activity rate above 83%.

While Nubank’s earlier narrative was driven primarily by rapid user acquisition, the more important evolution today is the deepening monetization of those users across payments, credit, savings, insurance and other financial services. This shift toward predictable, repeatable revenue streams positions Nu Holdings for more stable performance, even during periods of tighter credit conditions or renewed foreign-exchange volatility in Latin America. Reflecting this progress, revenues grew 39% year over year on a currency-neutral basis in the third quarter, reaching $4.2 billion.

A key contributor to this resilience is the company’s disciplined focus on high-engagement products. Rather than stretching into higher-risk credit to boost short-term earnings, Nu Holdings continues to scale revenues through everyday transactions, low-cost deposits and steady cross-selling. These revenue streams naturally compound with scale and help smooth out the quarter-to-quarter volatility that often challenges traditional banks. As more customers adopt multiple products, average revenue per active user continues to rise, reinforcing long-term earnings visibility.

The model becomes even more attractive when paired with Nu Holdings’ efficient cost structure. Its technology-led platform avoids the burden of extensive physical infrastructure, allowing incremental revenue from additional products to translate more directly into operating leverage. At a time when legacy banks are grappling with rising compliance and structural costs, Nu Holdings’ revenue durability stands out as a meaningful strategic advantage, one that supports premium valuation multiples and underpins consistent shareholder returns in the next phase of growth.

Block XYZ remains an important comparison because its ecosystem shows what Nu Holdings could become at scale. Block, through Cash App and Square, maintains a multi-product financial platform that grows wallet share as users adopt more services. The pattern mirrors how Block expanded beyond payments into credit and deposits, reinforcing the link between user engagement and durable revenue.

SoFi Technologies SOFI provides another relevant benchmark as a digital-first institution that strengthened its results by broadening its financial suite. SoFi demonstrated that cross-selling loans, deposits, and investment tools can turn a fast-growing user base into a stable revenue engine. SoFi shows how diversified, low-friction product expansion can convert scale into consistent, defensible revenue momentum.

NU also excels in capital efficiency, showcasing strong profitability metrics. Its trailing 12-month return on equity stands at 30%, nearly triple the industry average of 11.4%. Likewise, NU’s return on invested capital of 14.3% significantly surpasses the sector average of 3.4%, underscoring management’s effectiveness in deploying capital to generate robust shareholder returns.

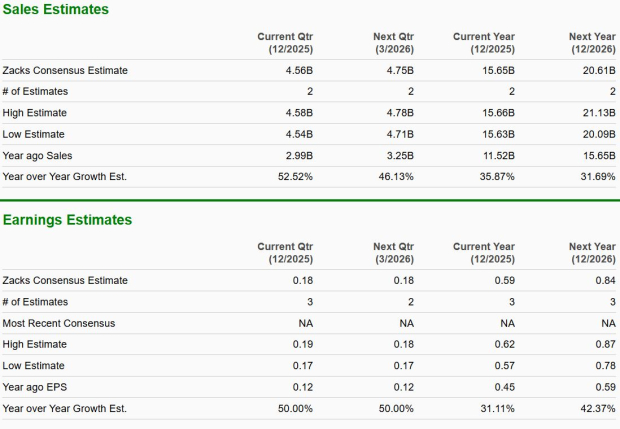

The Zacks Consensus Estimate for NU’s 2025 earnings is pegged at 59 cents, indicating 31% growth from the year-ago level. Earnings for 2026 are expected to increase 42% from the prior-year actuals. The company’s sales are expected to rise 36% and 32% year over year, respectively, in fiscal 2025 and 2026.

Nu Holdings is steadily evolving into a high-quality, durable fintech platform rather than a pure user-growth story. Its ability to deepen monetization through everyday financial services, maintain strong customer engagement, and scale efficiently gives the business resilience across economic cycles. The company’s disciplined approach to product expansion limits risk while supporting predictable, recurring revenue streams. Compared with global fintech peers, NU’s model shows improving operating leverage and strong capital efficiency. While short-term volatility cannot be ruled out after a strong run, the long-term fundamentals remain compelling. For investors with a medium to long-term horizon, buying NU appears justified as the company enters a more profitable and stable phase of growth.

NU currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 9 hours | |

| 9 hours | |

| 17 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite